If budgeting feels like it never quite works, the problem probably is not discipline. It is that most budgets only account for monthly bills and ignore the irregular expenses that show up with irritating consistency. Car repairs, holiday travel, annual insurance premiums, dental work, gifts. These costs are not emergencies. They are just normal life on a non-monthly schedule.

The good news: a simple system can fix this for good.

Why Monthly Budgets Miss the Mark

Traditional budgets list the predictable monthly costs: mortgage or rent, utilities, groceries, insurance, streaming services. That is a great start. But life does not arrive in neat 30-day cycles.

Property tax bills, semi-annual insurance premiums, and seasonal travel all land outside the monthly framework. When they hit, even a well-planned budget can feel like it failed overnight. The credit card comes out, stress kicks in, and the whole system feels broken.

The real issue is not overspending. It is that predictable irregular expenses were never part of the plan.

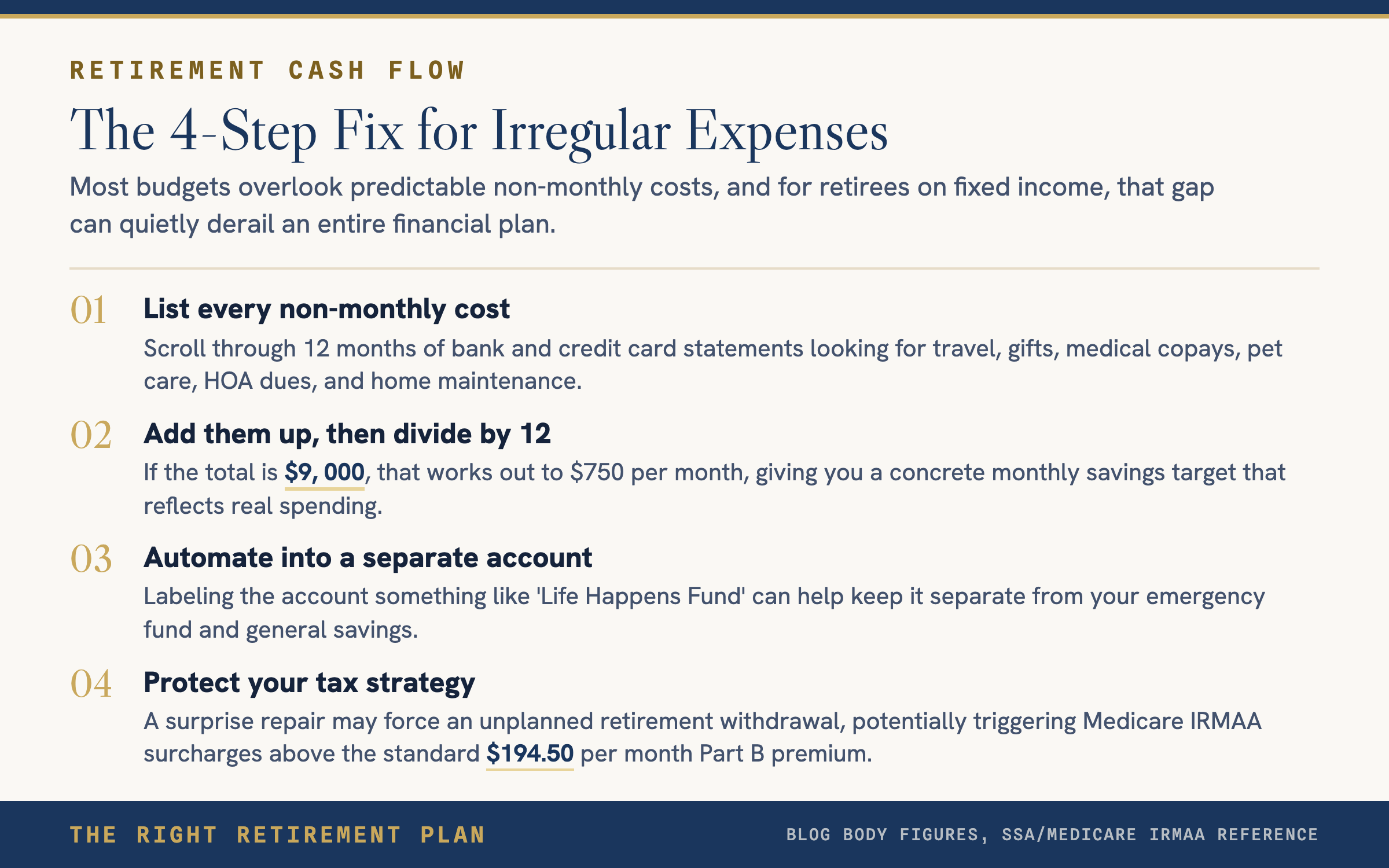

The 4-Step Fix for Irregular Expenses

This approach takes about 30 minutes and pays off every month going forward.

1. List every non-monthly expense from the last 12 months. Scroll through bank and credit card statements. Look for anything that does not recur monthly but still affects your finances. Think travel, gifts, medical copays, pet care, HOA dues, and home maintenance.

2. Add them up. The total often surprises people. Seeing the real number is better than being blindsided later.

3. Divide by 12. If the total is $9,000, that equals $750 per month.

4. Automate that amount into a separate account. Label it something like "Life Happens Fund." This is not your emergency fund and not your general savings. It is a buffer for normal, recurring but irregular costs.

When the car needs brakes or a grandchild's birthday rolls around, the money is already set aside. No scrambling, no guilt, no credit card debt.

Why This Matters Even More in Retirement

For retirees and pre-retirees living on a relatively fixed income, irregular expenses carry extra weight. A $1,400 furnace repair can force an unplanned withdrawal from a retirement account, potentially pushing income into a higher tax bracket or triggering Medicare IRMAA surcharges above the standard $194.50 per month Part B premium.

Building irregular costs into a monthly cash flow plan protects both the budget and the broader tax strategy. Many financial planners recommend keeping at least one full year of irregular expenses mapped out so that required minimum distributions and Roth conversion plans stay on track.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.