Why Your Tax Bracket Doesn't Mean What You Think

When couples see they're in the "32% tax bracket," many assume nearly a third of their income disappears to federal taxes. This misunderstanding costs retirees real money, sometimes tens of thousands over retirement, because it leads to poor timing decisions about IRA conversions and Social Security claiming.

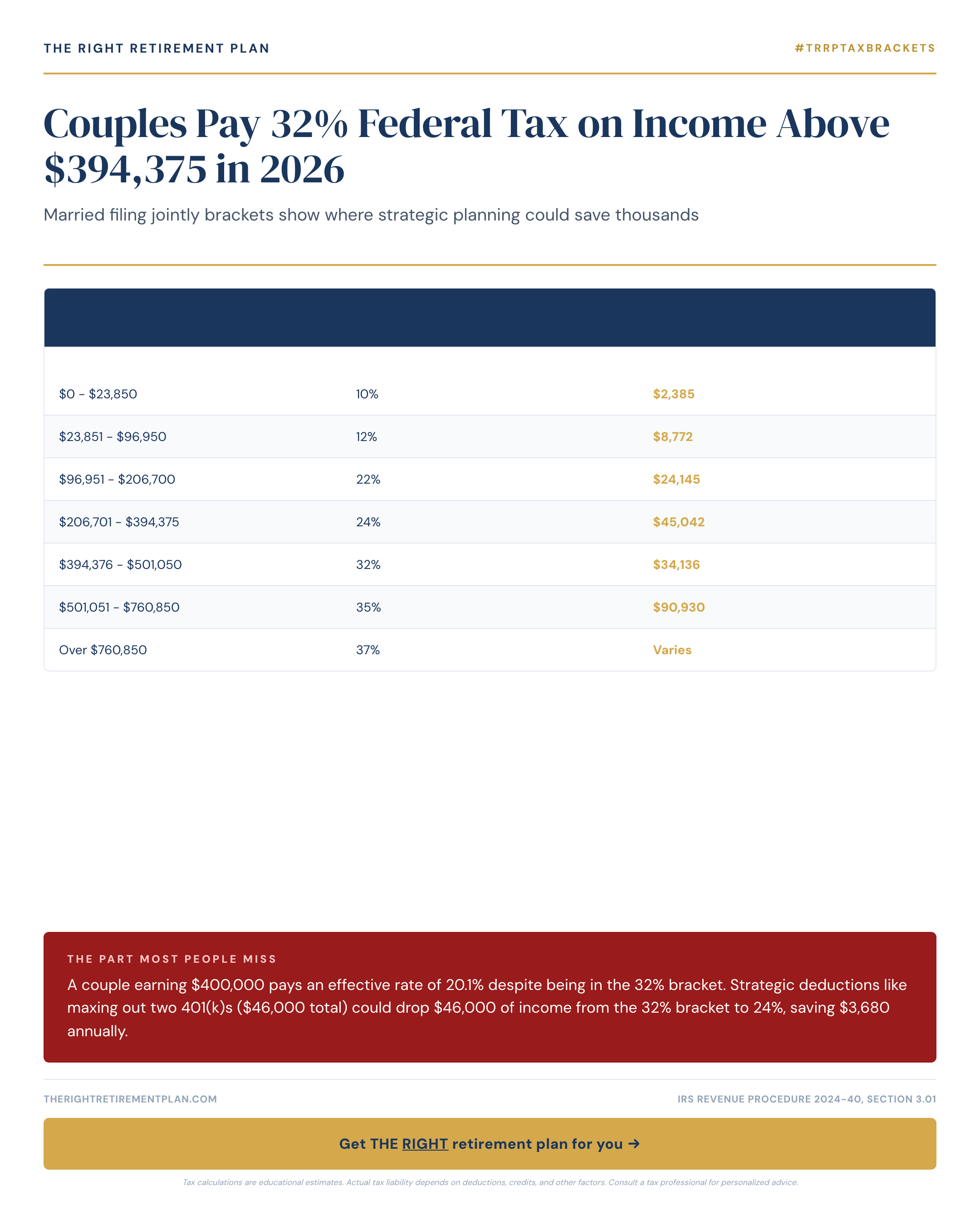

Here's the reality: a married couple earning $400,000 in 2026 pays an effective federal tax rate of approximately 20.1%, not 32%. The 32% federal tax bracket applies only to dollars above $394,375, not your entire income.

According to IRS projections, married couples filing jointly hit the 32% bracket on taxable income above $394,375 in 2026. Understanding exactly how this works, and where planning opportunities hide, could help you keep significantly more of your retirement income.

How the 2026 Federal Tax Brackets Actually Work

The federal income tax system is progressive, meaning different portions of your income get taxed at different rates. For married couples filing jointly in 2026, the <a href="/blog/2026-tax-brackets-a-250000-couple-pays-18-effective-rate">projected brackets</a> are:

- 10% on income from $0 to $23,850

- 12% on income from $23,851 to $96,950

- 22% on income from $96,951 to $206,700

- 24% on income from $206,701 to $394,375

- 32% on income from $394,376 to $501,050

- 35% on income from $501,051 to $751,600

- 37% on income above $751,600

For a couple with $400,000 in taxable income, only $5,625 actually gets taxed at 32%, the amount exceeding the $394,375 threshold. The actual federal tax on $400,000 works out to approximately $80,460, producing that 20.1% effective rate.

Strategic Planning Opportunities

Understanding tax bracket planning reveals specific opportunities to reduce lifetime tax liability. Every dollar you shift from a higher bracket to a lower one saves the difference in rates.

Retirement contribution strategies offer immediate benefits. In 2026, the 401(k) contribution limit reaches $23,500 per person, with an additional $7,500 catch-up contribution for those 50 and older. A couple maximizing both 401(k)s at $31,000 each could redirect $62,000 of pre-tax income.

Consider a couple with $420,000 in gross income. Without retirement contributions, roughly $25,625 sits in the 32% bracket. By maximizing two 401(k)s, they could drop taxable income to $358,000, keeping everything below the 32% threshold. The tax savings? Approximately $4,960 annually.

<a href="/blog/the-70500-annual-roth-conversion-most-high-earners-miss">Roth conversion timing</a> creates similar opportunities. The years between retirement and age 73 (when required minimum distributions begin) often create low-income windows. Strategic conversions during these years allow couples to pay taxes at lower rates on money that might otherwise face higher brackets later.

Maryland retirees often have additional considerations with state taxes. Understanding both federal and state bracket interactions helps maximize <a href="/topics/tax-planning">retirement tax planning</a> effectiveness.

Strategic planning requires looking beyond current brackets to project how tax rates, income sources, and legislative changes might affect your long-term tax burden.

If you want personalized guidance on how bracket planning might apply to your specific situation, consider taking our Retire Ready Score for a comprehensive assessment of your retirement readiness.