The Appeal of Cheap Advice

Automated platforms look impressive. The dashboards are clean, the fees hover around 0.25%, and onboarding takes minutes. You answer a few questions about age, risk tolerance, and timeline. Then an algorithm drops you into a model portfolio.

But a model portfolio is not a retirement plan. There is no conversation about which accounts to draw from first, how to time Roth conversions, or what happens to your tax bracket when Required Minimum Distributions (RMDs) kick in. For pre-retirees and retirees managing real complexity, the gaps matter more than the savings.

What the Vanguard Research Actually Shows

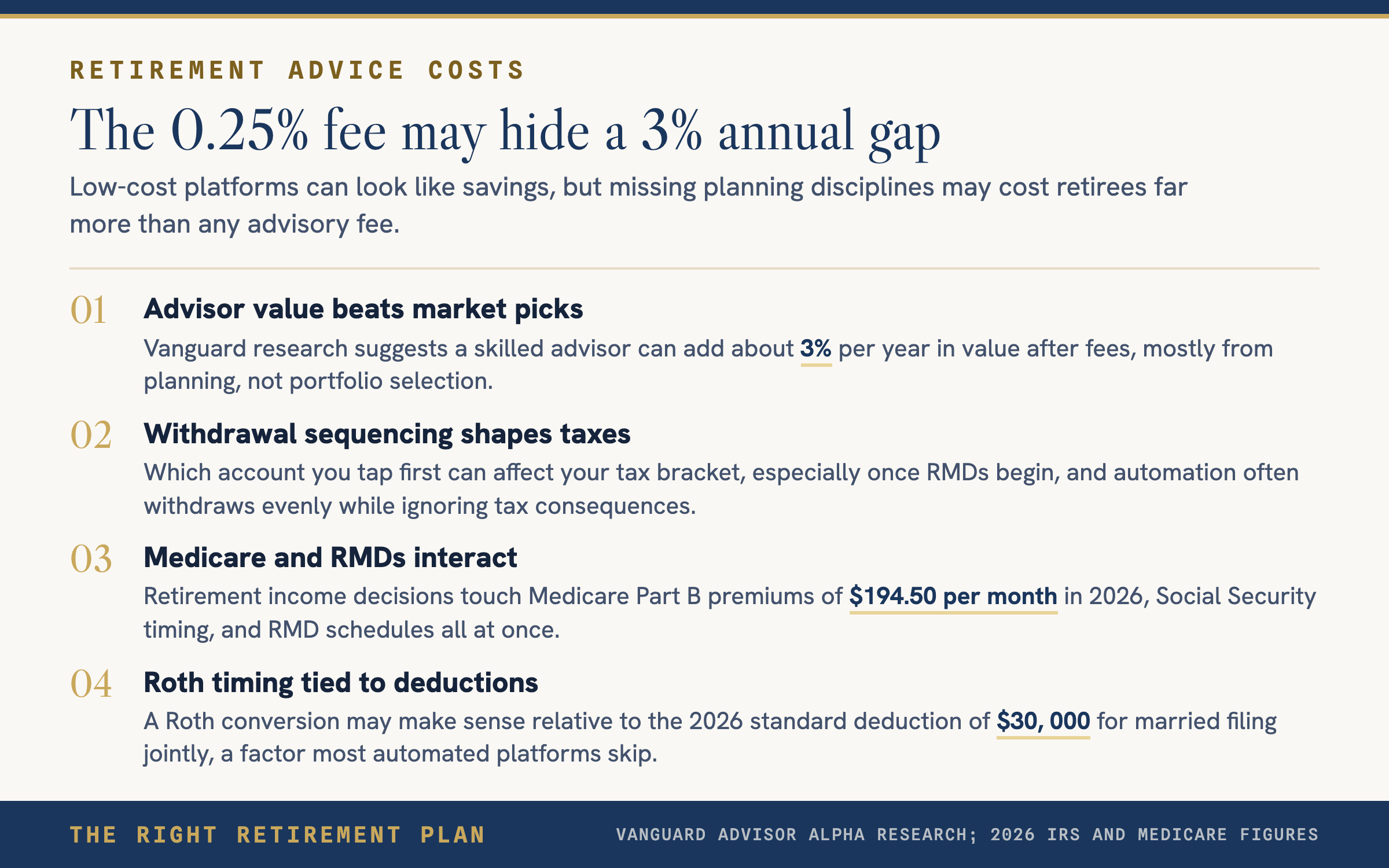

Vanguard's Advisor Alpha study found that working with a knowledgeable advisor can add about 3% per year in additional value after fees. That number does not come from beating the market. It comes from disciplines most low-cost platforms skip entirely.

- Tax-loss harvesting and asset location across account types

- Behavioral coaching that prevents panic selling at the worst time

- Tax-efficient withdrawal strategies that keep you in lower brackets

- Rebalancing and cash flow coordination

Where Retirees Feel It Most

Retirement income planning is not about staying invested. It is about sequencing. Which account do you tap at 63? When does a Roth conversion make sense relative to the 2026 standard deduction of $30,000 for married filing jointly? How do you hold enough cash so you never sell equities in a downturn?

These decisions interact with Medicare premiums (Part B is $194.50 per month in 2026), Social Security timing, and RMD schedules. A fiduciary advisor weighs all of those variables together. An algorithm runs a script and withdraws evenly, ignoring the tax consequences.

Retirees who rely on automation often overpay in taxes and undershoot their sustainable income. The fee looks low, but the lifetime cost of poor withdrawal sequencing can dwarf any advisory fee.

Choosing the Right Help

Not every retiree needs the same level of service, but every retiree deserves a plan that accounts for taxes, income sequencing, and life changes. Before settling on any platform, ask whether it can coordinate your full financial picture or just manage a slice of it.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.