The one to read first.

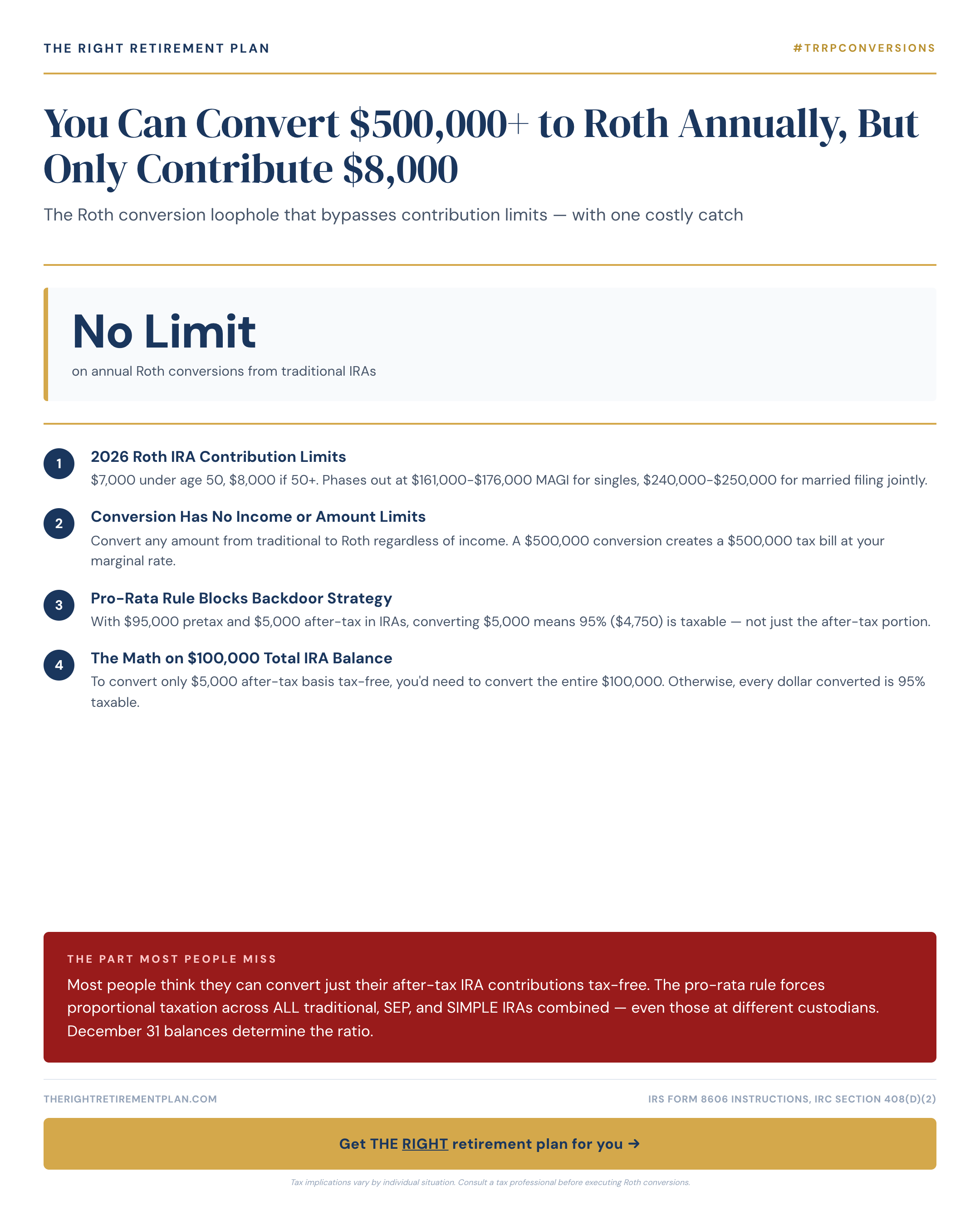

You Can Convert $500,000+ to Roth Annually, But Only Contribute $8,000

Learn how wealthy retirees convert unlimited amounts to Roth IRAs annually while contribution limits cap others at $8,000. The pro-rata rule creates a costly catch most advisors miss.

READ THE GUIDE →All Roth Conversions articles.

9 publishedThe $70,500 Annual Roth Conversion Most High Earners Miss

The mega backdoor Roth allows eligible high earners to convert up to $70,500 annually into tax-free retirement accounts, but only 43% of 401(k) plans offer the required features to make this powerful strategy work.

$500,000 Pretax IRA Converts to $385,000 After-Tax Roth by Age 70

Converting $500K from pretax IRA to Roth during ages 60-70 costs about $115K in taxes but can save $100K+ in lifetime taxes by avoiding the RMD spiral that traps retirees in higher brackets.

Save $200,000 by Converting Your IRA in Florida vs California

Moving from California to Florida before converting a $2M traditional IRA could save over $200,000 in state taxes. Here's what you need to know about strategic state residency planning for major Roth conversions.

A $150,000 Roth Conversion at 63 Costs $5,356/Year Extra in Medicare at 65

A $150,000 Roth conversion at age 63 can trigger Medicare's IRMAA lookback, adding $5,000+ annually to premiums starting at 65. Strategic timing and bracket-aware conversions can save thousands in hidden costs.

Convert $100,000 to Roth at 59? You Can't Touch It Tax-Free Until Age 64

Converting $100,000 to a Roth IRA at age 59 means you can't access those funds penalty-free until age 64 due to the 5-year conversion rule. This hidden timing trap affects thousands of pre-retirees who misunderstand Roth conversion withdrawal rules.

Converting $100K to Roth Today Costs $35K+ in Taxes

High earners considering Roth conversions should think twice if they expect lower retirement income, as converting $100K today could trigger $35K+ in taxes while future withdrawals might face just 12% rates.

Converting $50,000 Annually for 10 Years Could Save $187,000 in Lifetime Taxes

Converting $50,000 annually to a Roth IRA during your 60s could save $187,000 in lifetime taxes by avoiding higher brackets when RMDs begin at age 75.

Backdoor Roth IRA and Roth Conversions Explained

Learn how high-income earners can use backdoor Roth IRAs and Roth conversions to build tax-free retirement income. Key rules, timing tips, and strategies.

The Roth Conversions numbers for 2026.

The thresholds that actually move this part of your plan, kept current and sourced.

See the full reference →Frequently asked.

Social SecurityClaiming strategies, spousal benefits, taxation, and timing.10 articles →

Social SecurityClaiming strategies, spousal benefits, taxation, and timing.10 articles → Tax PlanningBracket math, withdrawal ordering, QCDs, and the tax torpedo.18 articles →

Tax PlanningBracket math, withdrawal ordering, QCDs, and the tax torpedo.18 articles → MedicareParts A/B/C/D, IRMAA, Medigap, and enrollment traps.8 articles →

MedicareParts A/B/C/D, IRMAA, Medigap, and enrollment traps.8 articles → Income PlanningSafe withdrawal rates, buckets, bond ladders, sequence risk.28 articles →

Income PlanningSafe withdrawal rates, buckets, bond ladders, sequence risk.28 articles →Have a question about roth conversions? Ask a real advisor.

No pitch, no pressure. A free conversation with a fiduciary who has read the same research you have.

Book a free conversation