What Is Really Driving the Volatility

In early April 2025, markets sold off sharply. The Dow dropped thousands of points across just a few sessions. The Nasdaq briefly entered bear market territory. Tariff announcements between the U.S. and China escalated quickly, and headlines made everything feel urgent.

But market volatility driven by policy negotiations tends to follow a pattern. The initial shock is loud. The resolution is quieter. And the investors who changed nothing often end up in the best position.

Beneath the tariff drama, broader fiscal goals were in play. Treasury Secretary Scott Bessent outlined a framework targeting 3% GDP growth, a 3% federal deficit as a share of GDP, and 3 million additional barrels of daily U.S. oil production. Whether or not those targets are met, the signal was clear: the administration was using disruption as a negotiating lever, not as a permanent policy stance.

Why Retirees Should Focus on Income, Not Headlines

When markets swing, it is tempting to react. But for anyone within five years of retirement, or already retired, the real risk is not a bad week in the market. The real risk is abandoning a sound income plan because of fear.

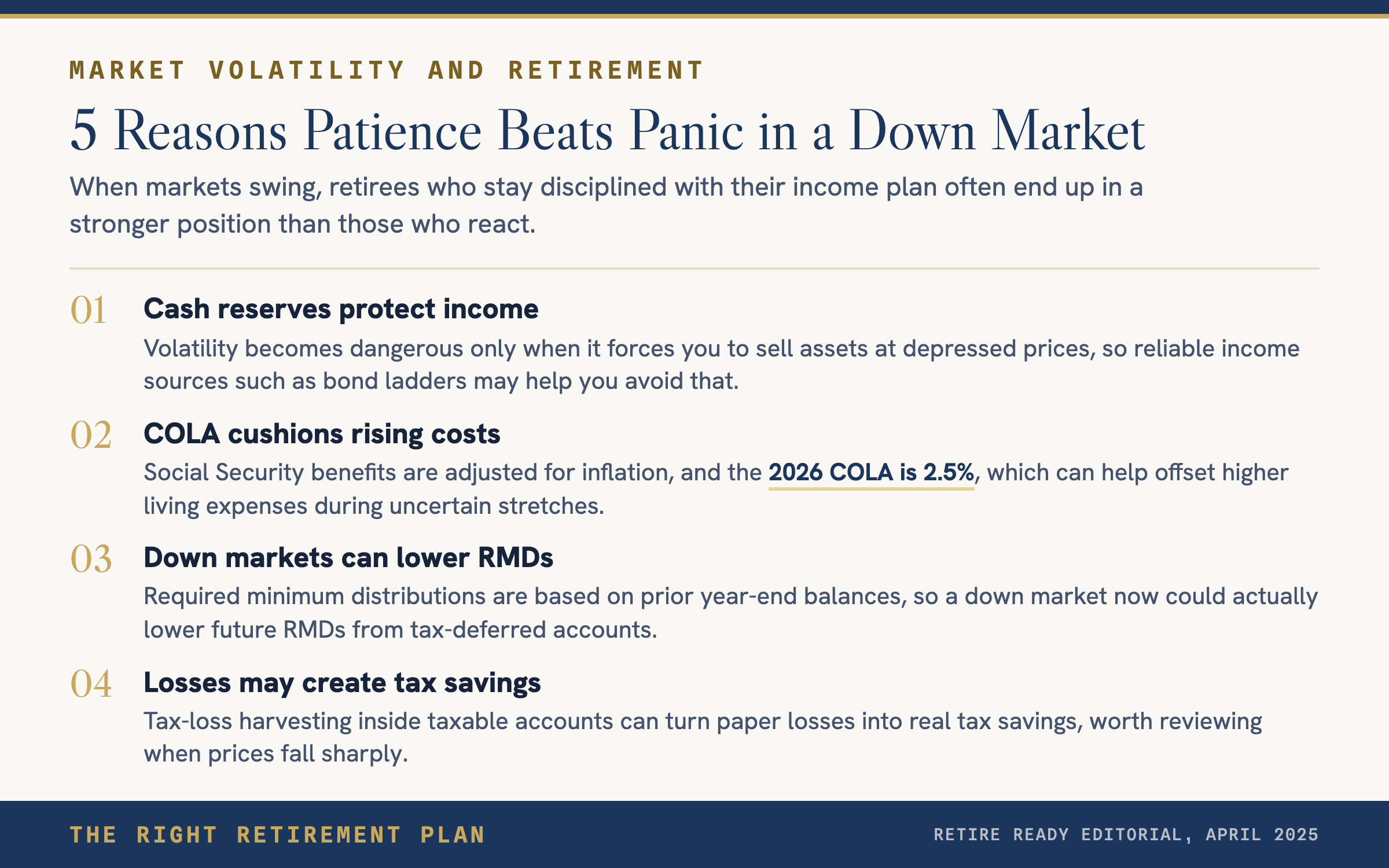

Market volatility becomes dangerous only when it forces you to sell assets at depressed prices to cover living expenses. That is why a well-built retirement income plan, one that includes cash reserves, bond ladders, or other reliable income sources, matters so much.

A few things worth remembering during volatile stretches:

- Social Security benefits are adjusted for inflation. The 2026 COLA is 2.5%, which helps offset rising costs.

- Required minimum distributions from tax-deferred accounts are based on prior year-end balances, so a down market now could actually lower future RMDs.

- Tax-loss harvesting inside taxable accounts can turn paper losses into real tax savings.

For Long-Term Investors, Discipline Wins

If retirement is still a decade or more away, volatility is your friend. Lower prices today mean more shares purchased with each contribution. The 2026 401(k) contribution limit is $24,000, with an additional $8,000 catch-up for those ages 60 to 63. Continuing to invest through downturns is one of the most reliable wealth-building strategies available.

Trying to time the bottom almost never works. Staying invested almost always does.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.