Why The Order Of Returns Matters

Two retirees can earn the same average return over 30 years and end up hundreds of thousands of dollars apart. The reason is sequence of returns risk. When withdrawals start, the order of the returns matters as much as the average.

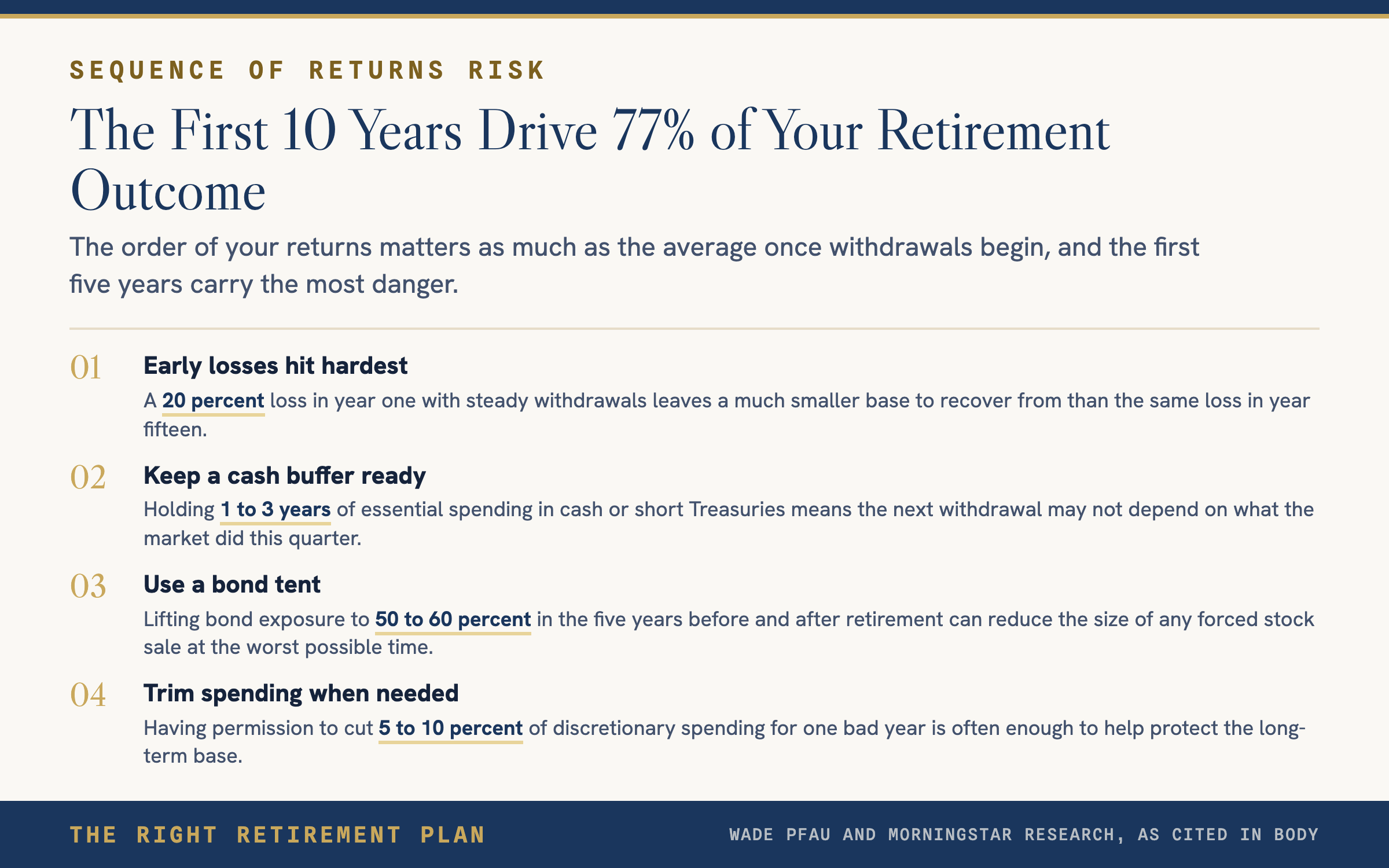

Research from Wade Pfau and Morningstar's buffer asset work consistently lands in the same place. The first five years of retirement carry the most risk, and the first ten years account for roughly 77 percent of the final outcome. A 20 percent loss in year one with steady withdrawals leaves a much smaller base to recover from than the same loss in year fifteen.

This is not a theoretical problem in 2026. The VIX touched 34 in April 2025 and spiked again to nearly 31 in late March 2026. A retiree who began withdrawals during either window and had no plan for selling something other than stocks would have locked in losses at exactly the wrong time.

How To Take Sequence Risk Off The Table

The goal is not to avoid stocks. It is to avoid being forced to sell stocks in a down year. A few patterns show up over and over in plans that hold up.

- Hold 1 to 3 years of essential spending in cash, short Treasuries, or short bond funds, so the next withdrawal does not depend on what the market did this quarter.

- Use a bond tent. Lift bond exposure to 50 to 60 percent in the five years before and after retirement, then drift back toward equities as the danger zone passes.

- Run the plan against a bad sequence scenario, not just an average return. Most retirement calculators default to averages, which understates the real risk in the first three years.

- Keep a flexible income line. When markets fall hard, having permission to trim 5 to 10 percent of discretionary spending for a year is often enough to protect the base.

Frequently Asked Questions

What is sequence of returns risk in plain English?

It is the danger that bad returns hit early in retirement, while you are also pulling money out. Even if the long term average ends up fine, those early losses leave a smaller base for the recovery to compound on.

Why do the first 10 years matter so much?

Research by Wade Pfau and others shows the compounded return in the first decade of retirement explains roughly 77 percent of the final outcome. Forced selling in those years removes capital that would otherwise have been there for the next 20 years.

What is the retirement risk zone?

The retirement risk zone is the roughly 10 year window straddling the retirement date, with the first 5 years inside the zone being the most dangerous. A loss during this window is harder to recover from than the same loss earlier or later.

What is a bond tent and does it actually work?

A bond tent lifts bond allocation to 50 to 60 percent in the years before and just after retirement, then gradually shifts back toward stocks. It reduces the size of any forced sale at the worst possible time, which is the actual mechanism behind sequence risk damage.

How much cash should a new retiree hold?

Most income plans aim for 1 to 3 years of essential spending in cash and short term Treasuries. The exact number depends on Social Security, pensions, and how flexible discretionary spending can be in a bad year.

Take The Next Step

If you want to see how your current plan holds up against a bad first decade, the free Retire Ready Score will walk you through the same lens in a few minutes.