The Bucket Strategy, How Retirees Keep Paying Themselves When Markets Get Wild

Every retirement plan eventually meets a bad market. Sometimes it is a banking crisis, sometimes an inflation spike, sometimes a war that nobody saw coming two weeks earlier. The question is not whether a downturn will hit your plan. The question is whether your plan has a way to keep paying you through it without selling at the worst possible time. The bucket strategy is the simplest, most durable answer we have.

What A Bucket Strategy Actually Looks Like

Instead of one big portfolio with one blended return, the bucket approach divides your savings into three pools based on when you will spend the money.

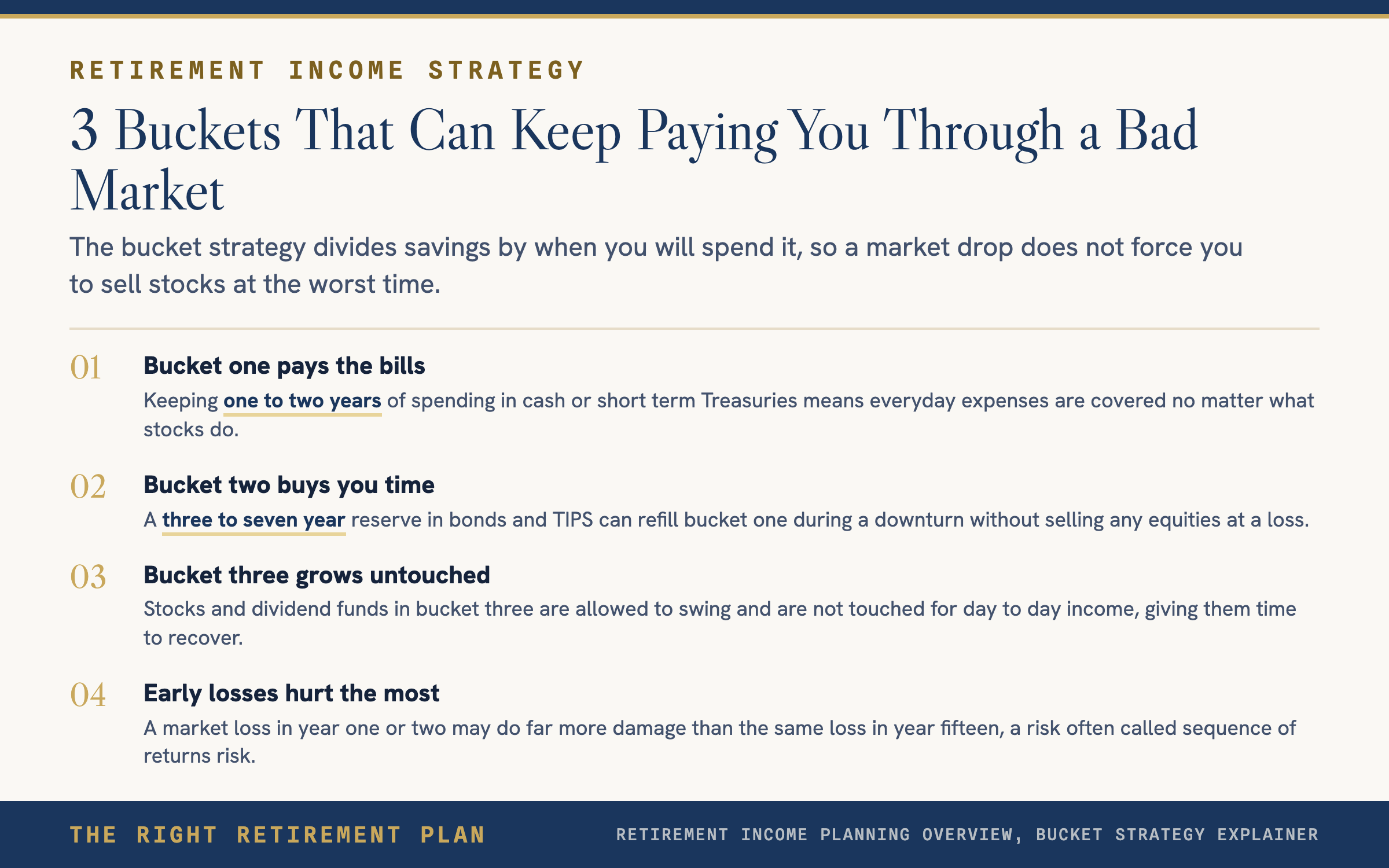

The first bucket holds one to two years of spending in cash, high yield savings, or short term Treasuries. It pays the bills. It does not grow much. It is not supposed to.

The second bucket holds three to seven years of spending in short and intermediate bonds, Treasury Inflation Protected Securities, and conservative income funds. It generates steady interest and is stable enough to refill bucket one without selling stocks at a loss.

The third bucket holds everything else, the long term growth engine. This is where stocks, dividend funds, and other equity exposure live. It is allowed to swing. It is expected to swing. It is not touched for day to day income.

The buckets are refilled on a schedule. In good years, profits from bucket three get moved down to refill bucket two. In bad years, the system stays still. You live off buckets one and two while bucket three recovers. That small shift removes the single most destructive behavior in retirement investing, selling stocks after they have already fallen.

Why It Works Against Sequence Of Returns Risk

The first five years of retirement are the most dangerous. A market loss in year one or two does far more damage than the same loss in year fifteen because every withdrawal during a downturn locks in a permanent drag on the portfolio. This is called sequence of returns risk, and it is the real reason retirements fail.

The bucket strategy tames sequence risk because it decouples your spending from the stock market. When the S and P drops twenty percent, your bucket one is still full of cash. Your bucket two is still paying interest. You never have to sell the equity pool to eat. By the time you would need to refill, history suggests markets have usually recovered. Not always on the same timeline, but often enough that a two to seven year reserve is a very high probability cushion.

Calibrating The Buckets To Your Plan

The right sizing depends on three variables. Your annual spending net of guaranteed income such as Social Security and pensions. Your risk tolerance. And the current yield environment. In a year when short term Treasuries pay four or five percent, a larger bucket two makes sense because you are actually being paid to wait. In a year when yields are below inflation, bucket two shrinks and bucket three picks up more of the long term load.

Many of the retirees we work with run a five year reserve combined with a growth pool weighted toward dividend payers. It keeps the income stable, reduces stress, and lets the long term money do its job.

If you would like to see how well your current plan would hold up against a bad sequence of returns, take our free Retire Ready Score. It pressure tests your income plan against the kind of markets we have actually been living in.