Annuities are one of the most aggressively marketed retirement products in America. The brochures promise safety, guaranteed income, and market protection. But for most retirees, annuities are more confusing than helpful and far better for the person selling them than the person buying them.

Before signing a contract that could lock up your savings for a decade, it pays to understand what is really going on behind the scenes.

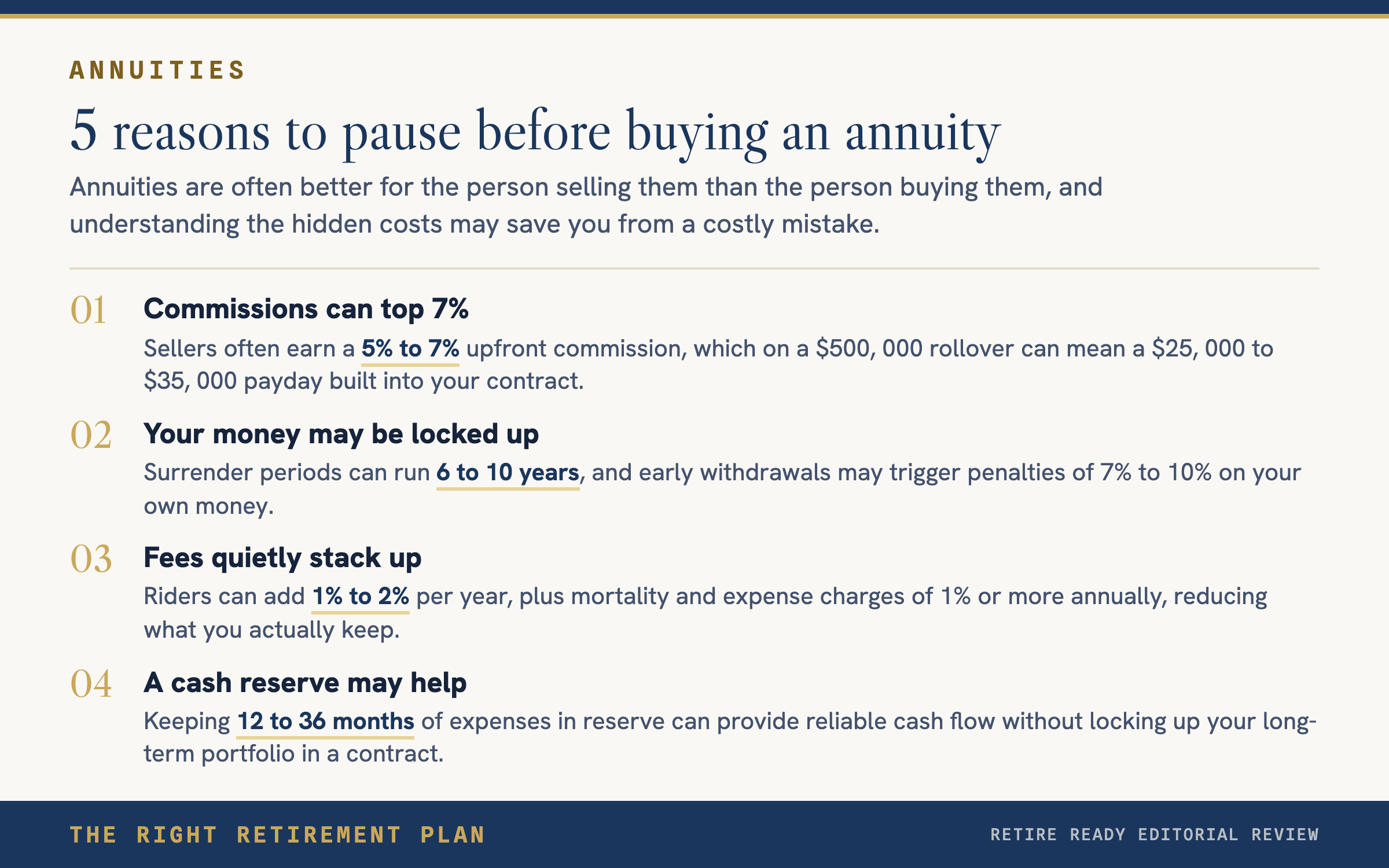

Follow the Money First

When someone sells you an annuity, they typically earn a 5% to 7% commission upfront. On a $500,000 rollover, that is a $25,000 to $35,000 payday. Often hidden. Often baked into the contract.

Once the sale is complete, there is little incentive for that person to help you adjust your plan over time. They have already been paid. Compare that to a fiduciary advisor who charges transparent, ongoing fees with no product kickbacks. One model is built to serve your goals. The other is built to move product.

The Lock-Up Problem

Most annuities come with a surrender period, typically 6 to 10 years. During that window, withdrawing more than a small percentage of your balance triggers penalties of 7% to 10%. On your own money.

If a medical emergency, family need, or unexpected expense comes up, your financial flexibility has been handed over to the insurance company. That tradeoff rarely gets the attention it deserves during the sales pitch.

The "Guaranteed Income" Illusion

The phrase "guaranteed income for life" sounds reassuring. But in many variable or indexed annuities, that income is simply your own principal being returned to you slowly, minus layers of fees:

- Riders that add 1% to 2% per year in charges

- Caps and participation rates that limit your upside

- Mortality and expense charges of 1% or more annually

- Locked-in annuitization that strips you of control over the asset

What Works Instead

Retirement income does not require an annuity contract. Many retirees build reliable cash flow using a combination of strategies:

- A diversified portfolio of dividend-paying stocks, bonds, and low-cost funds

- A dynamic withdrawal plan that adjusts based on market conditions and tax efficiency

- A cash reserve covering 12 to 36 months of expenses so the long-term portfolio can keep compounding

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.