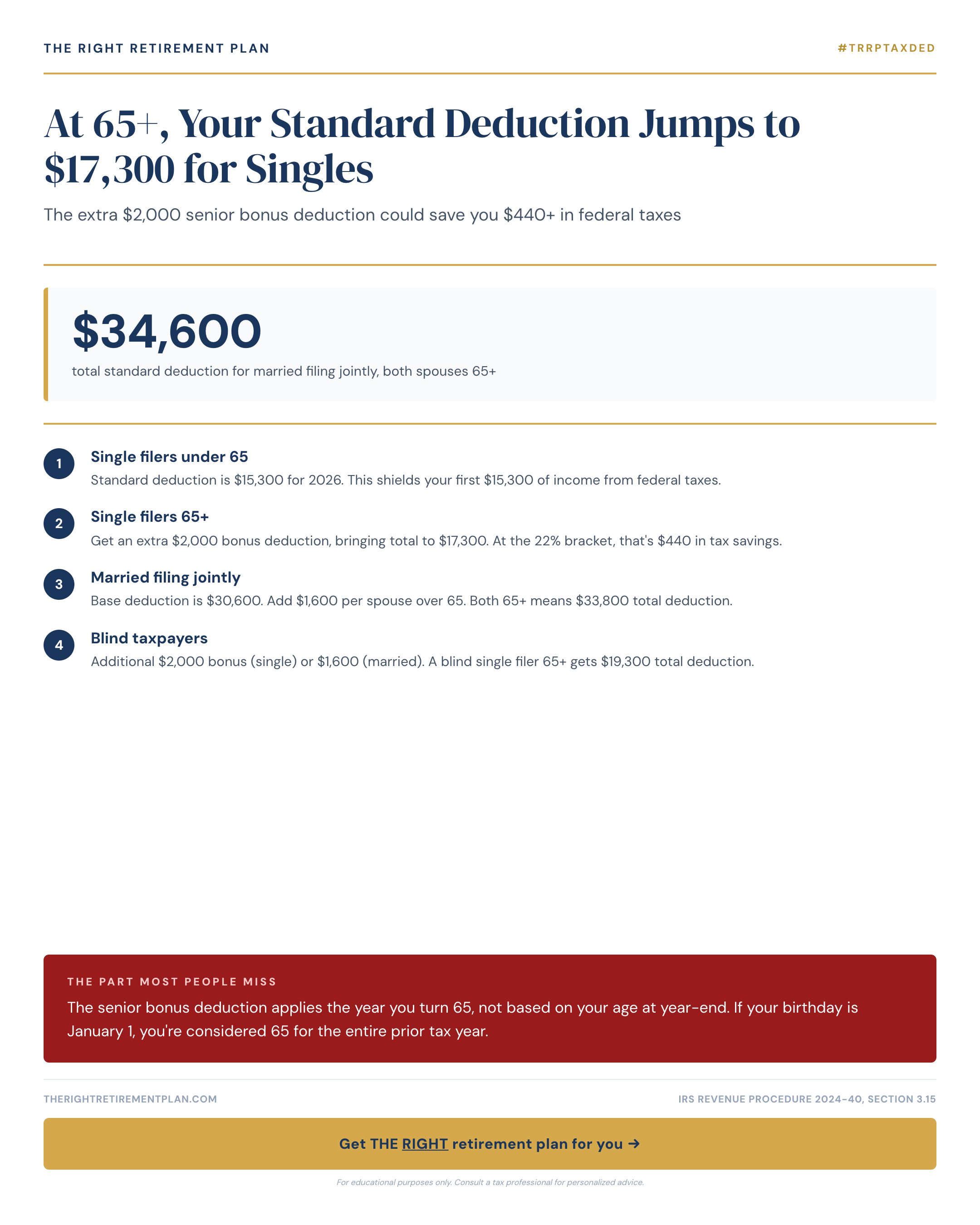

When you turn 65, the IRS gives you a welcome birthday gift: an additional $2,050 standard deduction that boosts your total to $18,150 for single filers in 2026. This senior standard deduction represents a meaningful tax break that many pre-retirees overlook in their planning.

For married couples filing jointly, the numbers are even more attractive. If both spouses are 65 or older, your combined standard deduction jumps to $35,500 in 2026, that's $3,300 more than younger taxpayers receive ($1,650 extra per spouse, on top of the $32,200 base deduction).

And for 2025 through 2028, there's a second layer: a bonus senior deduction of up to $6,000 per person age 65 or older, which phases out above $75,000 of modified adjusted gross income for singles ($150,000 for joint filers). For many retirees, that stacks on top of the age-65 standard deduction increase.

When the Senior Bonus Kicks In

The timing rules around the senior standard deduction catch many people off guard. You qualify for the extra deduction in the tax year you turn 65, regardless of when during the year your birthday falls.

Here's where it gets interesting: if your 65th birthday is January 1st, the IRS considers you 65 for the entire previous tax year. This quirky rule could move up your tax savings by a full year.

The practical impact is significant. That extra $2,050 deduction typically saves singles about $451 in federal taxes (assuming a <a href="/blog/2026-tax-brackets-a-250000-couple-pays-18-effective-rate">22% tax bracket</a>). For couples where both qualify, you're looking at potential savings of $726 or more annually.

Strategic Planning Opportunities

Smart retirees use this knowledge for tax planning strategies. If you're approaching 65, consider timing major financial moves around this threshold. Maryland retirees, for instance, might coordinate their federal planning with the state's retirement income tax benefits.

The enhanced deduction also affects whether itemizing makes sense. You might find that the higher standard deduction eliminates the need to track charitable donations, mortgage interest, and state taxes, simplifying your tax preparation considerably.

Some advisors recommend timing retirement account withdrawals to maximize the benefit of your increased standard deduction, particularly in your first year of eligibility.

Next Steps

Understanding tax advantages like the senior standard deduction is just one piece of comprehensive retirement planning. If you want personalized guidance on how this and other tax strategies fit into your overall retirement picture, consider taking our Retire Ready Score for tailored insights.