Why The Calendar Just Disappeared

Four months into 2026 and the headlines have outrun the year. Geopolitical conflict, inflation worries, tariff news, an AI infrastructure cycle pulling capital into chips and power, and a market that has reversed itself more than once. The path mattered more than the headline number, and that path is a preview of the rest of the year.

For retirees, the question is not what the market does next. It is whether the plan was built to keep paying income through whatever comes. That is the only useful exercise in May.

The Three Pieces To Confirm Now

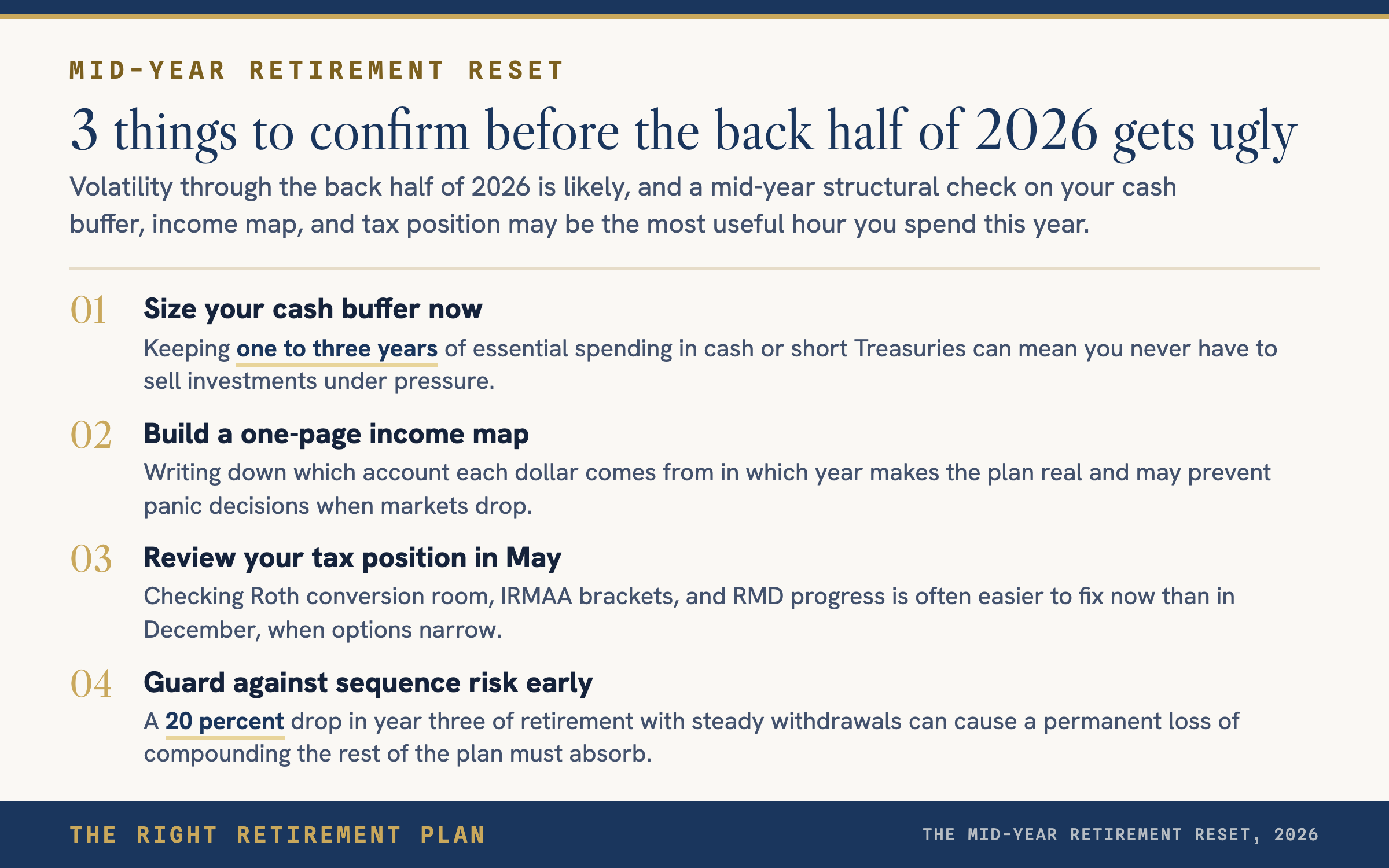

A mid year retirement reset is not a forecast. It is a structural check. Three pieces matter before any other decision.

- Cash buffer. One to three years of essential spending in cash, short Treasuries, or short bond funds. If a 25 percent equity drop forces a sale to fund next month, the buffer is too thin.

- Income map. A one page document that names which account each dollar comes from in which year. If it does not exist on paper, it does not exist when fear shows up.

- Tax position. Capital gains taken so far, Roth conversion room left in the current bracket, IRMAA brackets for next year, and whether RMDs are on track. This is the easiest thing to fix in May and the hardest thing to fix in December.

What The Headlines Cannot Tell You

Headlines describe the market. They do not describe your plan. The Fed is interesting and not actionable. Geopolitics is interesting and not actionable. The shape of the yield curve is interesting and only actionable if your fixed income ladder needs to extend or shorten.

The one place headlines do matter for retirees is sequence of returns risk in the first decade of retirement. A 20 percent drop in year three with steady withdrawals is a permanent loss of compounding that the rest of the plan has to absorb. That is the case for the cash buffer and the bond tent. Not because anyone can predict the next bad quarter, but because the plan has to survive one without selling something.

Frequently Asked Questions

Should I move to cash with this much volatility in 2026?

No. Moving to cash mid year is a market timing decision, and the data on market timing is unkind. The right move is to size the cash buffer correctly so you never have to make that decision under pressure. One to three years of essential spending is the standard.

How often should a retirement plan be reviewed?

A full review at least once a year, with a lighter mid year touch in May or June. Tax law moves, life changes, and asset allocations drift. A plan that has not been touched in three years is already wrong on at least one assumption.

Is the Fed going to cut rates this year?

Maybe. It is the wrong question for your plan. A retirement income strategy that only works at one rate path is fragile. Build it so it works across a reasonable range and you will not need to forecast the meeting.

What are guardrails in a retirement income plan?

Guardrails are pre committed rules that adjust spending up in good years and down in bad ones. They replace the old flat inflation adjustment with a system that flexes with the portfolio, which historically lets retirees take more in normal years without breaking the plan in bad ones.

Is now a good time to do a Roth conversion?

It depends on your bracket, your projected RMDs, and how much room you have left under the next IRMAA tier. The answer is rarely yes or no in isolation. Run the multi year projection before any conversion above five figures.

Take The Next Step

If you want a quick read on whether your current plan would hold up if the rest of 2026 turns ugly, take the free Retire Ready Score. It maps your setup against the five pillars of a complete retirement plan in a few minutes.