How The Pitch Usually Works

The pitch shows up in roughly the same shape every time. A glossy illustration. A 10 pay or 7 pay structure. A line chart that climbs steadily. Tax free growth, tax free income, a death benefit on top. Sometimes it is positioned as a better alternative to a 401k or IRA. Sometimes it is positioned as a personal banking system. The framing is always retirement.

There is a reason these products are sold so aggressively. The first year commission on a large 10 pay whole life policy is often a meaningful share of the first year premium. That is not a conspiracy. It is an industry standard incentive structure. When a product pays the seller that much, you should expect to see it sold a lot. And you do.

What The Illustration Does Not Show

A representative case. A 10 pay policy with a 52,000 dollar annual premium. Total scheduled outlay of 520,000 dollars over ten years. The illustration projects non guaranteed cash values and death benefits based on the carrier's current dividend scale.

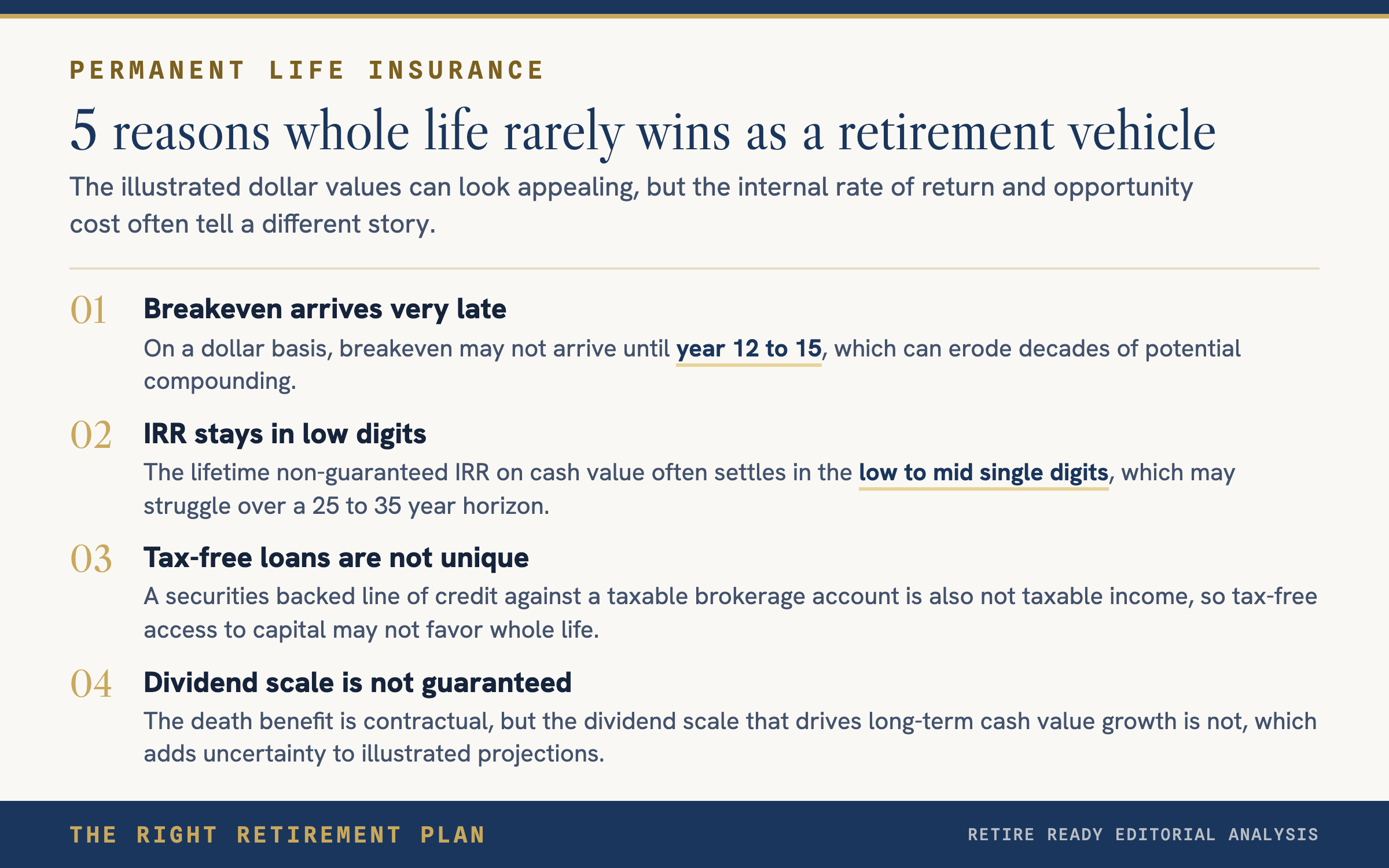

In dollar terms, the chart can look fine. By year 25, cash value can be more than 2.5 times what was paid in. Over 35 years, more than 4 times.

The number that is missing from most illustrations is the internal rate of return on the cash value column. Once that is computed, the picture changes. The breakeven point on a dollar basis often does not arrive until year 12 to 15. The lifetime non guaranteed IRR usually settles in the low to mid single digits. That is not nothing. It is also not a competitive vehicle for a 25 to 35 year retirement horizon.

The Same Money In A Taxable Account

Now run the same outlay through a diversified low cost equity portfolio. No insurance wrapper. Just a regular taxable brokerage account.

Over long periods, the historical equity premium has been difficult for permanent insurance cash value to compete with, even after capital gains taxes. Add direct indexing, where the platform owns the individual stocks inside an index and harvests realized losses at the security level, and the after tax gap widens further for households in higher tax brackets.

The gap that opens up between a well managed taxable account and a typical whole life illustration is the cost of choosing the policy as the retirement vehicle.

What About Tax Free Loans

The most common rebuttal is that whole life cash value can be borrowed against tax free, while continuing to grow. The first half is technically true. The second half is where the nuance lives. Loans accrue interest. Outstanding balances reduce the death benefit. If the policy lapses with a loan outstanding, the tax consequences can be severe.

A securities backed line of credit against a taxable brokerage account is not taxable income either. The underlying portfolio stays invested. The risk is different and loan to value discipline matters. The point is not that an SBLOC is risk free. It is that tax free access to capital is not unique to whole life.

When Permanent Insurance Actually Fits

There are real situations where permanent insurance is the right tool.

- Estate planning for families with taxable estates, especially using an irrevocable life insurance trust.

- Business succession funding where a death benefit funds a buy sell agreement.

- Asset protection in states where life insurance cash value receives meaningful creditor protection.

- A genuine permanent death benefit need that goes beyond what term insurance can solve.

- Forced savings for a household that has demonstrated repeatedly that accessible money will be spent.

Frequently Asked Questions

Is whole life insurance a scam?

No. It is a legitimate product that is often sold for the wrong reason. The product has uses. Funding a 30 year retirement is rarely one of them.

What is a Modified Endowment Contract?

A permanent life policy that has been funded above IRS limits loses much of its tax favored treatment. Loans and withdrawals are taxed as ordinary income up to gain, with a 10 percent penalty before age 59 and a half. Ask explicitly whether the proposed funding pattern triggers MEC status.

What is a securities backed line of credit?

A loan secured by a brokerage account. Loan proceeds are not taxable income. The portfolio stays invested. Lender risk is real, particularly in market drawdowns, and loan to value discipline is the main control.

Should I cancel a whole life policy I already own?

Not without analysis. Surrender charges, cost basis, gain or loss treatment, and any 1035 exchange options all matter. A standalone in force ledger with current dividend scale is the starting point.

What questions should I ask before buying permanent insurance?

What problem is this solving. Is the recommending person a fiduciary. What is the total compensation on the sale. What is the IRR on cash value at year 20 and year 30 under the current dividend scale. Could the policy become a Modified Endowment Contract. Have retirement accounts, HSA funding, emergency reserves, and taxable savings been addressed first.

Take The Next Step

If you want a quick read on whether the products in your retirement plan are actually doing the work they should be, take the free Retire Ready Score. It maps your setup against the five pillars of a complete retirement plan in a few minutes.