A lot of advisors sound like they are putting your interests first. But behind the scenes, many are cashing commission checks and selling products you do not need. Understanding the fiduciary standard is one of the most important steps a pre-retiree or retiree can take to protect their savings.

The Fiduciary Loophole You Have Never Heard Of

Many advisors call themselves "fiduciaries," but here is the catch. They only act as one some of the time.

They wear two hats. The fiduciary hat goes on when they give investment advice. The sales hat goes on when they sell products like annuities, insurance, or commission-based funds. They get to decide when to switch.

When the sales hat is on, they do not have to recommend what is best for you. They just need to recommend something "suitable enough." Think of a doctor saying, "Technically this medication could work for your condition. I also get a bonus for prescribing it."

How Hidden Fees Actually Work

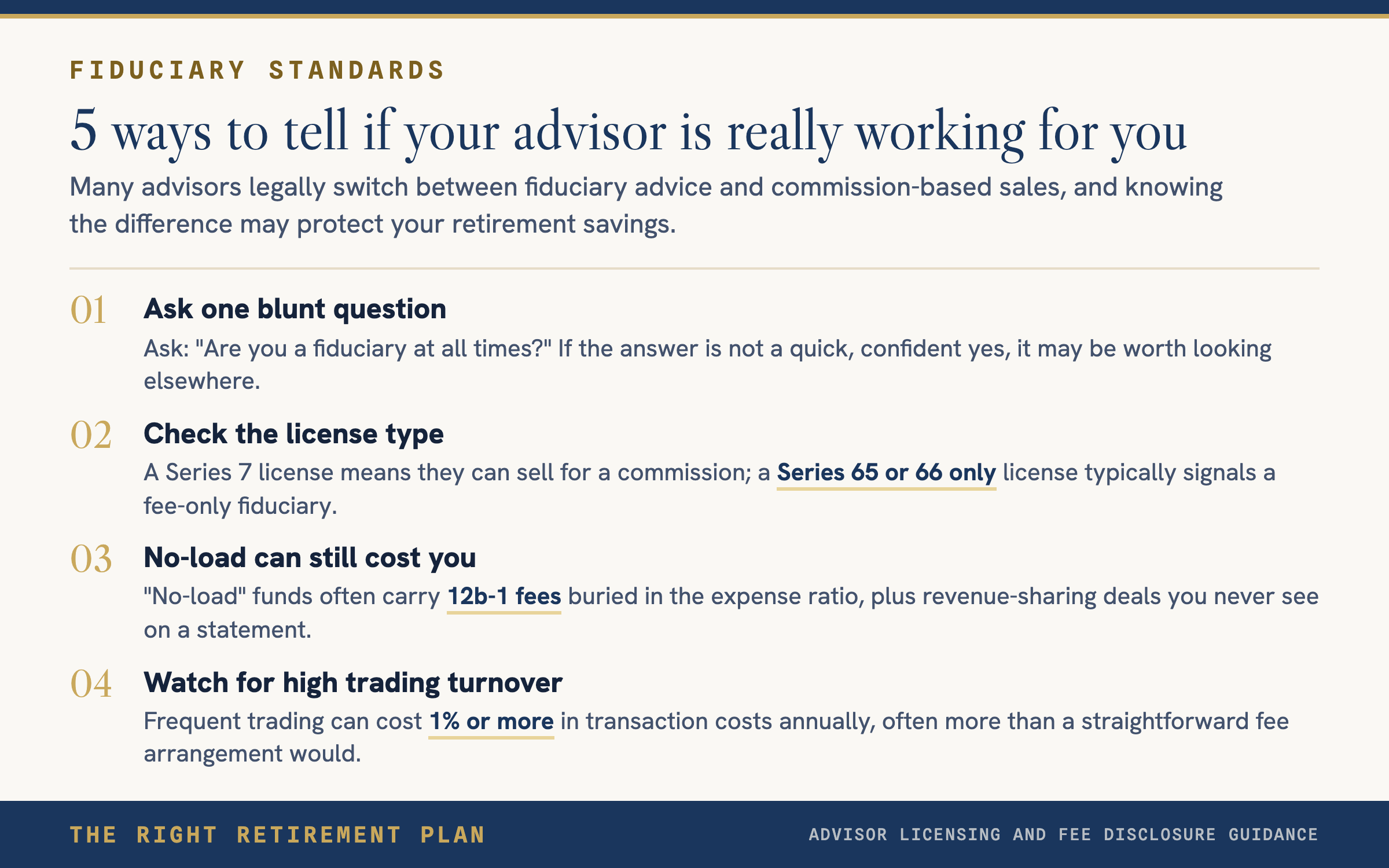

Some advisors claim they use "no-load" mutual funds, implying you are not paying them anything. But those funds often carry 12b-1 fees buried in the expense ratio, revenue-sharing agreements, or shelf-space payments that reward the advisor's firm for promoting certain funds. You are paying. You just do not see it.

Other advisors pitch "free" or "low-cost" advice, then generate revenue through frequent trading. High turnover can cost 1% or more in transaction costs annually. Clients end up paying more through hidden trading activity than they would under a straightforward fee arrangement.

Bank-affiliated advisors may also push credit cards, personal loans, or cash management accounts. These products often come with undisclosed incentives like bonuses, quotas, or internal points. None of that serves your financial plan.

How to Spot a Real Fiduciary Advisor

Checking licenses is the fastest way to know what kind of advice you are getting.

- Series 7: A broker license. They can sell investments for a commission.

- Life and Health Insurance License: They can sell annuities and insurance products.

- Series 65 or 66 only: Typically a fee-only fiduciary.

Ask one direct question: "Are you a fiduciary at all times?" If the answer is not a quick, confident "yes," consider looking elsewhere.

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.