In April 2025, the Dow surged nearly 3,000 points in a single day after a 90-day pause on proposed tariffs calmed inflation fears. For investors on the sidelines waiting for "the right time" to get back in, that rally came and went before they could act.

This pattern is not new. And it carries an important lesson for anyone planning for or living in retirement.

Market Rallies Do Not Send Invitations

Most people who try to "time the bottom" miss it. Most people who say they will wait until things calm down are still waiting. The biggest single-day gains tend to cluster around the most volatile periods, not the calm ones.

Consider a simple example using S&P 500 data from 1999 to 2023, starting with one million dollars:

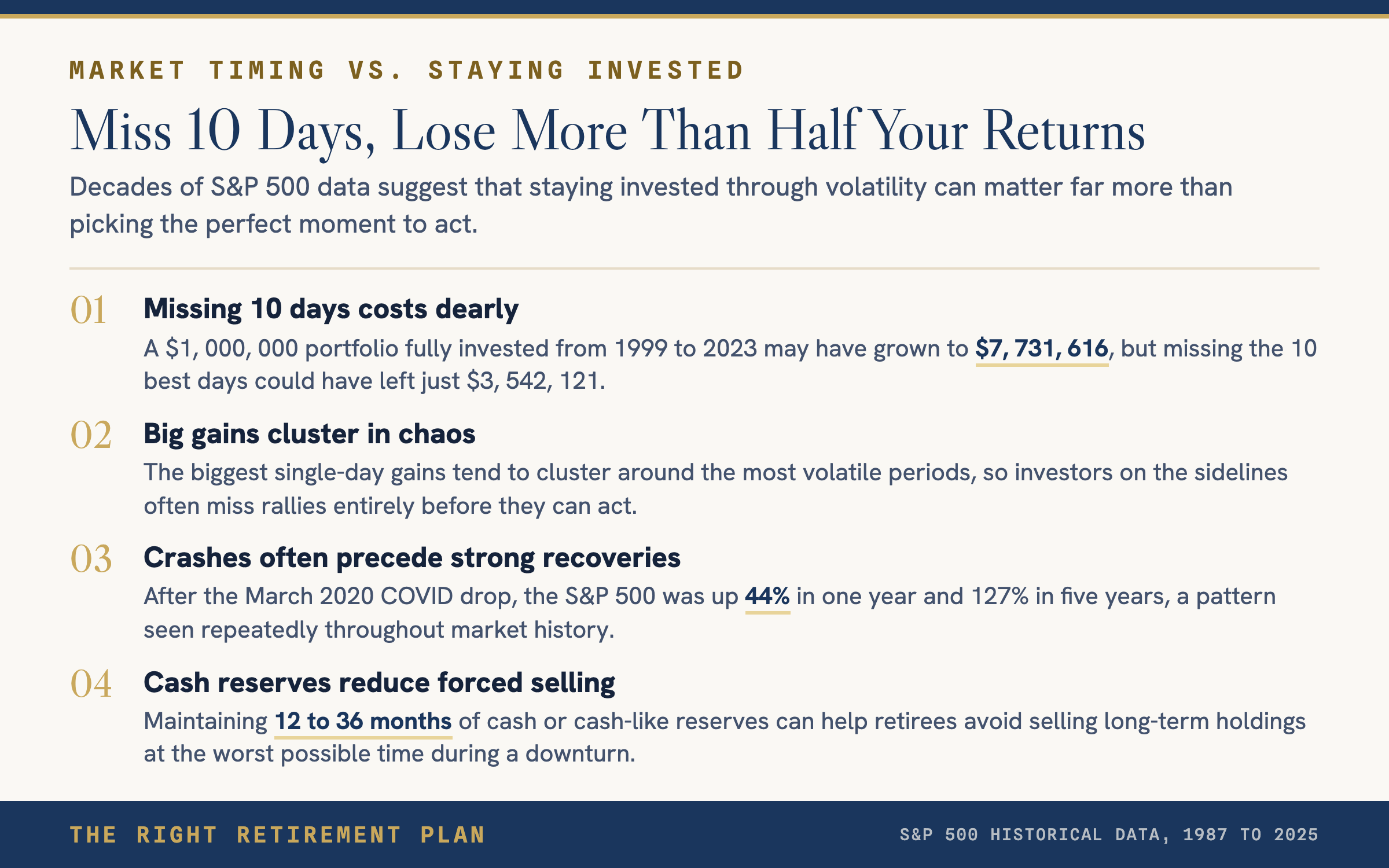

- Fully invested the entire time: $7,731,616

- Missed the 10 best days: $3,542,121

- Missed the 25 best days: $1,654,515

History Favors Those Who Stay In

Look at the largest two-day drops in S&P 500 history. Each one felt like a crisis at the time.

- After the 1987 crash (down 24.6% in two days), the S&P gained 28% in one year and 119% in five years.

- After the March 2020 COVID drop, the S&P was up 44% in one year and 127% in five years.

- After the October 2008 panic, five-year returns exceeded 100%.

How Retirees Can Stay Calm During Volatility

Staying invested does not mean ignoring risk. Many retirees maintain 12 to 36 months of cash or cash-like reserves specifically so they never have to sell long-term holdings during a downturn. This approach provides stable income, protects against forced selling, and gives growth-oriented investments time to recover.

A disciplined withdrawal strategy paired with adequate reserves turns scary headlines into background noise.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.