If you have worked at more than one company during your career, there is a good chance an old 401(k) is still sitting with a former employer. Maybe it is collecting dust. Maybe you have forgotten it exists. Either way, recent regulatory changes mean those forgotten accounts deserve your attention right now.

New Investment Options Can Mean New Risks

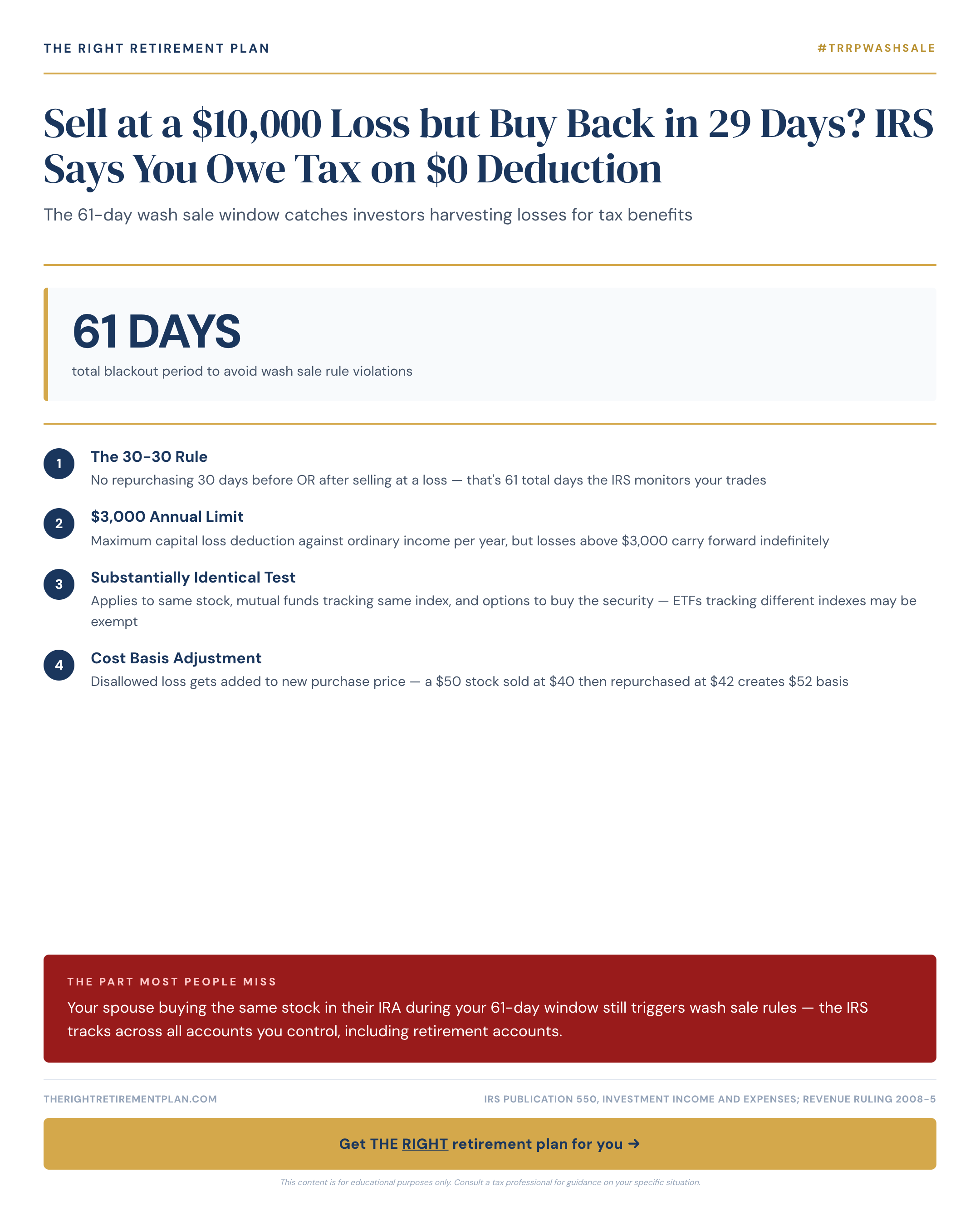

Recent guidance has opened the door for 401(k) plans to offer alternative assets like private equity, real estate, and even cryptocurrency. That may sound exciting, but there are real tradeoffs.

- These investments often carry higher fees and more volatility than a typical index fund.

- Many are illiquid, meaning your money could be locked up for years.

- Older plans are not always equipped to manage these alternatives well.

If you have an old 401(k), your investment lineup could shift without any notification, changing the risk profile of money you assumed was safe.

The Catch-Up Contribution Shake-Up

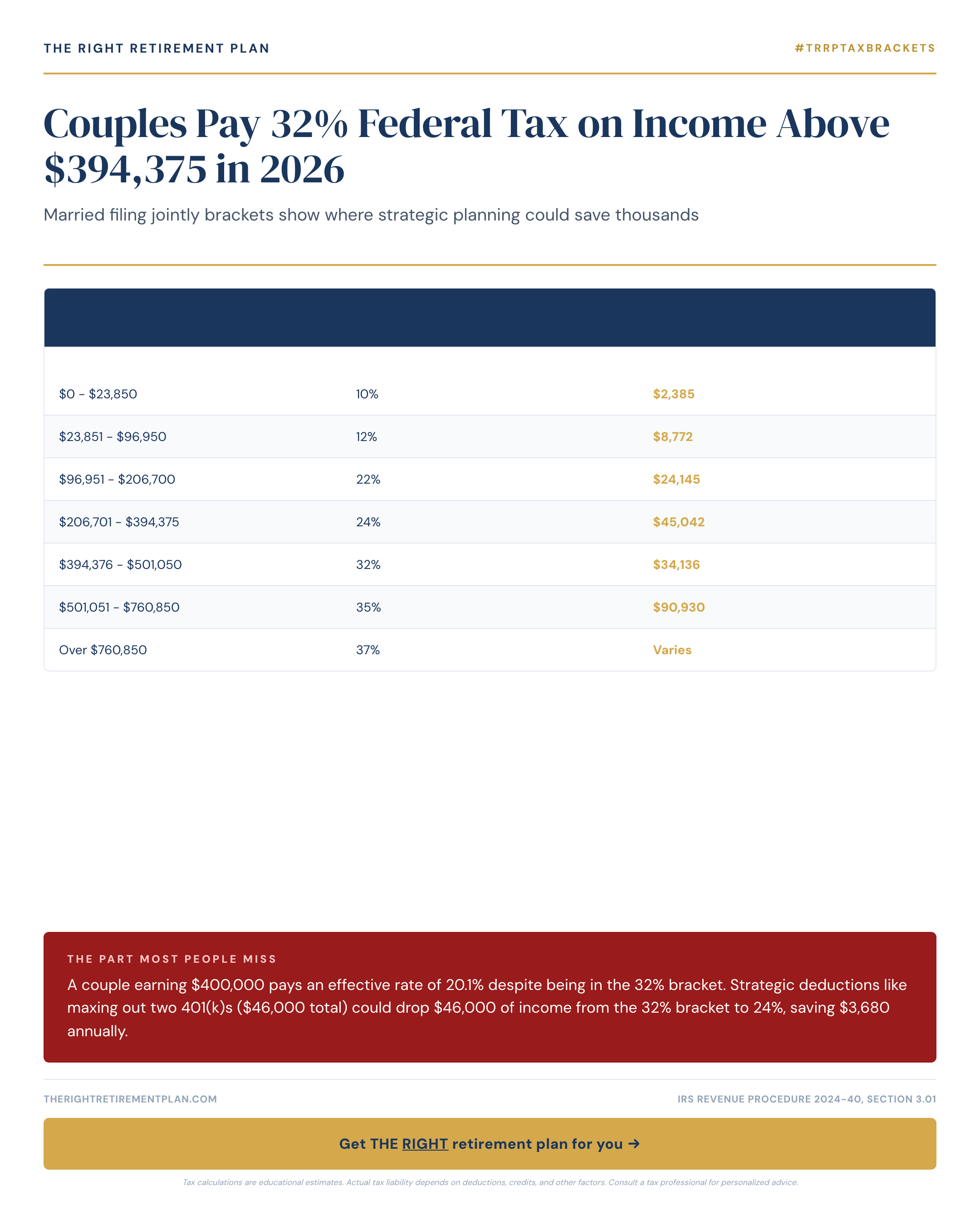

For 2026, the standard 401(k) contribution limit rises to $24,000. Workers aged 60 to 63 get an enhanced catch-up limit of $8,000 on top of that. This is a meaningful opportunity for anyone behind on retirement savings.

Here is the catch. Starting in 2026, if your FICA wages exceed $145,000, those catch-up contributions must go into a Roth (after-tax) account. This changes the tax math significantly. If an old 401(k) gets merged or reactivated, you could face this requirement unexpectedly.

Forgotten Accounts Face Forgotten Problems

New 401(k) plans are now required to auto-enroll employees and increase contributions over time. They also include automatic portability features that move small balances when you change jobs. But older plans do not have to follow these rules.

That means an old account could be stuck with high fees, outdated fund choices, and no easy path to consolidation. The longer it sits, the more these problems compound.

Here is what to do right now:

- Track down every old 401(k). Many people have lost accounts worth tens of thousands of dollars.

- Review your investments for high expense ratios, poor performance, or misaligned risk.

- Consider a rollover into an IRA or your current employer plan for more control and lower fees.

- Plan for the 2026 Roth catch-up rule, especially if you are in the 60 to 63 age bracket.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.