Imagine building a company over decades, only to face a tax bill that wipes out a third or more of the sale price. That is the reality many founders confront when they sell to a private buyer. For owners of closely held C-corporations, an ESOP sale combined with Section 1042 offers a powerful, IRS-sanctioned alternative that can defer millions in capital gains taxes.

How an ESOP Sale Under Section 1042 Works

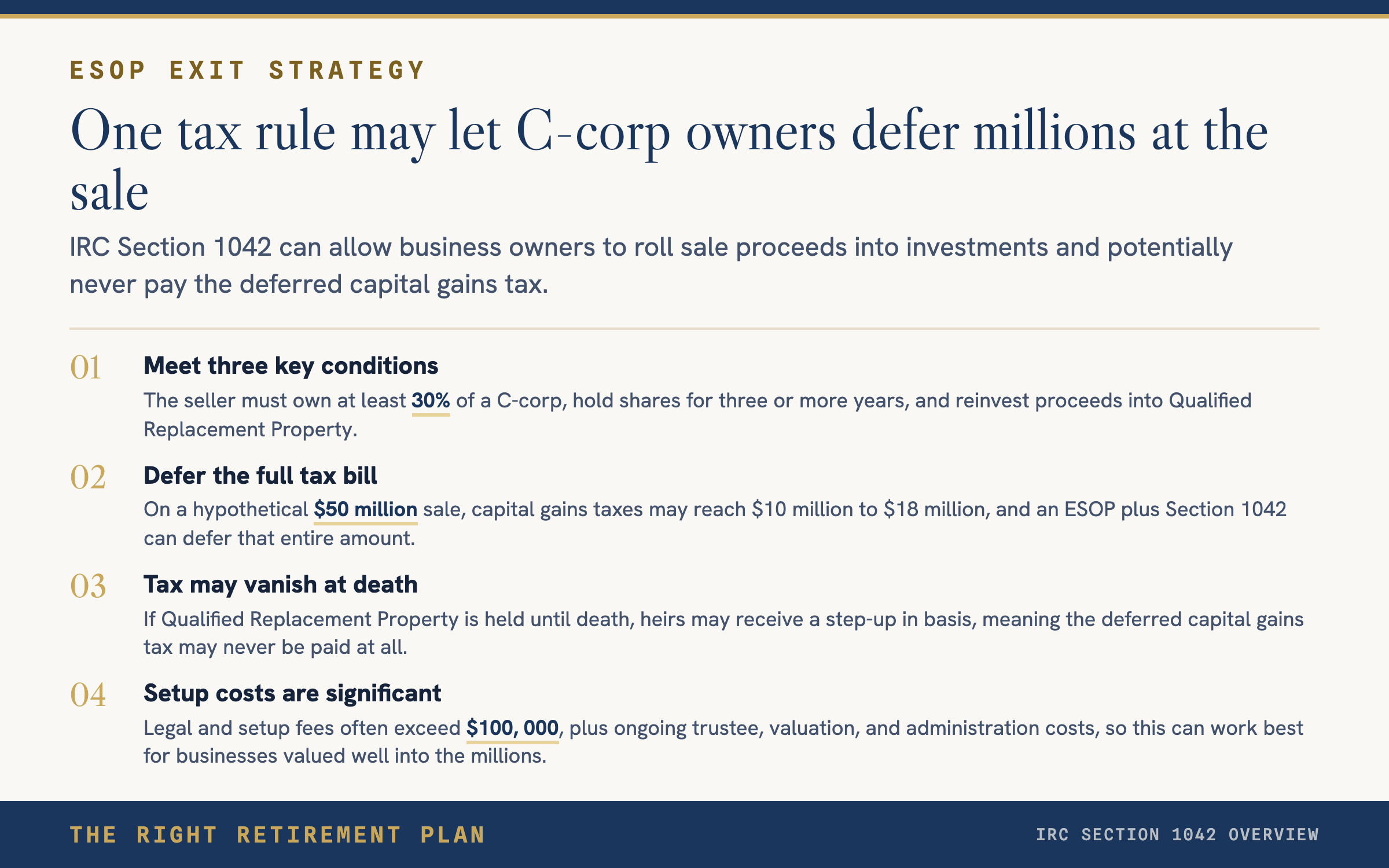

Section 1042 of the Internal Revenue Code allows C-corp owners to defer capital gains taxes when they sell shares to an ESOP, provided three conditions are met.

- At least 30% of the company is sold to the ESOP.

- The seller has held the shares for three or more years.

- Sale proceeds are reinvested into Qualified Replacement Property within a specific window.

If the seller holds the QRP until death, heirs receive a step-up in basis. That means the deferred capital gains tax may never be paid at all.

Why Business Owners Choose This Path

Tax savings grab the headlines, but an ESOP sale offers benefits beyond the balance sheet. Selling to an ESOP lets the founder keep existing leadership in place, reward employees with real ownership stakes, and avoid the disruption that often follows a private equity buyout. Employees become beneficial owners, which can boost morale and retention. The company continues operating without layoffs or culture shock.

For a hypothetical $50 million sale, the capital gains tax bill under a traditional transaction could easily reach $10 million to $18 million at combined federal and state rates. An ESOP plus Section 1042 strategy can defer that entire amount.

The Trade-Offs to Understand

ESOPs are not simple or cheap. Legal and setup fees often exceed $100,000. Ongoing costs include independent valuations, trustee fees, and plan administration. The deal structuring and QRP investment selection add layers of complexity that require experienced legal and financial guidance.

This strategy is best suited for owners of profitable C-corporations valued well into the millions, where the tax savings far outweigh the setup and maintenance costs.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.