You've probably seen the ads: "Protect your family with a living trust!" Maybe an attorney quoted you $2,500 to $5,000 for a trust package. Or a well-meaning friend insisted that without a trust, your heirs will spend years in probate court.

Here's what those ads don't tell you: for estates under $13.99 million, a properly structured will combined with smart account titling can accomplish nearly everything a living trust does, often at a fraction of the cost. According to the American Bar Association, roughly 95% of American households fall below the 2026 federal estate tax exemption threshold, yet the trust industry continues marketing these products as essential for everyone.

This doesn't mean trusts are useless. For certain situations, blended families, special needs dependents, significant real estate in multiple states, they remain valuable tools. But for the typical retiree with a straightforward estate, the math often doesn't support the expense.

The Zero-Cost Probate Avoidance Strategy

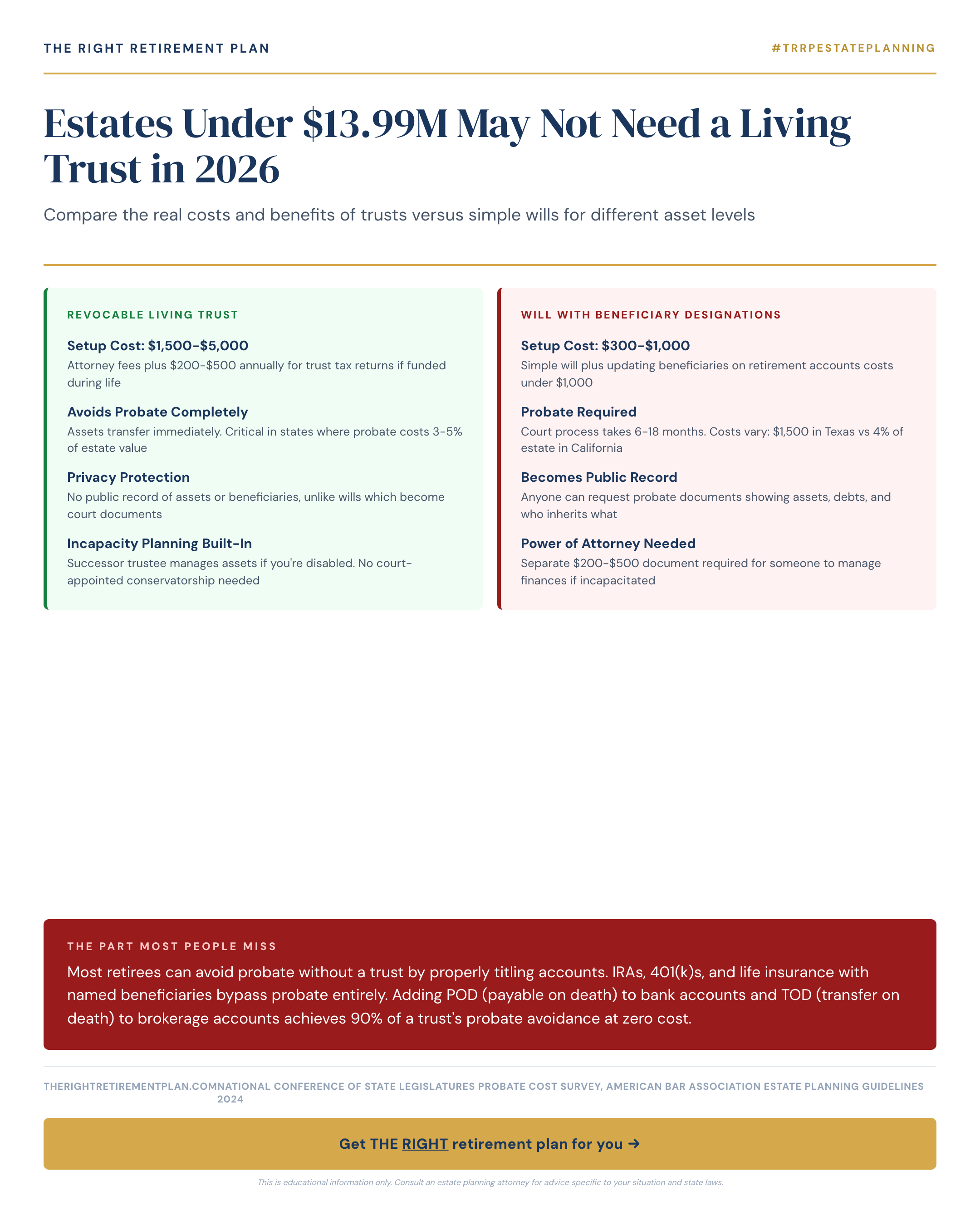

Most retirees can avoid probate on 90% or more of their assets without spending a dime on a trust. The secret lies in understanding which assets actually go through probate, and which don't.

Assets that bypass probate automatically with proper titling:

- Retirement accounts (IRAs, 401(k)s, 403(b)s) with named beneficiaries pass directly to those beneficiaries

- Life insurance policies with named beneficiaries pay directly to those individuals

- Bank accounts with Payable on Death (POD) designations transfer immediately to named beneficiaries

- Brokerage accounts with Transfer on Death (TOD) designations work the same way

- Jointly titled property with rights of survivorship passes automatically to the surviving owner

What actually goes through probate:

- Real estate titled solely in your name

- Vehicles in your name alone

- Personal property without designated beneficiaries

- Bank and investment accounts without POD/TOD designations

For many Maryland retirees, properly titled accounts mean the only assets requiring probate are a car, household items, and perhaps a home. Many states have simplified probate procedures for smaller estates that avoid lengthy court processes entirely.

When You Actually Need a Living Trust

Despite the effectiveness of beneficiary designations, certain situations genuinely warrant the expense of a revocable living trust.

Real estate in multiple states creates the strongest case for a trust. Without one, your heirs may face separate probate proceedings in each state where you own property. If you own a vacation home in Florida and your primary residence in the Mid-Atlantic, your estate could face two parallel court processes.

Blended families with complex inheritance wishes often benefit from trust provisions. If you want your current spouse to have use of your home during their lifetime but ultimately want the property to pass to children from a previous marriage, a trust accomplishes this more reliably than a will.

Special circumstances that warrant trusts include:

- Adult children with spending problems or creditor issues

- Beneficiaries receiving means-tested government benefits

- Minor children who can't legally inherit directly

- Privacy concerns where public probate records are problematic

If none of these situations apply to you, a simple will combined with proper beneficiary designations likely accomplishes your goals at far lower cost.

A 2019 study by WealthCounsel found that roughly 60% of living trusts are inadequately funded at the grantor's death. That beautiful $5,000 trust document becomes essentially decorative if you never transferred your assets into it. Those assets still pass through probate, exactly what you paid to avoid. Conversely, the simple beneficiary designation on your IRA requires no ongoing maintenance and passes directly regardless of what your will or trust says.

The 2026 federal estate tax exemption of $13.99 million per person means trusts provide zero tax benefit for approximately 99.9% of estates. For most retirees, beneficiary designations on retirement accounts, life insurance, and POD/TOD registrations accomplish probate avoidance at no cost while requiring minimal maintenance.

If you're wondering whether your current estate setup has gaps that could cost your heirs, consider taking our Retire Ready Score for personalized guidance on your specific situation.