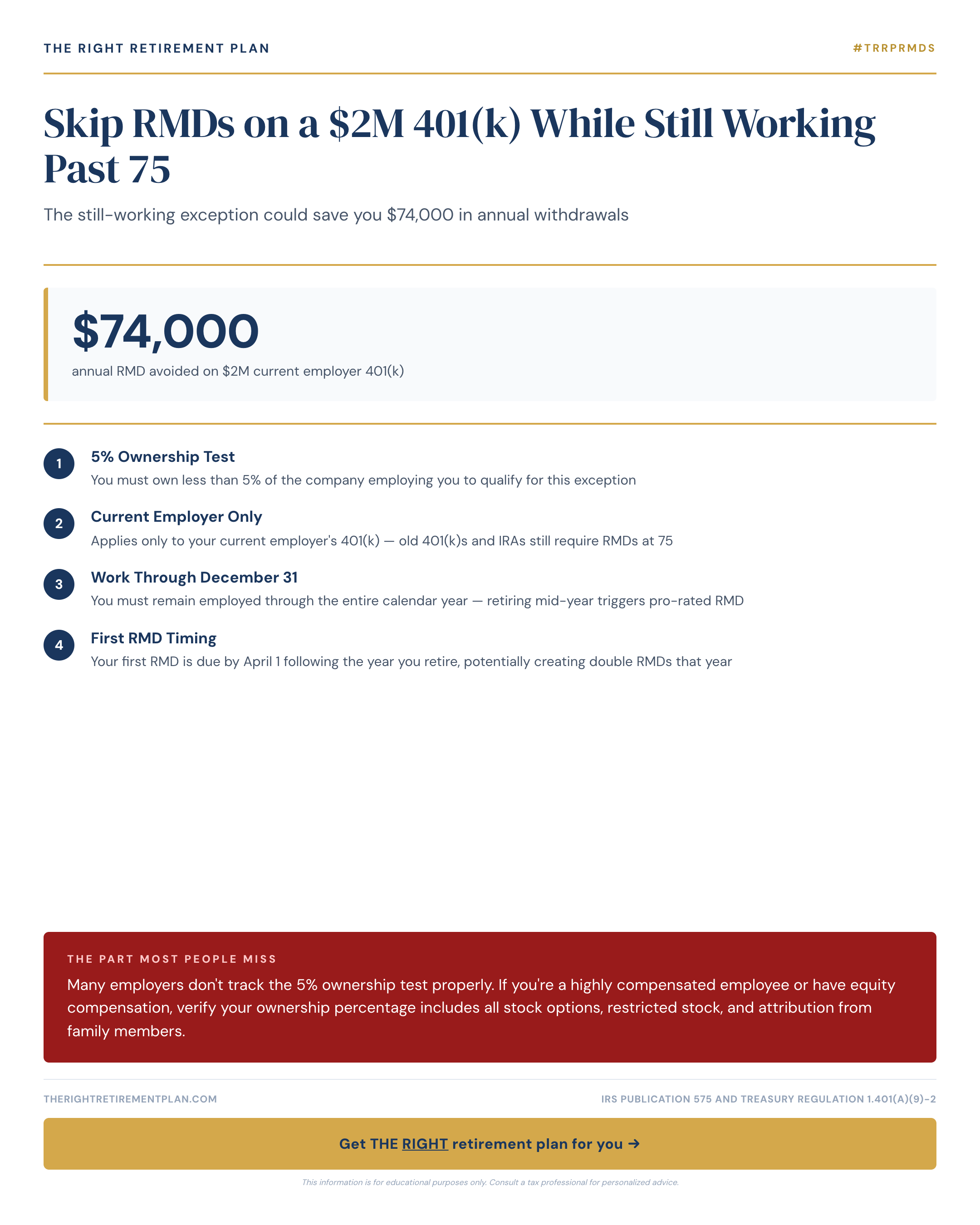

The $74,000 Tax Decision You Might Be Missing

If you're 75 with a $2 million 401(k) and still working, you might assume required minimum distributions are unavoidable. After all, you've passed the SECURE 2.0 Act's RMD age of 73. Time to start withdrawing, right?

Not necessarily. The IRS still-working exception could let you delay RMDs on your current employer's 401(k) indefinitely, as long as you remain employed and meet specific ownership requirements.

On a $2 million balance at age 75, your RMD would be approximately $74,000 using the IRS divisor of 27.0. That's $74,000 you may not need to withdraw, report as ordinary income, or pay federal taxes on at potentially the 24% or 32% bracket.

But this exception has strict rules that trip up even sophisticated investors. Ownership thresholds, rollover timing, and plan document language all determine eligibility.

How the Still-Working Exception Actually Works

The still-working exception applies only to qualified employer retirement plans, 401(k)s, 403(b)s, and certain governmental 457(b) plans, where you're currently employed. It never applies to IRAs, regardless of employment status.

Under IRC Section 401(a)(9)(C), if you're still working for the plan sponsor and own less than 5% of the company, you can delay RMDs until April 1 following the year you actually retire.

Key requirements include:

- Active employment by the plan sponsor (not just consulting fees)

- Less than 5% ownership, including attributed ownership from family

- Plan document permission, not all employers allow this delay

The math makes this valuable. Each year of delay keeps money growing tax-deferred. At age 75, you'd withdraw 3.7% annually. At age 80, that jumps to 4.4%, meaning larger required distributions from a potentially bigger balance.

The 5% Ownership Test That Catches People Off Guard

The ownership threshold extends far beyond shares you personally hold. Under IRC Section 318, your ownership percentage includes:

- Direct stock ownership and preferred shares

- Stock options (both vested and unvested)

- Restricted stock units, even if unvested

- Family attribution: Stock owned by your spouse, children, grandchildren, and parents

Request a formal ownership calculation from HR or legal, specifically including all equity compensation and family attribution.

The Rollover Trap That Triggers Immediate RMDs

Even if you qualify for the still-working exception on your current 401(k), old retirement accounts don't receive protection. This creates a costly mistake.

IRAs and previous employers' 401(k)s never qualify, only your current employer's plan. A 76-year-old with $2 million in their current 401(k) and $1.5 million in an old IRA must still take RMDs on that IRA, generating roughly $57,252 in required distributions.

Some plans segregate rollover contributions and apply standard RMD rules to that portion. Others treat all assets uniformly. This requires careful review of plan documents, potentially years before reaching RMD age.

The question isn't just whether you can delay required minimum distributions, it's whether delaying serves your complete financial picture, including estate planning goals.

If you're weighing RMD timing strategies, our Retire Ready Score can help you evaluate how your current plan performs across taxes, income, and healthcare costs in just two minutes.