The Best States To Retire In 2026, A Full Ranking Of All 50 With Taxes, Weather, Healthcare And Family Access

Where you retire changes almost every number on your plan. Two identical retirees with the exact same portfolio can end up tens of thousands of dollars apart each year depending on which state signs the paychecks. That gap compounds across a twenty or thirty year retirement. The right state also shapes the softer parts of the picture, the climate you live in, the community you find, the hospital system that will take care of you, and how easy it is for your kids and grandkids to get to you.

This is a long post because the decision deserves a long look. We ranked every state using five factors that actually matter in retirement, built a tax framework based on your income level, flagged the states where recent law changes are a big deal, and added a short list for retirees who want to stay in a city. All figures are current as of 2026 and sourced from public data, not opinion.

The Five Factors We Used To Rank Every State

1. Taxes that hit retirees specifically, including state income tax, Social Security taxation, pension and IRA treatment, estate and inheritance taxes. Source data from the Tax Foundation 2026 State Tax Competitiveness Index, Kiplinger state-by-state retirement tax guide, and the ACTEC State Death Tax Chart.

2. Cost of living, using the MERIC Cost of Living Data Series and BEA Regional Price Parities.

3. Healthcare quality for seniors, using the America's Health Rankings 2025 Senior Report and the Commonwealth Fund state scorecards.

4. Climate and natural disaster risk, using NOAA billion dollar disaster data and the FEMA National Risk Index.

5. Community fit and family access, meaning is there an existing retiree community for you, and can your adult kids actually get to you in a day. This is softer but real.

The Tax Picture By Income Level, Because The Same State Is Not Equal For Everyone

The state that is best for a $70,000 a year retiree is often not the state that is best for a $250,000 a year retiree. A lot of the recent state tax changes only kick in at certain income levels, so the smart move is to run the comparison for your own number, not a national average.

Roughly $40,000 to $80,000 In Retirement Income

This is the sweet spot for state tax relief. Every state that still taxes Social Security, Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, and Vermont, has an income based exemption that almost always covers a retiree in this band. In practice, households here rarely pay state tax on their Social Security anywhere.

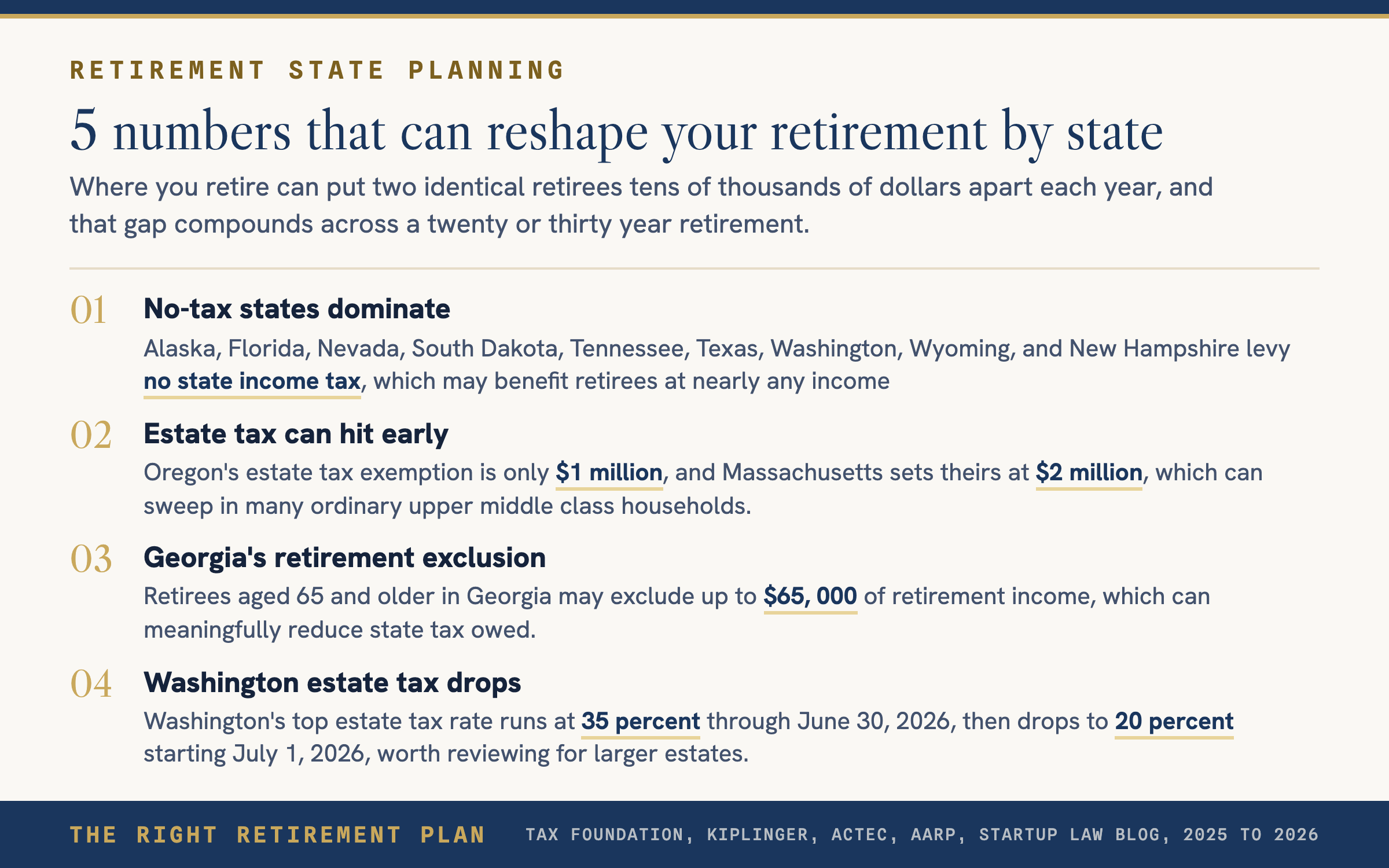

At this income level the states that shine are the ones with no income tax at all (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, Wyoming) plus states with generous pension exclusions like Illinois, Mississippi, and Pennsylvania which exempt retirement income entirely, or Georgia which excludes up to $65,000 of retirement income at 65 and older. Source: Kiplinger's 50 state retirement tax guide.

Roughly $80,000 to $200,000

This is where states start to separate. Above about $100,000 of combined income, retirees in Minnesota, Rhode Island, and Vermont begin owing real state tax on Social Security. Connecticut phases out its exemption above $75,000 single and $100,000 joint. Colorado is now a clean exemption at 65 and older, which is a recent and meaningful win for retirees in that band (source: AARP Colorado).

At the same time, the state income tax rate itself becomes a bigger issue. A 10 percent top rate in California, Hawaii, New Jersey, New York, or Oregon costs real money at this income level. Flat tax, low rate states like North Carolina (3.99 percent, dropping), Arizona (2.5 percent), Indiana (3 percent), and Pennsylvania (3.07 percent) start to look very attractive.

Above $200,000 And For Larger Estates

Here the estate tax question becomes as important as the income tax question. Twelve states plus DC still levy an estate tax, and the exemptions range from Connecticut's $13.99 million (matching the federal limit) down to Oregon's $1 million and Massachusetts's $2 million, which sweep in a lot of ordinary upper middle class households. Washington runs the highest top estate rate in the country, currently 35 percent, dropping back to 20 percent on July 1, 2026 (source: Startup Law Blog on the Washington rollback).

Five states levy an inheritance tax, which is paid by the person inheriting: Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. Maryland is the only state with both an estate tax and an inheritance tax. Iowa repealed its inheritance tax effective January 1, 2025 (source: Tax Foundation estate and inheritance map).

For larger estates, moving from Oregon to Washington to a no estate tax state like Florida, Texas, or Nevada can save seven figures, but residency must be real and documented, not a drivers license swap.

Our Composite Top Ten For 2026

We blended tax friendliness, cost of living, healthcare, climate risk, and community access. The rankings roughly agree with consensus picks from Bankrate, WalletHub, Kiplinger, and Forbes, with adjustments where those lists underweight recent law changes.

1. Wyoming. No income tax, no estate tax, no inheritance tax, low cost of living. WalletHub ranked Wyoming number one for 2026. Thin population means healthcare access can be hard outside Cheyenne or Casper, but the tax math is unmatched.

2. Florida. No income tax, no estate tax, huge retiree community, warm climate year round. The real cost is hurricane exposure and a property insurance market in crisis. For retirees who can self insure or accept higher premiums, Florida still delivers.

3. South Dakota. Kiplinger's number one for 2026. No income tax, no estate tax, low cost of living, strong financial privacy laws for trusts. Cold winters are the obvious offset.

4. Tennessee. No income tax, no estate tax, low cost of living, growing metro areas like Nashville and Knoxville, and a mild climate by national standards. Tornado risk is real.

5. New Hampshire. Bankrate's number one for 2025. No income tax after the 2025 repeal of the interest and dividends tax, excellent healthcare, four real seasons. High property taxes are the trade.

6. Nevada. No income tax, no estate tax, Las Vegas and Reno amenities, growing 55 plus communities. Water stress and summer heat are long term concerns.

7. Texas. No income tax, lots of retiree friendly cities, low grocery costs. High property tax and hurricane exposure on the Gulf offset the savings for some retirees.

8. Mississippi. A budget pick. Lowest cost of living in the country, full exemption of retirement income, no estate tax. Healthcare quality is a real weakness, so it works best for retirees willing to travel for specialty care.

9. Pennsylvania. Full retirement income exemption at retirement age, low 3.07 percent flat rate, walkable cities like Pittsburgh. The inheritance tax is the offset, though lineal heirs pay only 4.5 percent.

10. Utah. Kiplinger's number one for retiree happiness. Outdoor lifestyle, strong healthcare, growing infrastructure. The Social Security tax credit phases out, so higher income retirees lose that benefit, and cost of living is rising fast.

Honorable mentions: Idaho, North Carolina, South Carolina, Georgia, and Delaware all do well for different reasons.

All 50 States, Quick Take

Each line shows the essentials: state income tax treatment, Social Security treatment, estate or inheritance tax, and the single headline fact that moves the decision. Always verify against your state's department of revenue before making a permanent move.

1. Alabama. Flat 5 percent income tax. Social Security exempt. No death tax. Defined benefit pensions fully exempt, though 401(k) and IRA withdrawals are taxed. Low cost of living, weak rural healthcare.

2. Alaska. No income tax, no Social Security tax, no death tax. High grocery and heating costs, and healthcare access is thin outside Anchorage.

3. Arizona. 2.5 percent flat income tax. Social Security exempt. No death tax. Popular Sun Belt destination. Extreme summer heat and wildfire exposure.

4. Arkansas. Graduated to 3.9 percent. Social Security exempt. No death tax. $6,000 retirement income exclusion. Low cost, tornado risk.

5. California. Graduated to 13.3 percent, the highest in the country. Social Security exempt. No death tax. High cost of living and climate risk offset the exempt Social Security.

6. Colorado. Flat 4.4 percent. Taxes Social Security but now fully exempts it for taxpayers 65 and older. No death tax. $24,000 pension deduction at 65 and older.

7. Connecticut. Graduated to 6.99 percent. Income based Social Security exemption. Estate tax with a high $13.99 million exemption. High cost but strong healthcare.

8. Delaware. Graduated to 6.6 percent. Social Security exempt. No death tax. No sales tax. $12,500 pension exclusion at 60 and older.

9. Florida. No income tax. Social Security exempt. No death tax. Hurricane and insurance risk are the real cost.

10. Georgia. 5.19 percent flat. Social Security exempt. No death tax. Up to $65,000 retirement income exclusion at 65 and older.

11. Hawaii. Graduated to 11 percent. Social Security exempt. Estate tax with $5.49 million exemption. Employer pensions exempt. Highest cost of living in the country.

12. Idaho. Flat 5.3 percent. Social Security exempt. No death tax. Bankrate top five. Growing fast, wildfire exposure.

13. Illinois. Flat 4.95 percent. Social Security exempt. Estate tax with $4 million exemption, no inflation indexing. All retirement income fully exempt. High property taxes.

14. Indiana. Flat 3 percent. Social Security exempt. No death tax. Simple, low rate, no special retirement breaks.

15. Iowa. Flat 3.8 percent. Social Security exempt. No death tax as of January 1, 2025. All retirement income exempt at 55 and older.

16. Kansas. Graduated income tax. Social Security tax eliminated for tax year 2024 and beyond. No death tax. Tornado risk.

17. Kentucky. Flat 4 percent. Social Security exempt. Inheritance tax with Class A (spouse and children) exempt. $31,110 pension exclusion.

18. Louisiana. Graduated to 4.25 percent. Social Security exempt. No death tax. High hurricane and flood exposure, expensive insurance.

19. Maine. Graduated to 7.15 percent. Social Security exempt. Estate tax around $7 million. Bankrate number two for 2025. Mild summers, cold winters.

20. Maryland. Graduated to 5.75 percent. Social Security exempt. Both estate tax ($5 million) and inheritance tax. Only state in the country with both. Strong healthcare.

21. Massachusetts. Flat 5 percent plus a 4 percent millionaire surtax. Social Security exempt. Estate tax with a $2 million exemption, second lowest in the country. Top tier healthcare. High cost.

22. Michigan. Flat 4.25 percent. Social Security exempt. No death tax. 2026 pension and 401(k) exemption up to $67,610 single and $135,220 joint.

23. Minnesota. Graduated to 9.85 percent. Taxes Social Security but exempts it fully for AGI up to about $82,000 single and $105,000 joint. Estate tax with $3 million exemption. Kiplinger's number one for senior healthcare.

24. Mississippi. Flat 4.4 percent. Social Security exempt. No death tax. All retirement income exempt. Cheapest state to live in. Weak healthcare infrastructure.

25. Missouri. Flat 4.7 percent. Social Security tax eliminated for tax year 2024. No death tax. Tornado risk.

26. Montana. Graduated to 5.9 percent. Partially taxes Social Security. No death tax. Outdoor lifestyle, limited specialty healthcare.

27. Nebraska. Graduated to 5.2 percent. Social Security fully phased out 2024. Inheritance tax still in place.

28. Nevada. No income tax. Social Security exempt. No death tax. Las Vegas and Reno amenities. Water and heat issues long term.

29. New Hampshire. No income tax. Social Security exempt. No death tax. Bankrate number one for 2025. High property taxes.

30. New Jersey. Graduated to 10.75 percent. Social Security exempt. Inheritance tax. Generous retirement income exclusion if income is under $100,000. High cost of living.

31. New Mexico. Graduated to 5.9 percent. Taxes Social Security but exempts it below $100,000 single and $150,000 joint. No death tax. Low cost, limited specialty healthcare.

32. New York. Graduated to 10.9 percent. Social Security exempt. Estate tax around $7.16 million. $20,000 pension exclusion for private pensions at 59 and a half. Public pensions fully exempt. High cost.

33. North Carolina. Flat 3.99 percent, scheduled to drop to 2.99 percent by 2028. Social Security exempt. No death tax. Pensions fully taxed. Mild inland climate, hurricanes on the coast.

34. North Dakota. Graduated to 2.5 percent. Social Security exempt. No death tax. Harsh winters, low tax burden.

35. Ohio. Graduated to 3.5 percent. Social Security exempt. No death tax. Retirement income credit up to $200. Affordable Midwest option.

36. Oklahoma. Graduated to 4.75 percent. Social Security exempt. No death tax. Among the cheapest in the country. Tornado alley. Weak healthcare rankings.

37. Oregon. Graduated to 9.9 percent. Social Security exempt. Estate tax with the lowest exemption in the country at $1 million, which sweeps in many middle class estates. No sales tax.

38. Pennsylvania. Flat 3.07 percent. Social Security exempt. Inheritance tax. Spouses and lineal heirs pay 0 percent or 4.5 percent. All retirement income exempt at retirement age. Pittsburgh and Philadelphia offer walkable urban life.

39. Rhode Island. Graduated to 5.99 percent. Income based Social Security exemption. Estate tax with $1.80 million exemption. Bankrate top ten.

40. South Carolina. Graduated to 6.2 percent. Social Security exempt. No death tax. $10,000 and $15,000 retirement deductions. Coastal hurricane risk.

41. South Dakota. No income tax. Social Security exempt. No death tax. Kiplinger number one for 2026. Cold winters.

42. Tennessee. No income tax. Social Security exempt. No death tax. Growing metros, low cost of living, tornado risk.

43. Texas. No income tax. Social Security exempt. No death tax. High property taxes. Hurricane and heat exposure.

44. Utah. Flat 4.55 percent. Taxes Social Security via a credit that phases out. No death tax. Outdoor lifestyle, strong healthcare. Rising cost of living.

45. Vermont. Graduated to 8.75 percent. Income based Social Security exemption. Estate tax with $5 million exemption. Bankrate number four. Beautiful, expensive, strong healthcare.

46. Virginia. Graduated to 5.75 percent. Social Security exempt. No death tax. $12,000 age 65 deduction, income tested. Moderate cost, Bankrate top ten.

47. Washington. No income tax except 7 percent capital gains above about $270,000. Social Security exempt. Estate tax at 35 percent top rate through June 30, 2026, then 20 percent starting July 1, 2026. Exemption around $3 million.

48. West Virginia. Graduated to about 4.82 percent. Social Security fully exempt for tax year 2026. No death tax. Bankrate top ten. Rural healthcare is weak.

49. Wisconsin. Graduated to 7.65 percent. Social Security exempt. No death tax. Bankrate top ten. Madison and Milwaukee offer urban amenities. Cold winters.

50. Wyoming. No income tax. Social Security exempt. No death tax. WalletHub number one. Lowest overall retiree tax burden in the country. Low population and healthcare thin outside the cities.

For City Dwellers, Urban Life In Retirement

Not every retiree wants to move to a golf course community. For the retiree who wants a walkable downtown, a real art scene, public transit, and strong healthcare, tax haven states are often the wrong answer, because the big upsides there come with low density. These are the cities we keep seeing on 2025 and 2026 best places to retire lists that combine urban amenities with a workable tax profile.

- Pittsburgh, Pennsylvania. UPMC healthcare system, neighborhoods with real character, affordable cost of living. Pennsylvania exempts all retirement income at retirement age.

- San Antonio, Texas. Low cost in a major metro, no state income tax, walkable River Walk and King William districts.

- Asheville, North Carolina. Blue Ridge setting, four mild seasons, independent arts and food scene, growing healthcare access. North Carolina exempts Social Security.

- Tampa and St. Petersburg, Florida. No income tax, no estate tax, warm climate, improving walkability, with the Florida caveat on hurricane and insurance risk.

- Raleigh, North Carolina. Research Triangle hospitals, cultural amenities, moderate climate, growing retiree population.

- Charleston, South Carolina. Historic walkable core, coastal lifestyle, $15,000 senior retirement deduction. Hurricane exposure offsets some appeal.

- Greenville, South Carolina. Revitalized downtown, cost of living 9 percent below national average, Blue Ridge access.

- Madison, Wisconsin. College town amenities, top healthcare, walkable. Wisconsin does tax retirement income, so run the numbers.

- Portland, Maine. Walkable waterfront, strong food scene, New England healthcare network.

- Lexington, Kentucky. Horse country, affordable, Kentucky's $31,110 pension exclusion, University of Kentucky medical center.

Climate Risk Is A Retirement Risk Too

A hurricane that takes your roof in year three of retirement can reroute your plan. The NOAA billion dollar disaster database recorded 23 billion dollar disasters in 2025 alone. Hurricane exposure is concentrated in Florida, Louisiana, Texas, the Carolinas, Alabama, and Mississippi. Wildfire exposure is concentrated in California, Oregon, Washington, Colorado, Arizona, New Mexico, Idaho, and Montana. Tornado risk is highest across Oklahoma, Kansas, Texas, Missouri, Arkansas, Tennessee, Mississippi, Alabama, and Georgia. Insurance markets have pulled back in Florida, California, and Louisiana, which matters enormously for retirees on a fixed income.

Community And Family Access, The Soft Factors That Become Hard Factors

Two things consistently show up in retiree satisfaction research. First, having a local community of people roughly your age and stage, whether that is a 55 plus development, a church, a university town, or a dense neighborhood of long term residents. Second, being in reasonable reach of adult children and grandchildren. A two hour direct flight beats a three leg itinerary through a hub every time. Before finalizing a state, look at your top three cities on a flight map from your kids' home airports. Small differences in travel time translate into real differences in how often you actually see them.

The best state for you is rarely the one at the top of any single list. It is the one that lines up your income level, your estate size, your health needs, and where your family actually is.

If you want a structured way to stress test your plan against the state you are in now and the state you are thinking about, take our free Retire Ready Score. It is built to compare tax, income, and longevity scenarios across different states so you can see the math before the move.