The Real Cost of Your Gym Membership

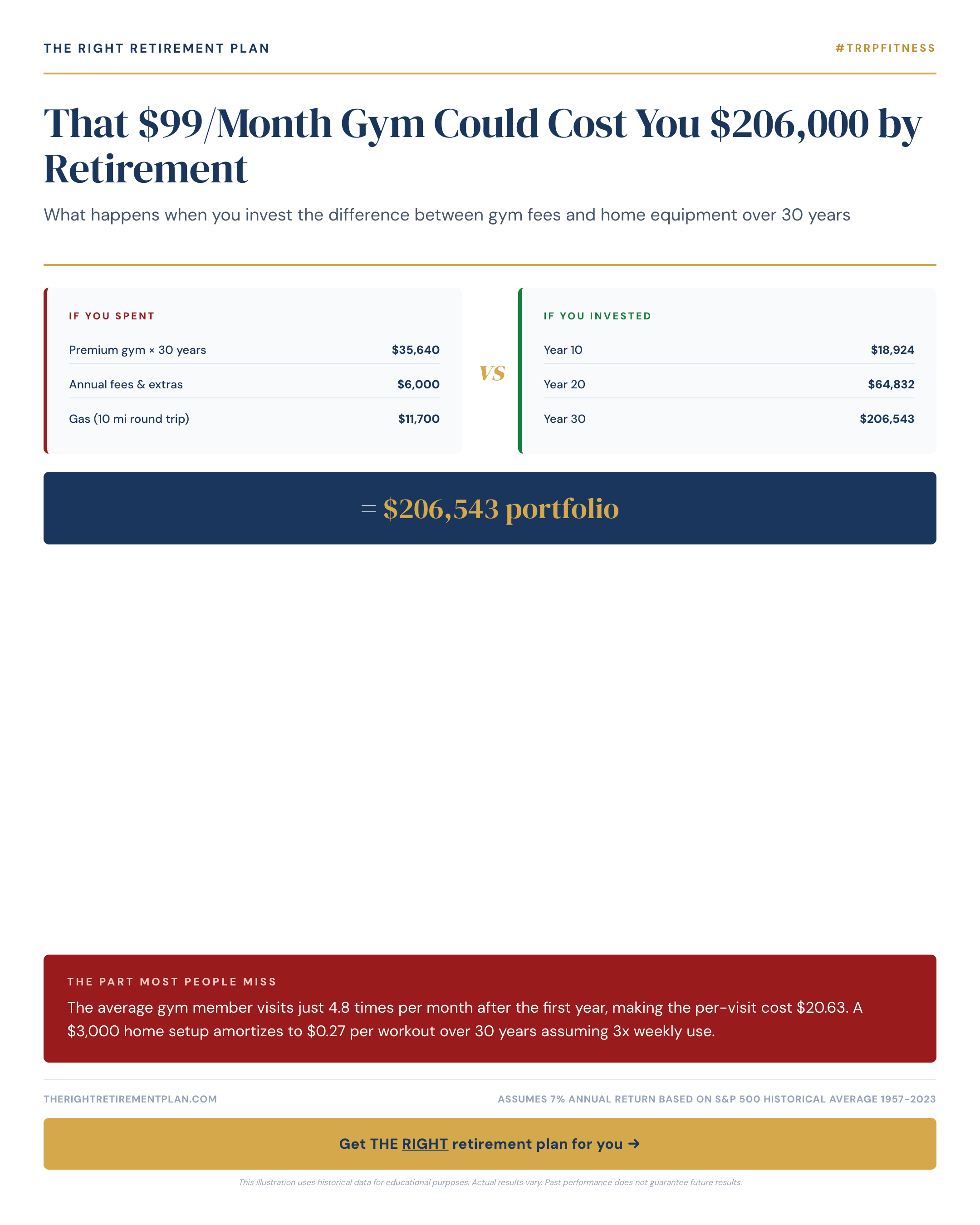

That $99 monthly gym membership seems reasonable until you run the numbers. The average gym member visits just 4.8 times per month after the first year, making each visit cost $20.63. Over 30 years, you'll spend $35,640 in membership fees alone.

But here's where retirement planning gets interesting: what if you invested that money instead?

A quality home gym setup costs around $3,000 upfront. Assuming you work out three times weekly for 30 years, that's just $0.27 per workout. The difference? You save $32,640 that could be earning compound returns in your retirement accounts.

The $206,000 Opportunity Cost

When Maryland retirees invest that $99 monthly gym payment at a 7% annual return over 30 years, it grows to approximately $242,000. Even accounting for the $3,000 home equipment cost, you're looking at a net gain of $206,360.

This isn't just about fitness equipment. It's about understanding how small monthly expenses can derail your retirement security. Every recurring payment represents money that could be working for your future instead of someone else's bottom line.

Consider these retirement-friendly alternatives:

- Resistance bands and dumbbells for strength training

- Streaming fitness classes instead of studio memberships

- Walking groups in your neighborhood

- Home yoga practice with online instruction

Beyond the Gym: A Retirement Planning Lesson

This gym example illustrates a crucial retirement planning principle: small, consistent investments compound dramatically over time. Whether it's gym fees, premium cable packages, or daily coffee shop visits, every expense represents a choice between immediate gratification and future security.

Smart retirement planning means regularly auditing your monthly expenses and asking: "Could this money work harder in my 401(k) or IRA?" The answer might surprise you, especially when you factor in potential tax advantages and employer matching.

The difference between a comfortable retirement and financial stress often comes down to these seemingly minor decisions made consistently over decades.

If you want personalized guidance on optimizing your retirement strategy beyond gym memberships, consider taking our free Retire Ready Score to see how your current plan measures up.