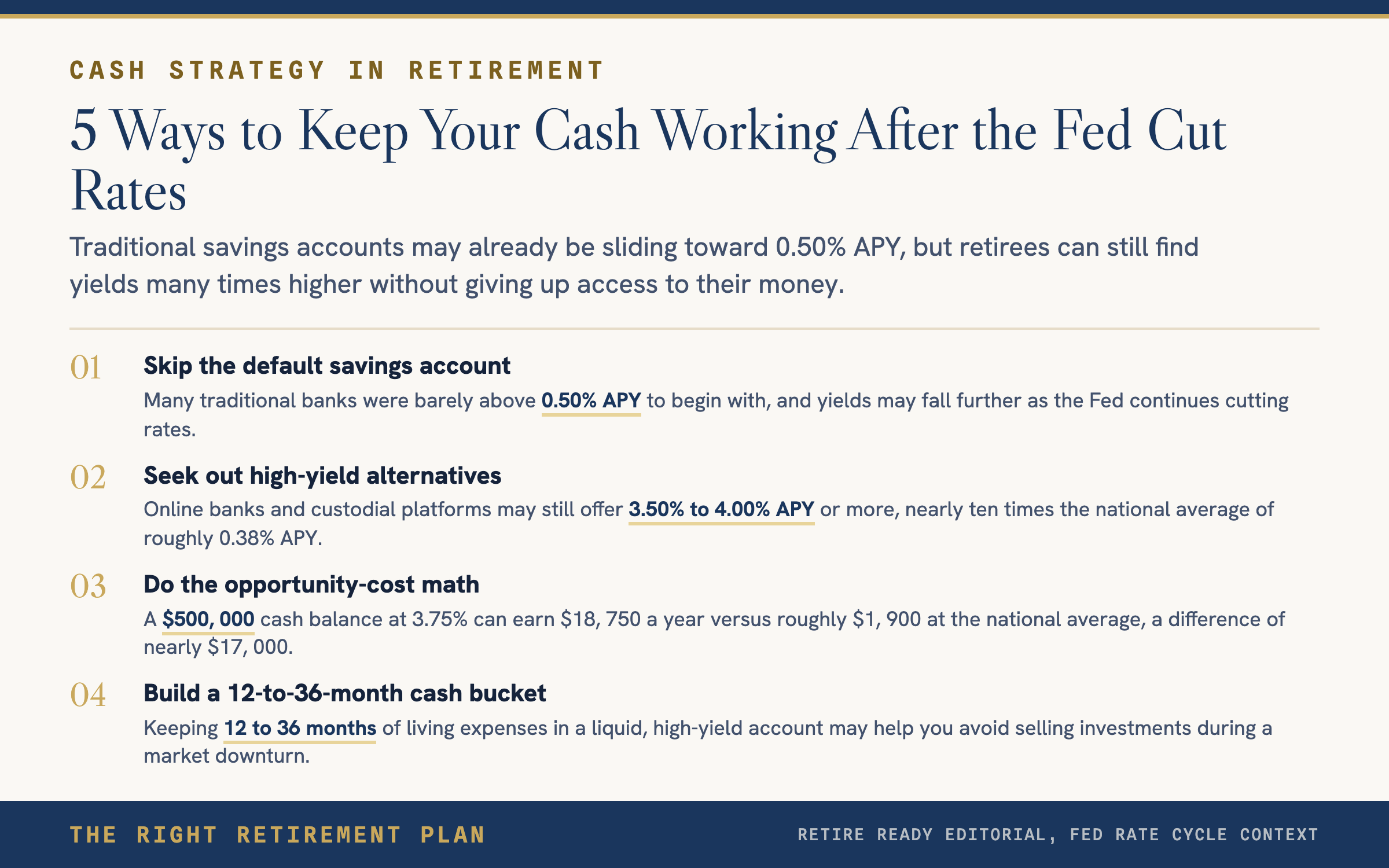

The headlines are clear: the Fed has lowered rates. Borrowers may be smiling, but savers are watching their yields shrink. Traditional banks are already slashing returns on savings accounts, and many were barely above 0.50% APY to begin with.

The good news is that your cash does not have to suffer. High-yield cash accounts from online banks, brokerages, and custodial platforms are still paying in the range of 3.50% to 4.00% APY or more. That is nearly ten times the national average savings rate of roughly 0.38% APY.

Why This Matters for Retirees Right Now

Retirees and pre-retirees tend to hold more cash than younger investors. Emergency reserves, upcoming tax payments, home purchases, and short-term spending needs all require liquid dollars. When those dollars earn next to nothing, the opportunity cost adds up fast.

Here is some simple cash yield math. If you are sitting on $500,000 in cash at the national average of 0.38%, you would earn roughly $1,900 in a year. At 3.75%, that same balance earns $18,750. That is a difference of nearly $17,000, and you never have to give up access to your money.

When shopping for a high-yield option, look for accounts with no lockups, no minimums, and same-day liquidity. Many programs also offer expanded FDIC coverage well beyond the standard $250,000 per depositor by spreading deposits across multiple partner banks.

How a Cash Bucket Strategy Puts Yield to Work

Many retirees use a "bucket" approach to organize their retirement income. The idea is straightforward. Keep 12 to 36 months of living expenses in a liquid, high-yield cash account so you never have to sell investments during a market downturn.

This approach serves multiple purposes.

- It provides a psychological buffer that helps you stay invested when stocks drop.

- It creates a predictable income stream from interest alone.

- It gives you flexibility for large, short-term expenses like taxes, healthcare costs, or home repairs.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.