Most people hear "financial plan" and picture a thick PDF full of pie charts and projections that are outdated before the ink dries. That version of planning is a relic. A real plan is something you actually use.

If you have ever asked yourself whether you have enough to retire, whether you are paying more in taxes than you should, or what happens if the market drops again, you are already thinking like a planner. The problem is that most people have never been shown what a genuine retirement financial plan can do.

What a Financial Plan Really Is

A financial plan is a living strategy designed to give you clarity, control, and confidence. It is not a product. It is a process that evolves as your life changes.

Think of it as a GPS for your financial life. You set the destination. Maybe that is retiring at 62, relocating to a lower tax state, or leaving a legacy. The plan maps the route and reroutes when life throws a detour.

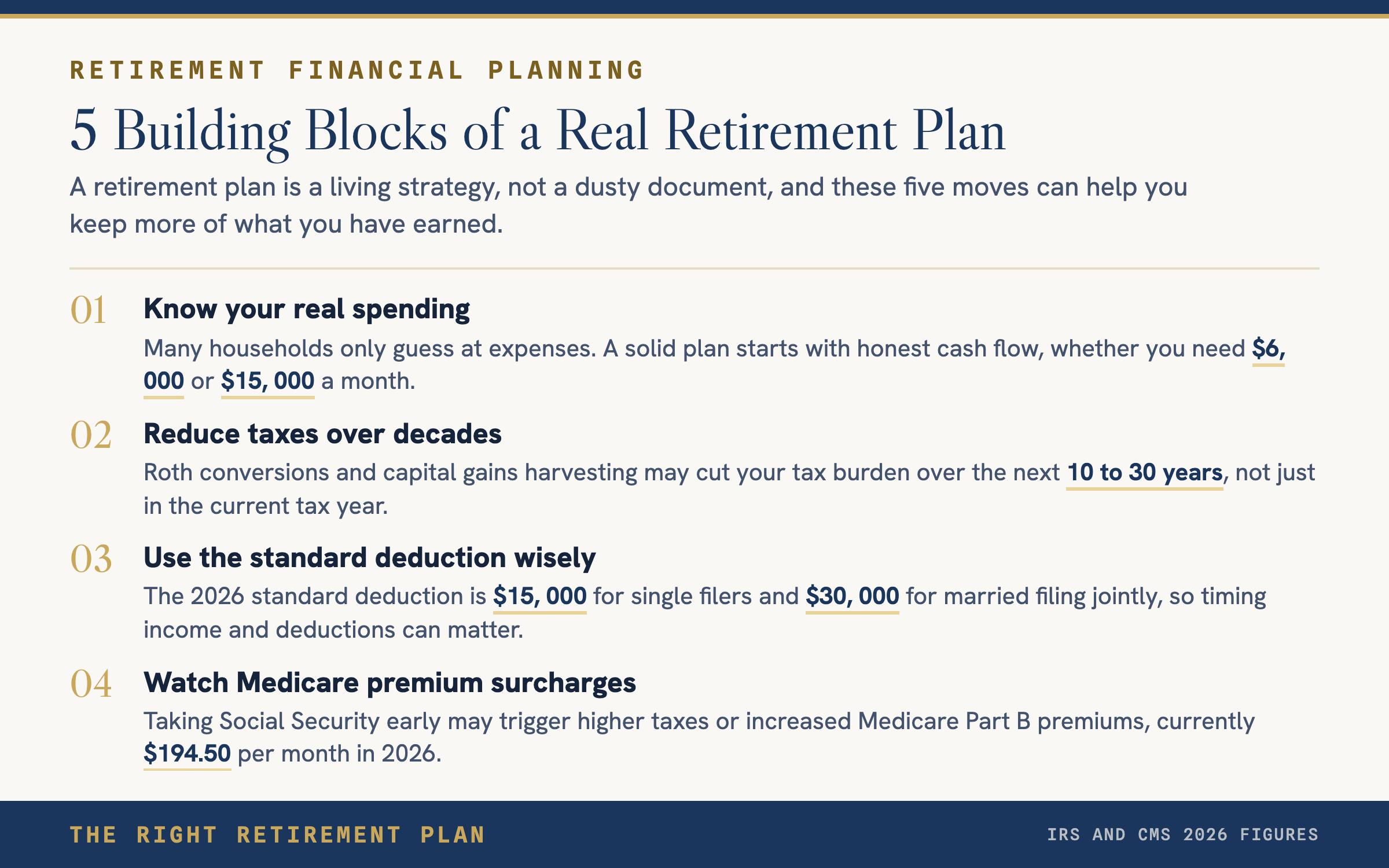

In practice, a strong retirement financial plan helps you do several things well.

The Building Blocks of a Good Plan

Know what you actually spend. Many households have a vague sense of their expenses, but few know the real numbers. Do you need $6,000 a month in retirement or $15,000? A plan starts with honest cash flow so everything else is built on reality.

Grow your savings without losing sleep. Investing should not feel like gambling. Your plan should define how your money is invested and why, based on your goals and time horizon, not on headlines or emotions.

Minimize taxes over a lifetime. Most plans ignore tax strategy entirely. From asset location to Roth conversions to capital gains harvesting, a smart retirement financial plan reduces your tax burden not just this year but over the next 10 to 30 years. With the 2026 standard deduction at $15,000 for single filers and $30,000 for married filing jointly, even basic decisions around timing income and deductions matter.

Prepare for big transitions. Retiring early, selling a business, or claiming Social Security (with its 2.5% COLA for 2026) are decisions that deserve analysis before they happen, not after.

Build in margin for the unexpected. Markets crash. Health changes. A plan should include emergency reserves, withdrawal flexibility, and insurance strategies so that a bad quarter does not become a bad decade.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.