Since 2007, Apple has released dozens of iPhone models, each prompting millions of consumers to upgrade. If you bought every major iPhone release since the original, you'd have spent approximately $14,000. But what if you'd invested that money in Apple stock instead?

The Staggering Numbers

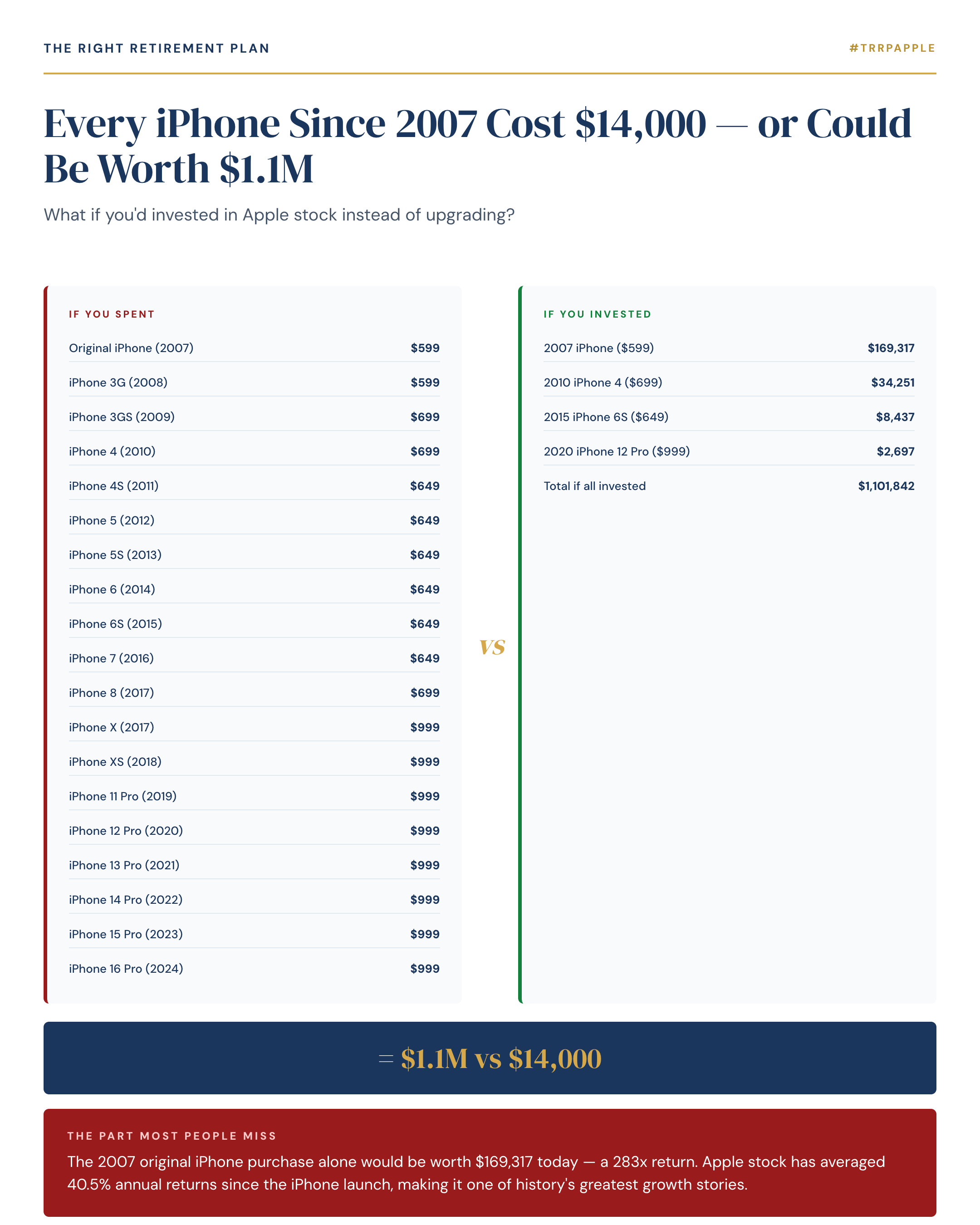

The math is eye-opening. That original $499 iPhone purchase in 2007 would be worth $169,317 today if invested in Apple stock, a 283x return. Apple has delivered an average annual return of 40.5% since the iPhone's launch, making it one of history's most remarkable growth stories.

If you'd consistently invested your iPhone upgrade money into Apple stock over the past 17 years, that $14,000 could have grown to approximately $1.1 million. Even accounting for taxes on gains, you'd be looking at a nest egg that dwarfs the utility of having the latest phone model.

This isn't about hindsight being 20/20, it's about understanding the power of compound growth and opportunity cost.

Why This Matters for Your Retirement Planning

Retirement decisions work the same way. Small choices compound over decades, and getting one detail wrong can cost tens of thousands of dollars. Consider these examples:

- Claiming Social Security at 62 versus full retirement age can reduce lifetime benefits by hundreds of thousands

- Rolling a 401(k) into the wrong type of IRA can trigger unnecessary tax bills

- Choosing the wrong Medicare supplement plan can cost thousands annually

The key insight: Every financial decision has an opportunity cost. When you spend money on something that depreciates (like phones, cars, or luxury items), you're not just losing that money, you're losing what that money could have become through smart investing.

The good news: most costly retirement mistakes are completely avoidable when you understand how the rules actually work and have a clear strategy.

If you want to see how these principles apply to your specific retirement situation, take our free Retire Ready Score, a brief assessment that evaluates your current plan across income, taxes, healthcare, and protection.