The Conversion Clock Nobody Explains

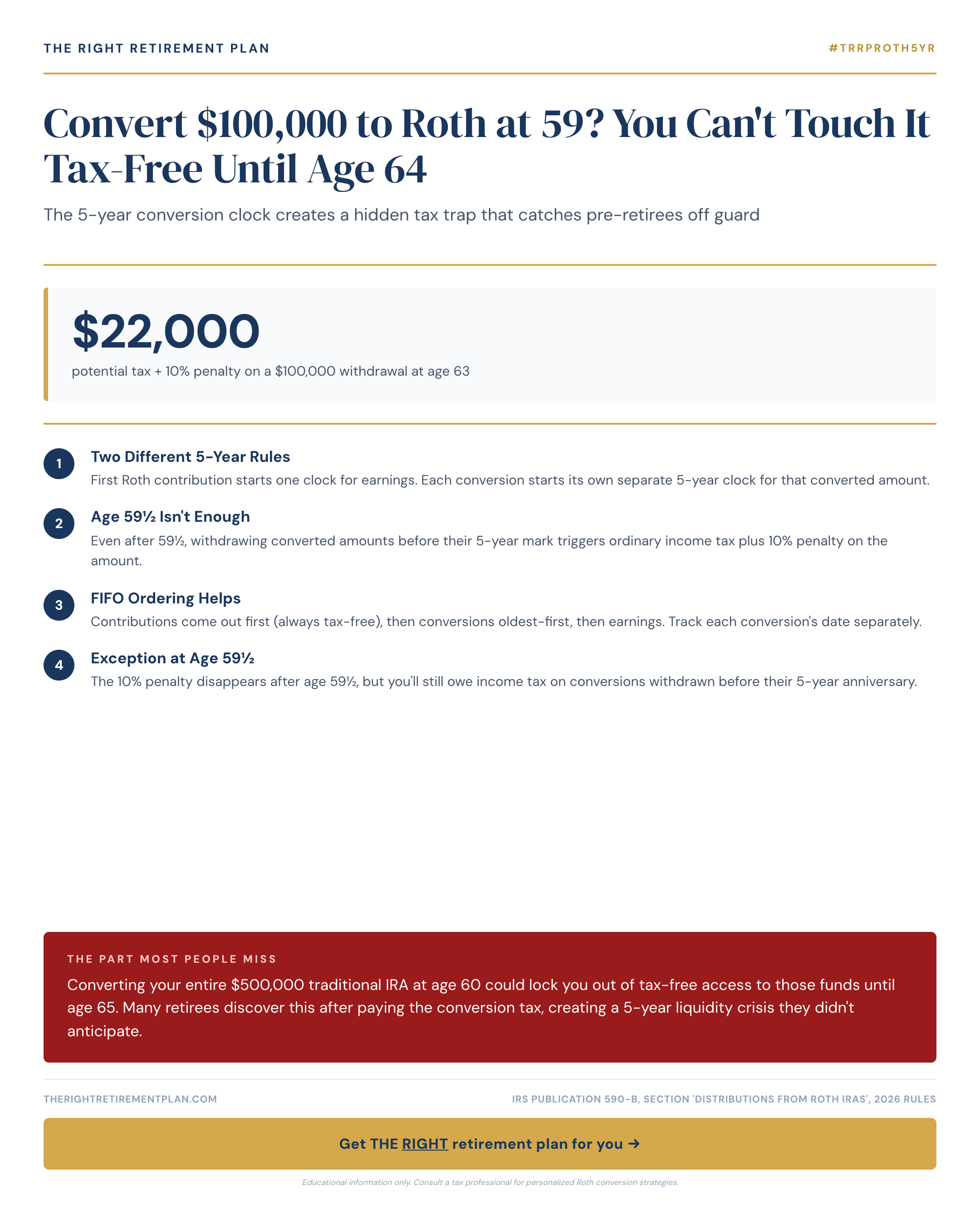

You've done the math on Roth conversions and decided to convert $100,000 from your traditional IRA at age 59. You pay the taxes and assume you now have $100,000 in a tax-free account ready whenever you need it.

Then you discover the 5-year rule, and realize you can't touch those converted dollars without a 10% penalty until you turn 64.

This Roth conversion timing trap catches thousands of pre-retirees every year. The IRS collected over $23 billion in early withdrawal penalties in 2023, with a significant portion coming from retirees who misunderstood conversion withdrawal rules.

How the 5-Year Conversion Rule Actually Works

The IRS maintains two separate 5-year clocks for Roth IRAs, and confusing them causes most planning errors.

The first clock governs when earnings become tax-free. This starts with your first Roth contribution and only needs to begin once in your lifetime.

The second clock applies separately to each Roth conversion. Every conversion has its own 5-year holding period before you can withdraw those specific converted dollars penalty-free if you're under age 59½ at the time of withdrawal.

Here's the critical distinction: if you convert funds and want to withdraw them within 5 years, you'll face a 10% penalty on the converted amount, even if you already paid income tax on the conversion.

Withdrawal order matters:

- First out: Direct contributions (always penalty-free)

- Second out: Converted amounts (oldest conversions first)

- Last out: Earnings (subject to both timing rules)

Convert $100,000 at age 59 and need $30,000 at age 62? You'll owe $3,000 in penalties because that conversion hasn't aged 5 years, regardless of your current age.

Strategic Conversion Timing for Mid-Atlantic Retirees

Many Maryland retirees assume the 5-year rule becomes irrelevant after age 59½. This is only partially true, timing still matters significantly.

The age 59½ exception works differently than most expect:

- Convert at age 58, withdraw at age 60: No penalty (you're over 59½)

- Convert at age 60, withdraw at age 62: 10% penalty applies (conversion under 5 years old)

Smart timing strategies include:

Start early if possible. Begin modest conversions at age 55, and your first batch becomes fully accessible by 60, right when many retirement transitions occur.

Stagger across multiple years. Instead of converting $500,000 in one year and hitting the 37% bracket for 2026, spread conversions over 5-7 years:

| Age | Conversion Amount | Access Date | 2026 Tax Bracket |

|-----|------------------|-------------|------------------|

| 58 | $75,000 | Age 63 | 22% |

| 59 | $75,000 | Age 64 | 22% |

| 60 | $75,000 | Age 65 | 22% |

Maintain separate liquidity. Keep 1-3 years of expenses in taxable accounts during conversion years to avoid forced early withdrawals.

The solution? Make a small Roth contribution in your early 50s, even $1,000, just to start the earnings clock. This single move could mean tax-free growth five years sooner on everything you convert later.

Understanding how Roth conversion timing fits your specific retirement timeline requires examining your complete financial picture. If you want personalized guidance on whether conversion timing could create gaps in your plan, consider taking our Retire Ready Score assessment.