The Real Cost of Confusing Activity With Progress

Most investors lose three to four percent a year to themselves, not the market. The cause is mistaking trading activity for smart management. Here is what the data says, and what we do about it.

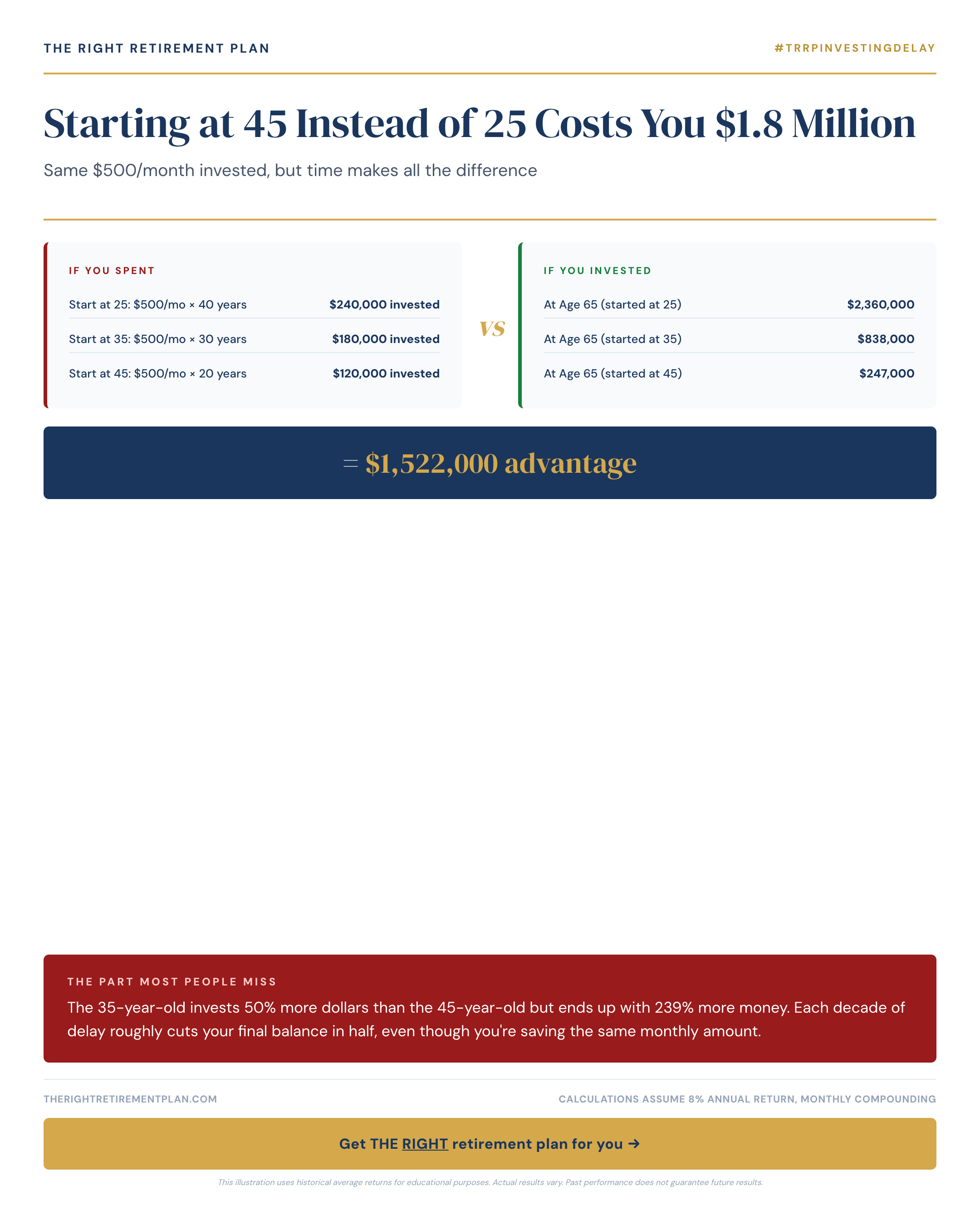

Starting retirement savings at 45 instead of 25 costs the average investor $1.8 million, even with identical monthly contributions. Time and compound growth make all the difference in retirement planning.

The math behind retirement savings timing is sobering. An investor who starts at 25 and contributes $500 monthly until age 65 accumulates approximately $2.1 million. Wait until 45 to begin the same $500 monthly contributions, and you'll end up with just $328,000 by retirement.

That 20-year delay costs you $1.8 million, despite investing the exact same amount each month.

The power of compound growth explains this dramatic difference. When you start at 25, your money has 40 years to grow and compound. Each dollar invested early benefits from decades of market returns building upon previous returns.

Consider these key factors:

If you're starting retirement planning later in life, don't panic. Maryland retirees and others across the Mid-Atlantic have several catch-up options available in 2026:

Starting your retirement planning journey requires understanding these timing dynamics and creating a strategy that maximizes your remaining years until retirement. If you want personalized guidance on how these principles apply to your specific situation, consider taking our Retire Ready Score for a comprehensive assessment.

If you want help building a retirement plan that actually makes sense for your situation, our team at Compound Advisory does this work every day. You can schedule a complimentary review at https://compoundadvisory.co/free-assessment.

Have questions about your specific situation? Take the free Retire Ready Score →

More on money math from the TRRP editorial team.

Most investors lose three to four percent a year to themselves, not the market. The cause is mistaking trading activity for smart management. Here is what the data says, and what we do about it.

Behavioral mistakes cost retirees about 1.2 percent a year. Most of the damage hits in the first five years of retirement, and the fix is structural, not emotional.

The retiree who finishes well is rarely the one who picked the best fund. The pattern shows up in seven habits, none of which require predicting the market.

Our content gives you the knowledge. A qualified advisor can help you act on it.

Take the Free Assessment