We have all grown up with the idea that retirement happens at 65. But 65 is just a number on a calendar. It is not a financial requirement, and it is definitely not a finish line.

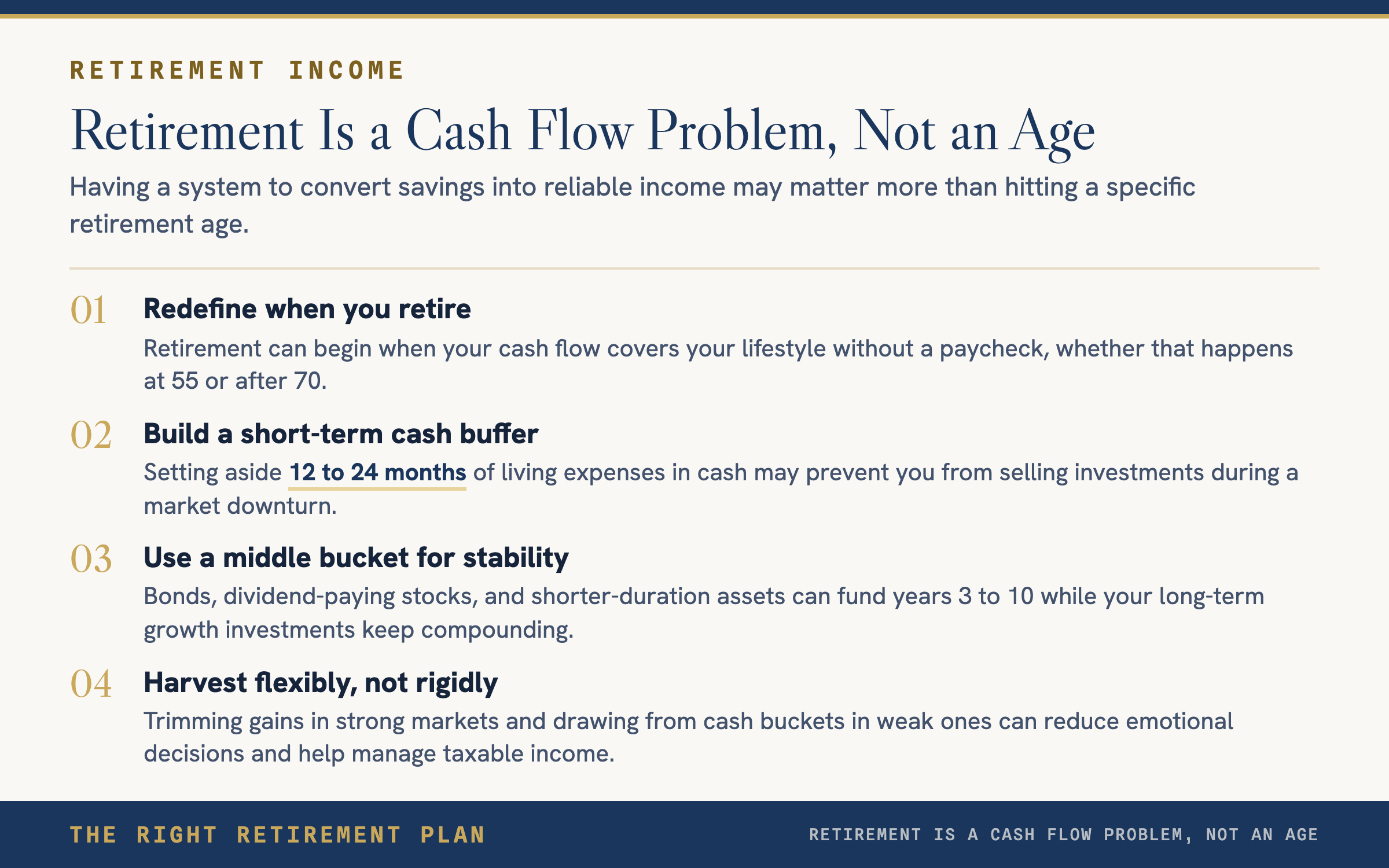

Retirement happens when your money can cover your lifestyle without relying on a paycheck. If that is happening at 55, you are retired. If it is not happening at 70, you are not. The real question is not "When can I retire?" It is "Does my retirement cash flow support the life I want?"

Turning a Portfolio into Reliable Income

Consider a retiree with $3.4 million in investable assets, no debt, and a paid-off home. On paper, that looks like plenty. But without a system to convert savings into income, even a strong balance sheet can feel uncertain. Many retirees are not short on money. They are short on cash flow confidence.

A bucket strategy is one of the most effective ways to solve this. Here is how it typically works.

Short-term cash bucket (Years 0 to 2). Set aside 12 to 24 months of living expenses in cash or cash-like instruments. This creates breathing room so you never have to sell investments in a down market just to pay bills.

Intermediate bucket (Years 3 to 10). This sleeve holds bonds, dividend-paying stocks, and shorter-duration assets designed for stability and income. It funds your middle years while long-term investments keep growing.

Growth bucket (Years 10 and beyond). Globally diversified equities and growth-oriented funds sit here. The purpose is to outpace inflation, rising healthcare costs, and longevity risk. Because your near-term needs are already covered, these assets can ride out volatility.

A Flexible Harvesting Strategy Ties It Together

Markets move, and so does retirement spending. Rather than withdrawing the same fixed amount each month, a flexible harvesting approach adjusts based on conditions.

- In strong markets, trim gains from growth assets.

- In weak markets, pull from cash and bond buckets.

- Rebalance along the way and layer in tax-aware withdrawal planning.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.