Signed into law on July 4, 2025, the One Big Beautiful Bill Act is the most significant tax overhaul since 2017. It makes several temporary provisions permanent, introduces new deductions, and reshapes retirement and estate planning for years to come.

Whether you are already retired or approaching retirement, this law changes the planning landscape in ways worth understanding now.

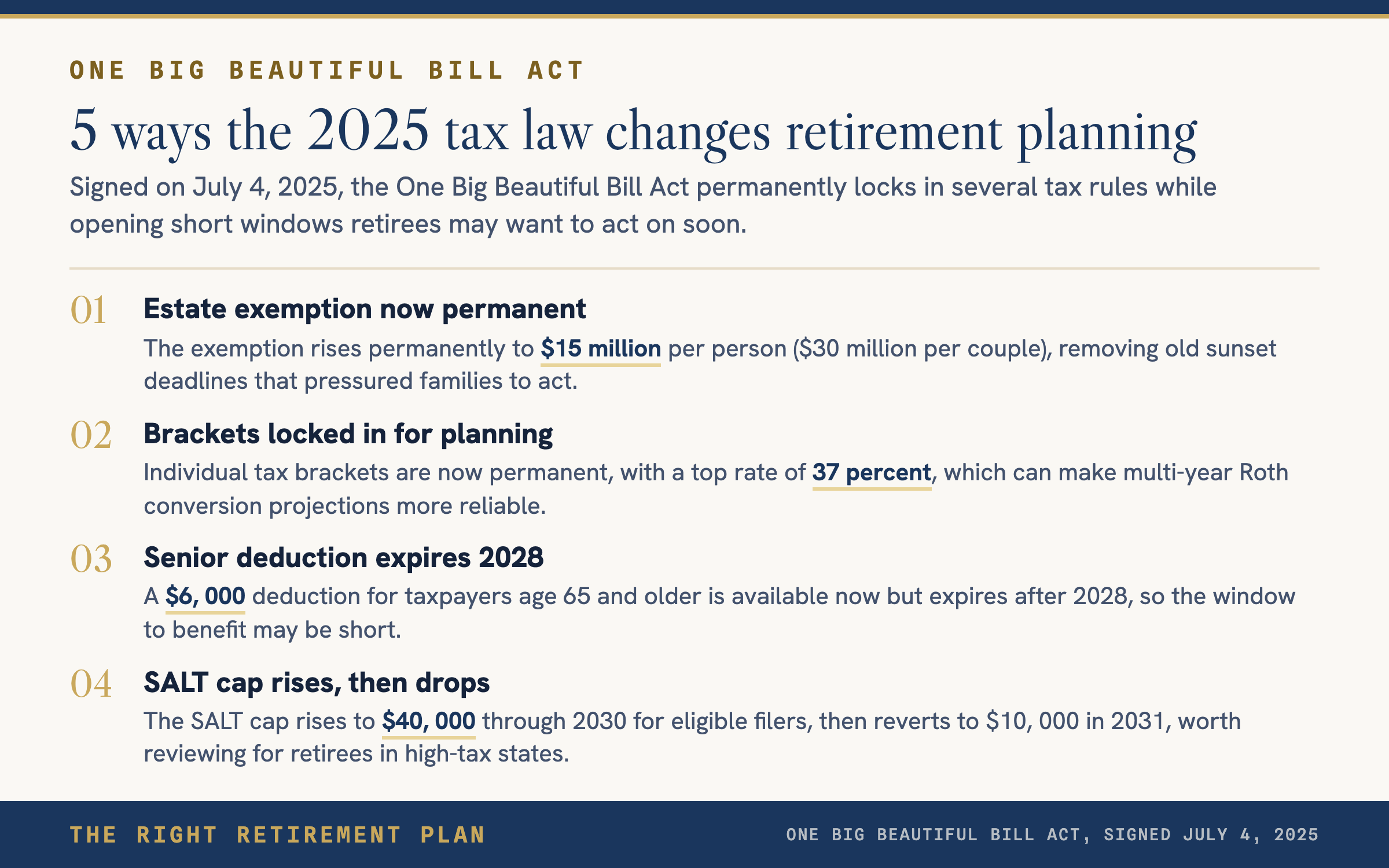

Permanent Changes That Matter Most

The estate and gift tax exemption increases permanently to $15 million per person. For married couples, that means up to $30 million can transfer to heirs free of federal estate tax. The generation-skipping transfer tax exemption rises to match. This eliminates the old "use it or lose it" pressure that had families scrambling before sunset deadlines.

Individual tax brackets from the 2017 Tax Cuts and Jobs Act are now locked in. The top rate stays at 37 percent. The standard deduction is permanently set at $15,750 for single filers and $31,500 for married couples filing jointly. For retirees building multi-year Roth conversion strategies or managing required minimum distributions, stable brackets make projections far more reliable.

Temporary Provisions With Short Windows

Several benefits expire between 2028 and 2030. A new $6,000 senior deduction is available to taxpayers age 65 and older, though it phases out at higher income levels. For a retiree in the 22 percent bracket, that could mean roughly $1,320 in annual tax savings while it lasts.

The SALT deduction cap rises from $10,000 to $40,000, effective through 2030. It begins phasing out at $500,000 in modified adjusted gross income. Retirees in high-tax states may see real relief, but only temporarily. Planning around these windows is important because the cap drops back to $10,000 in 2031.

Long-Term Care Gets More Urgent

The bill reduces Medicaid funding, particularly for long-term care programs. Retirees who assumed Medicaid would serve as a backstop for nursing home costs should revisit that assumption. Hybrid life insurance and annuity products that include long-term care riders, as well as self-funding strategies, deserve a fresh look.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.