The Million-Dollar Head Start

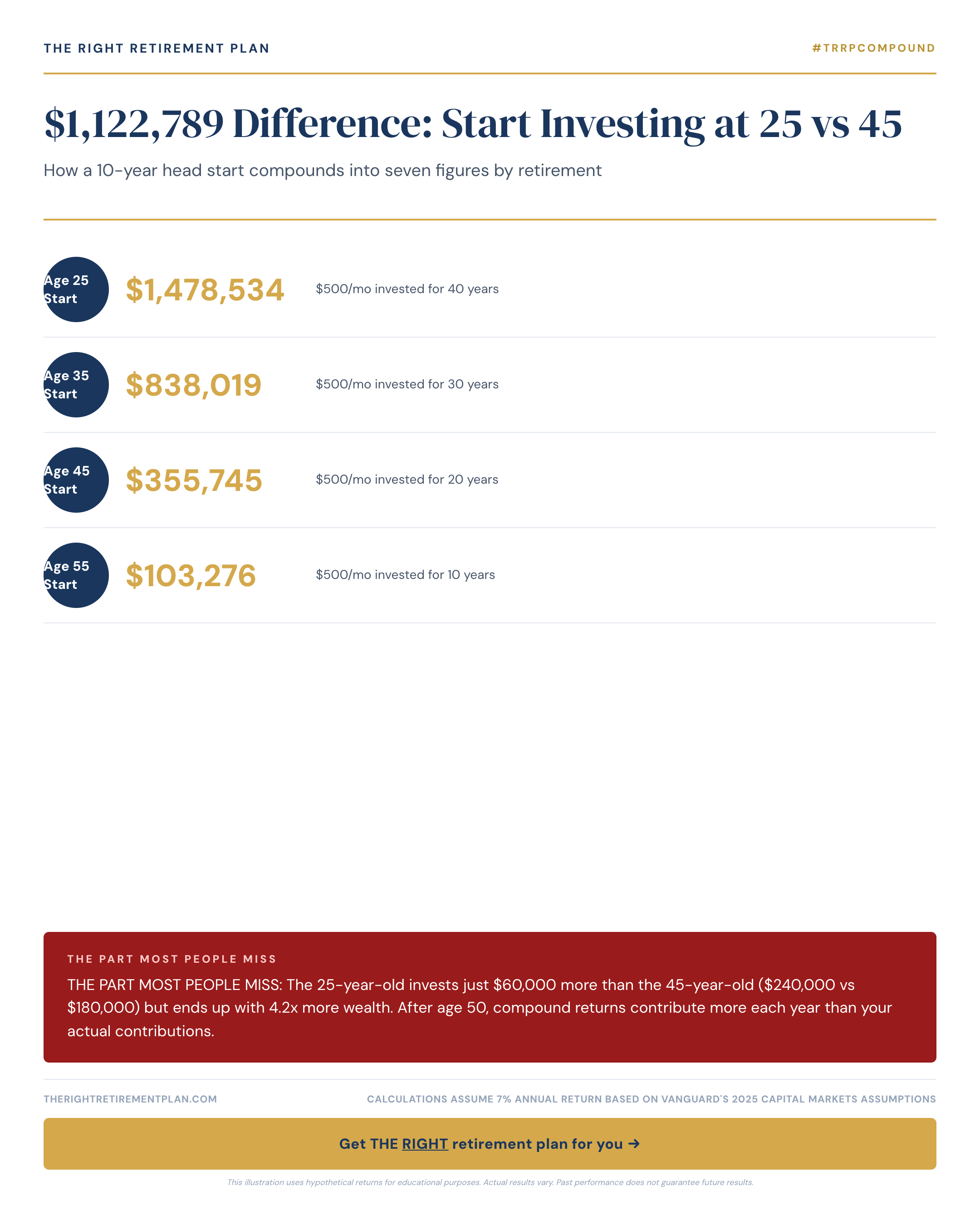

The difference between starting retirement investing at 25 versus 45 isn't just about time, it's about compound growth creating life-changing wealth. A 25-year-old who invests $500 monthly until age 65 accumulates $1,342,789, assuming a 7% annual return. Meanwhile, a 45-year-old investing $750 monthly for the same 20 years reaches just $219,000.

That's a staggering $1,122,789 difference, even though the younger investor contributes only $60,000 more ($240,000 versus $180,000). The early starter ends up with 4.2 times more wealth simply by beginning two decades earlier.

Here's why this matters for retirement planning: compound returns accelerate dramatically over time. In the first decade, your contributions drive most growth. But after age 50, compound returns often contribute more annually than your actual deposits.

Why Geography Matters for Retirement Timing

For Maryland retirees and others in the Mid-Atlantic region, starting early becomes even more critical given higher living costs. A comfortable retirement in areas like Annapolis requires substantial savings, often $1 million or more.

Consider these scenarios:

- Age 25 start: $500/month grows to $1.34 million

- Age 35 start: $750/month grows to $610,000

- Age 45 start: $1,500/month grows to $611,000

Notice how the 45-year-old must invest three times as much monthly to match what the 35-year-old achieves with moderate contributions. This illustrates why retirement investing should begin as early as possible, even with small amounts.

Making Up for Lost Time

If you're starting later, don't panic. Focus on maximizing catch-up contributions once you reach 50. In 2026, you can contribute an extra $7,500 to your 401(k) beyond the standard $23,500 limit, and an additional $1,000 to IRAs beyond the $7,000 base.

Consider these strategies:

- Automate investments to ensure consistency

- Increase contributions with every raise

- Take advantage of employer matching, it's free money

- Review and rebalance annually

Starting your retirement planning journey early isn't just about money, it's about financial freedom and peace of mind. If you want personalized guidance on your retirement timeline, consider taking our Retire Ready Score to see how your current plan measures up.