For most retirees and pre-retirees, taxes quietly rank as the single largest annual expense. Federal income tax, state income tax, capital gains tax, property tax, and Medicare surcharges all add up. The total is often bigger than a mortgage payment, yet most households spend far less time managing taxes than they do shopping for a better rate on a savings account.

The worst part? Many people are paying more than they legally owe, simply because no one showed them the alternatives.

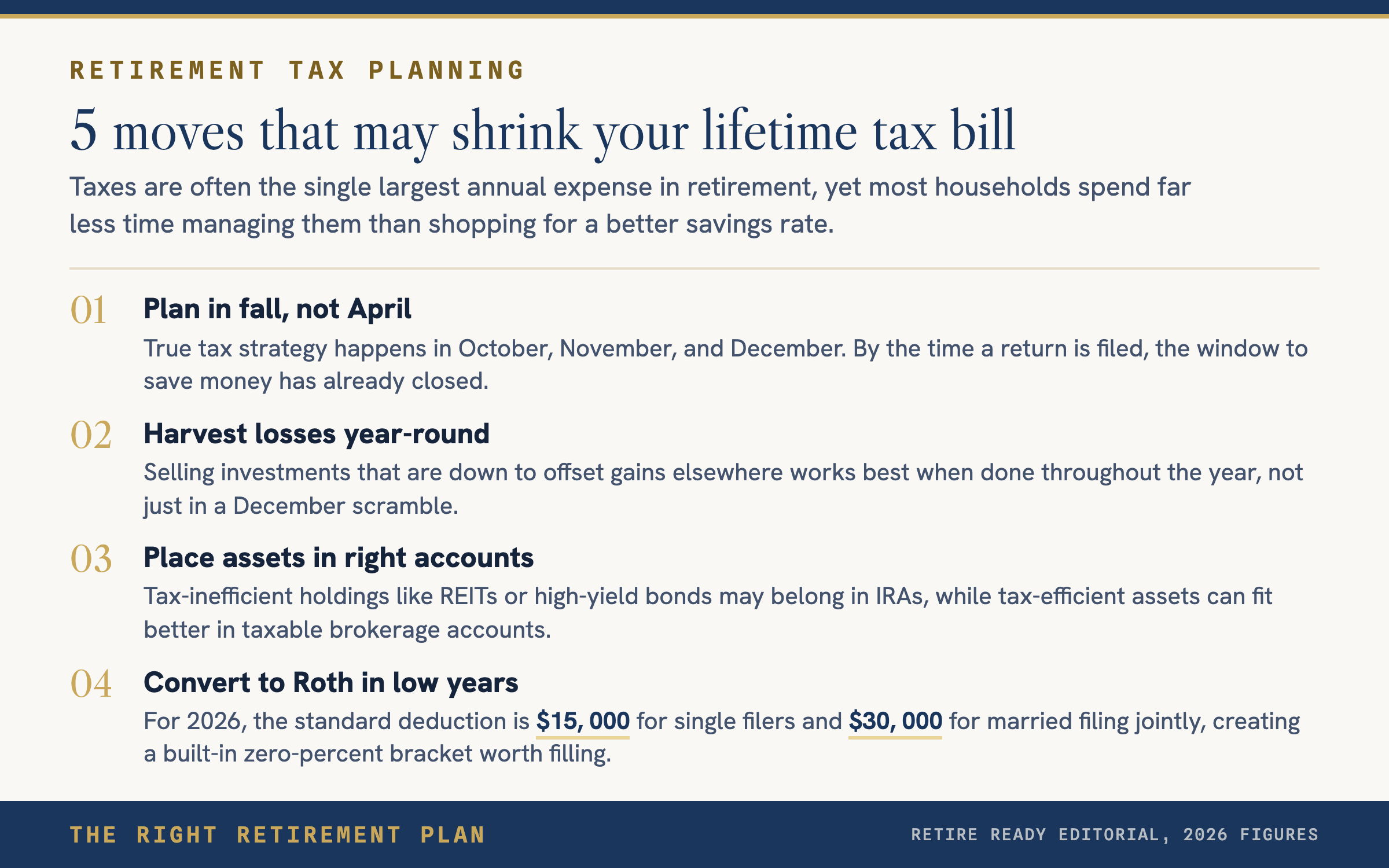

Tax Preparation Is Not Tax Planning

Most people think tax planning is what happens in April when a CPA says how much is owed. That is tax preparation, not tax strategy. By the time a return is filed, the window to save money has already closed.

True retirement tax planning is proactive. It happens in October, November, and December, not the night before the filing deadline. It touches investments, withdrawal sequencing, charitable giving, and estate planning all at once. If taxes are not part of the conversation year round, dollars are slipping through the cracks.

Smart Tax Moves Worth Knowing

Here are strategies that many retirees either overlook or underuse.

Tax-Loss Harvesting. Selling investments that are down to offset gains elsewhere. This works best when done throughout the year, not just in a December scramble.

Asset Location. Placing the right investments in the right account types. Tax-inefficient holdings like REITs or high-yield bonds belong in IRAs or other tax-deferred accounts. Tax-efficient growth assets and municipal bonds fit better in taxable brokerage accounts. This can improve after-tax returns without changing your actual allocation.

Strategic Charitable Giving. Donor-advised funds let you bunch several years of gifts into one year for a larger deduction. Gifting appreciated stock instead of cash avoids capital gains entirely. Timing donations around high-income years multiplies the benefit.

Roth Conversions in Low-Income Years. Converting traditional IRA funds to a Roth during years when taxable income dips (for example, the gap between early retirement and Social Security) lets you pay tax at a lower bracket now and enjoy tax-free growth later. For 2026 the standard deduction is $15,000 for single filers and $30,000 for married filing jointly, which creates a built-in zero-percent bracket worth filling each year.

Pay What You Owe, Nothing More

No one is suggesting you dodge taxes. The goal is to avoid unnecessary taxes by using every legal tool available. Even a few well-timed moves can lower effective tax rates, improve cash flow, and create a more flexible retirement drawdown strategy. The higher your income or accumulated savings, the higher the stakes.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.