Where The 4 Percent Rule Came From

Bill Bengen's 1994 study tested every 30 year retirement window in modern history and found that a 4 percent starting withdrawal, adjusted for inflation, never ran out of money. That single number became the most quoted rule in retirement planning. It was useful as a sanity check. It was never meant to be a withdrawal policy for an entire 30 year retirement.

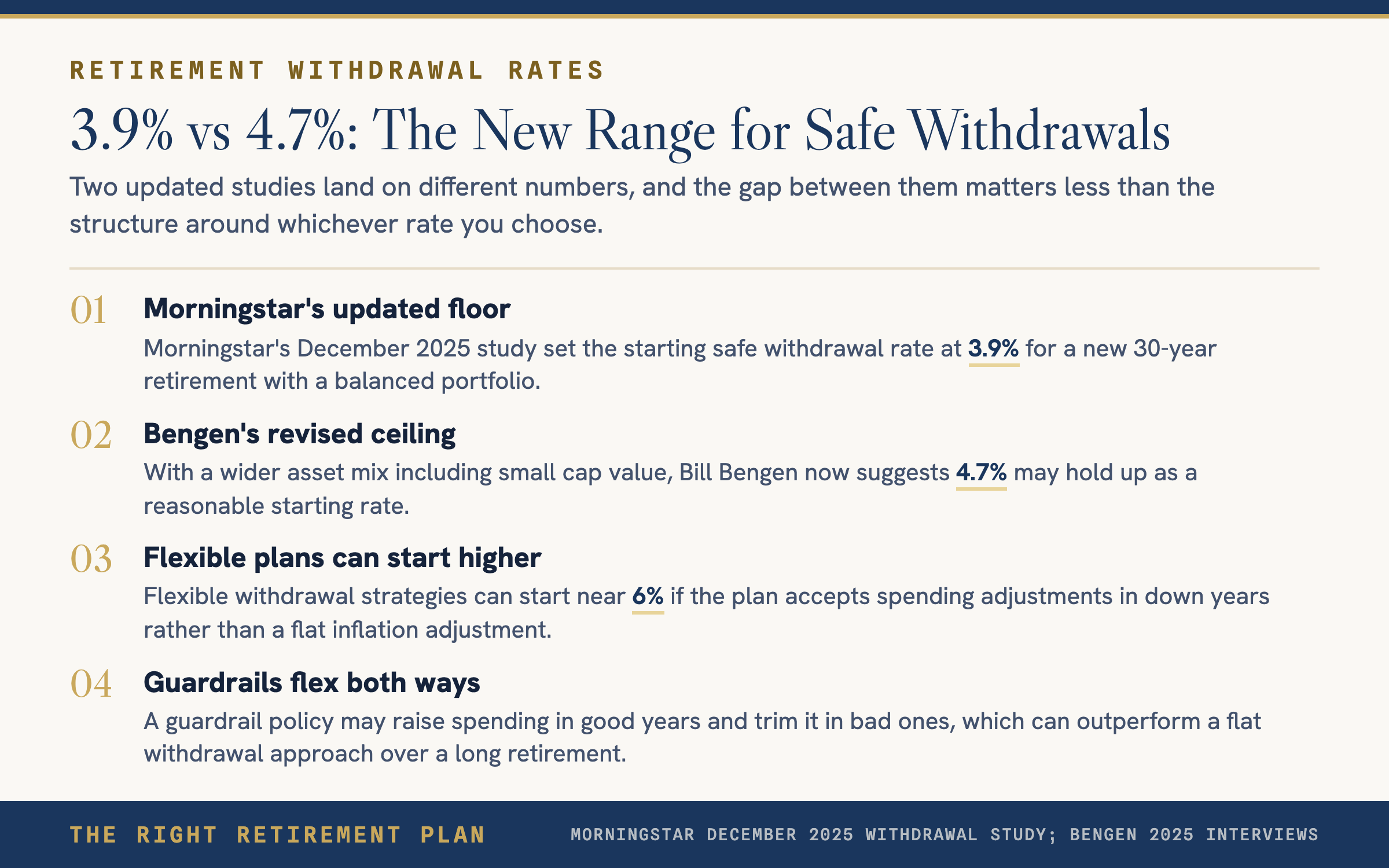

In December 2025, Morningstar updated its annual safe withdrawal study and landed at 3.9 percent for a new retiree with a 30 year horizon and a balanced portfolio. The drop was small but real, driven by current valuations and the actual order of returns since the study began. Bengen himself, in interviews this year, has pushed in the other direction. With a wider mix that includes small cap value, he now suggests 4.7 percent may hold up. Some flexible strategies start near 6 percent and adjust as markets move.

Four different numbers, all defensible, and none of them are the rule for you.

What To Use Instead

A modern income plan does not pick a single number and ride it. It builds in a few moving parts.

- A starting rate anchored to current rates and valuations, not a number from 30 years ago.

- A guardrail policy that quietly raises spending in good years and trims it in bad ones, instead of a flat inflation adjustment.

- A cash and short bond layer that covers 1 to 3 years of essential spending, so a down market never forces a sale.

- A clear distinction between essential spending, which should be funded from stable sources, and discretionary spending, which can flex.

Frequently Asked Questions

Is the 4 percent rule still valid in 2026?

It depends on what you mean. As a fixed withdrawal policy, no, no serious income planner uses it that way. As a starting sanity check, yes. Morningstar's 2025 update lands at 3.9 percent and Bengen's updated work lands at 4.7 percent, so the 4 percent number sits inside a reasonable band.

What is the safe withdrawal rate for 2026?

Morningstar's December 2025 research recommends a 3.9 percent starting rate for a new 30 year retirement with a balanced portfolio. The rate moves up if you accept some spending flexibility, and down if you want a near zero failure probability.

Why did Bill Bengen raise his number?

Bengen revisited the original study with a wider asset mix, particularly small cap value, and found a higher historical safe rate of about 4.7 percent. The original 4 percent was always the worst case in his data, not the typical case.

What is a guardrail withdrawal strategy?

A guardrail policy adjusts spending in response to portfolio performance. If the portfolio rises past an upper guardrail, spending bumps up. If it falls past a lower guardrail, spending trims. It captures more upside without breaking on the downside.

Should I use 3.9, 4, or 4.7 percent for my plan?

That is the wrong question. The right question is whether the plan still works through a bad sequence, a long retirement, and realistic taxes. The starting rate is one input. The structure around it is what makes it survive.

Take The Next Step

If you want a clean read on whether your current plan is built around one number or all of them, take the free Retire Ready Score. It maps your setup against the five pillars of a complete retirement plan in a few minutes.