A recent $15 million judgment against a retiree following what seemed like a routine fender-bender serves as a stark reminder: standard auto insurance limits won't protect your retirement nest egg from today's supersized lawsuit awards.

Why Retirees Face Higher Lawsuit Risk

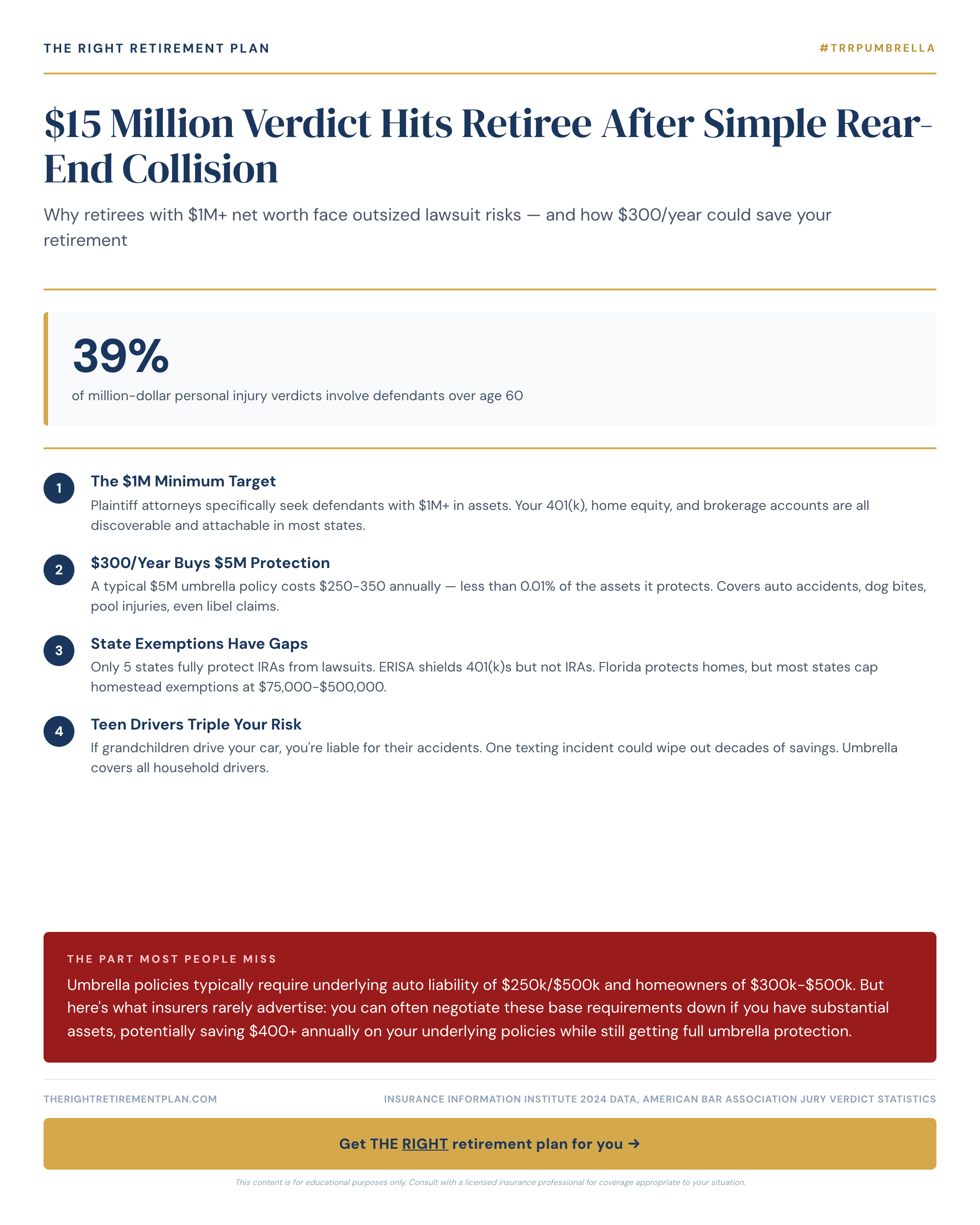

Attorneys specifically target defendants with visible wealth during discovery. If you own rental properties, have substantial investment accounts, or live in an upscale neighborhood, you're painting a target on your back. Maryland retirees, like those in affluent Annapolis communities, are particularly vulnerable given the state's high median home values and retirement account balances.

The math is simple but sobering:

- Most auto policies cap liability at $100,000, $500,000

- Average lawsuit settlements now exceed $1.2 million

- Retirement accounts, home equity, and investment portfolios are all fair game for creditors

This protection gap leaves retirees exposed to losing decades of careful savings in a single legal judgment.

The $300 Solution: Umbrella Insurance

Umbrella insurance provides liability protection beyond your standard auto and homeowners policies. For roughly $200, $400 annually, you can secure $1, $2 million in additional coverage. Higher limits ($5, $10 million) typically cost just $50, $100 more per million.

Here's what most people don't realize: umbrella policies require underlying coverage minimums, typically:

- Auto liability: $250,000/$500,000

- Homeowners liability: $300,000, $500,000

But you can often negotiate these base requirements with your insurer, especially if you demonstrate substantial assets that warrant umbrella protection.

Smart Coverage Strategies

Consider these approaches when shopping for umbrella insurance:

- Bundle with your existing auto/home carrier for discounts

- Increase underlying policy deductibles to offset premium costs

- Review coverage annually as your net worth changes

- Document all assets to ensure adequate protection limits

The peace of mind alone makes umbrella insurance one of retirement's smartest investments. For less than a monthly dinner out, you're protecting everything you've worked decades to build.

If you want personalized guidance on protecting your retirement assets, consider taking our Retire Ready Score to see how your current protection strategy measures up.