When Bonds Stop Paying, Why Dividend Stocks Deserve A Second Look In Retirement

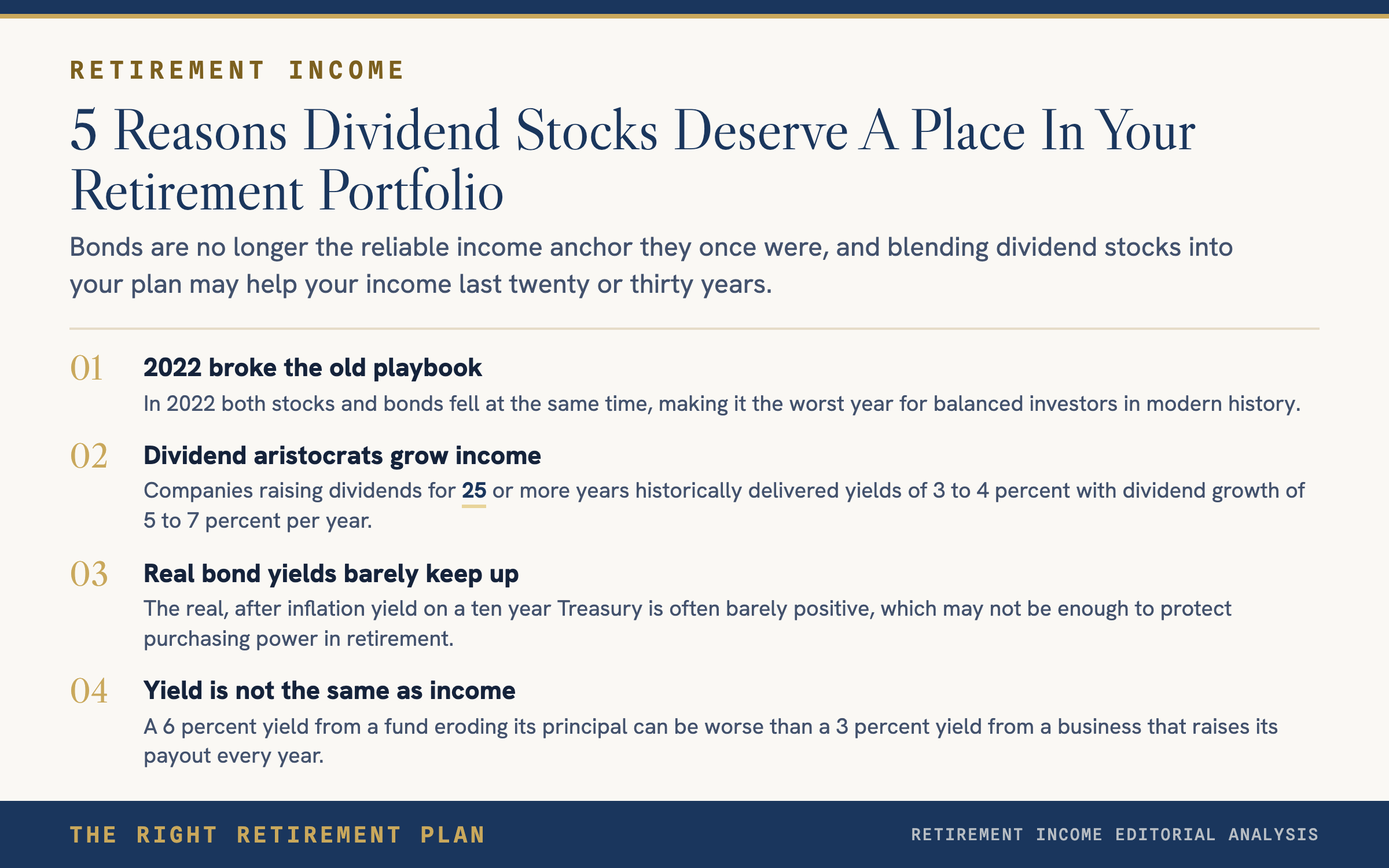

For thirty years, the 60/40 portfolio was retirement gospel. Sixty percent stocks for growth, forty percent bonds for income and ballast. The math worked because bonds paid meaningful interest and moved opposite to stocks when markets wobbled. That world is gone. In 2022 both sides of the portfolio fell at the same time, the worst year for balanced investors in modern history. Since then, Treasury yields have swung hard on every Fed meeting, every war headline, and every inflation print. Retirees need a plan that does not depend on bonds doing what they used to do.

Why Bonds Are Not The Safety Blanket They Used To Be

Bonds are simple. You lend money, you collect interest, you get your principal back. The problem is that two of those three steps are now volatile. Interest rates move in wider ranges than they did a decade ago, which means the market value of your bonds can drop ten or fifteen percent before you ever collect a coupon. Inflation, which spent most of the last thirty years below target, now swings on oil shocks, supply chain shocks, and the kind of war premium that shows up the moment a conflict spreads in Eastern Europe or the Middle East.

The net effect is that the real, after inflation yield on a ten year Treasury is often barely positive. That is not income. That is permission to keep up.

What Dividend Stocks Do Differently

A high quality dividend stock does three things a bond cannot. It pays income that tends to grow. It participates in the long term value of a real business. And it carries no fixed maturity, so rising rates do not force a paper loss on your statement.

Companies that have raised their dividend for twenty five years or more, often called dividend aristocrats, tend to share a common profile. Strong balance sheets, pricing power, and management teams that treat the dividend as a promise rather than a policy. Utilities, consumer staples, healthcare, and a slice of industrials dominate the list. A portfolio built from this group historically produced a yield in the three to four percent range with dividend growth of five to seven percent per year. Over a twenty year retirement, that compounding matters more than the starting yield.

The risk is real but different from bond risk. Dividend stocks can be cut, and share prices fall in a downturn. The protection comes from diversification, dividend coverage, and a willingness to own the business through the cycle rather than trade it.

Blending The Two In Volatile Markets

The answer for most retirees is not to abandon bonds. It is to stop treating them as the only source of defense. A modern income allocation might hold short duration Treasuries or Treasury Inflation Protected Securities for near term spending, a ladder of individual bonds or a short duration fund for the next three to five years, and a broad basket of dividend growth stocks for the income that has to last twenty or thirty years. More retirees across the country are moving toward this blended approach as bond only income plans fall behind the cost of living.

If you want a second set of eyes on your income plan, start with our free Retire Ready Score. It will show you exactly how resilient your current mix is to the next rate shock or geopolitical event.