What To Do After Tax Season To Set Up A Better Retirement

Most people file their return, breathe out, and forget about taxes until next April. If you are close to retirement, that is a missed opportunity. Your return is the single best snapshot of where your plan stands. It tells you how your income is stacking up, where you are quietly overpaying, and what you can still fix while there is time. The ninety days after tax season is when the highest leverage retirement work happens. Here is how to use it.

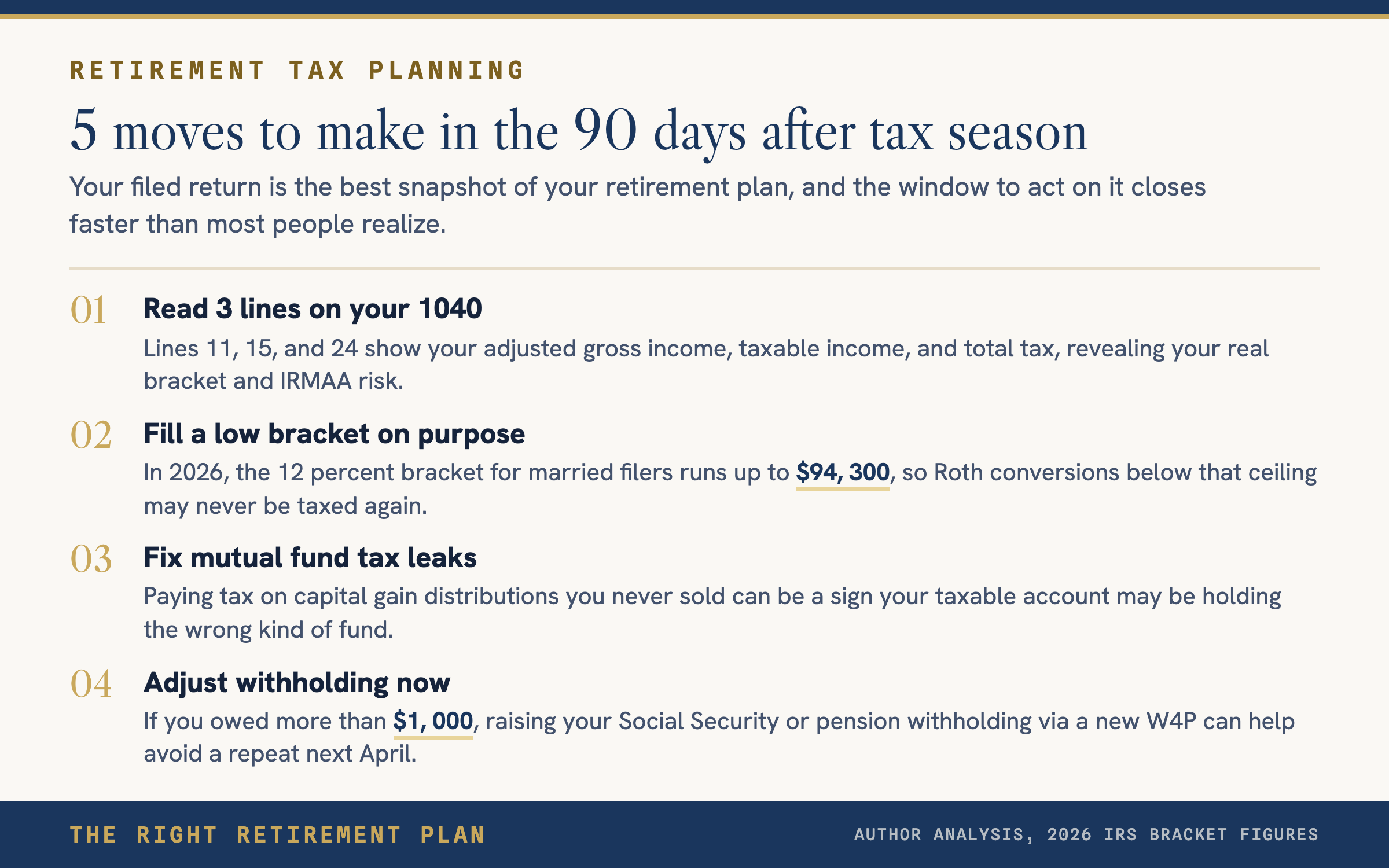

Read Your Return Like A Plan, Not A Receipt

Pull out your 1040 and look at three lines. Line 11 shows your adjusted gross income. Line 15 shows your taxable income. Line 24 shows your total tax. Together those three numbers reveal your real marginal bracket, your effective rate, and how close you are to the next IRMAA cliff for Medicare.

Many pre retirees are sitting in the 12 or 22 percent bracket right now and will jump two brackets the moment Social Security and required minimum distributions start. The ninety days after filing is the window to fill the bottom of a low bracket on purpose, usually through Roth conversions. In 2026, the 12 percent bracket for married filers runs up to $94,300. Every dollar of income you convert below that ceiling is a dollar that never gets taxed again.

Fix The Mistakes The Return Just Flagged

A return written in April is also a confession in April. Look for the quiet leaks. Did you pay tax on mutual fund capital gain distributions you never actually sold? That is a sign your taxable account is holding the wrong kind of fund. Did you hit the net investment income tax? That tells you about location, not performance. Is your itemized deduction now smaller than the standard deduction? Bunching charitable gifts into a donor advised fund every other year can swing thousands of dollars back to you.

This is also the moment to adjust withholding. If you owed more than $1,000, raise your Social Security or pension withholding now rather than writing a check next April. If you got a big refund, you lent the government money for free. Fix both by filing a new W4P.

Build The Plan For Next Year While The Numbers Are Fresh

Tax planning works best when it is proactive, which means the work happens in spring and summer, not December. Map out your expected income for the rest of 2026. Estimate any one time events such as a business sale, pension lump sum, or inherited IRA distribution. Then decide, on paper, how much Roth conversion space you have, whether a qualified charitable distribution makes sense at 70 and a half or later, and how to sequence withdrawals from taxable, tax deferred, and Roth buckets to flatten your lifetime tax bill.

The pattern we see every year is simple. Households who plan their taxes in May pay tens of thousands less over the course of retirement than households who plan their taxes in April. The math is not subtle. It is just a matter of who shows up for the meeting before the window closes.

If you want a simple starting point, take our free Retire Ready Score and see where your tax plan ranks against retirees in your situation.