The Power of Strategic Vacation Spending

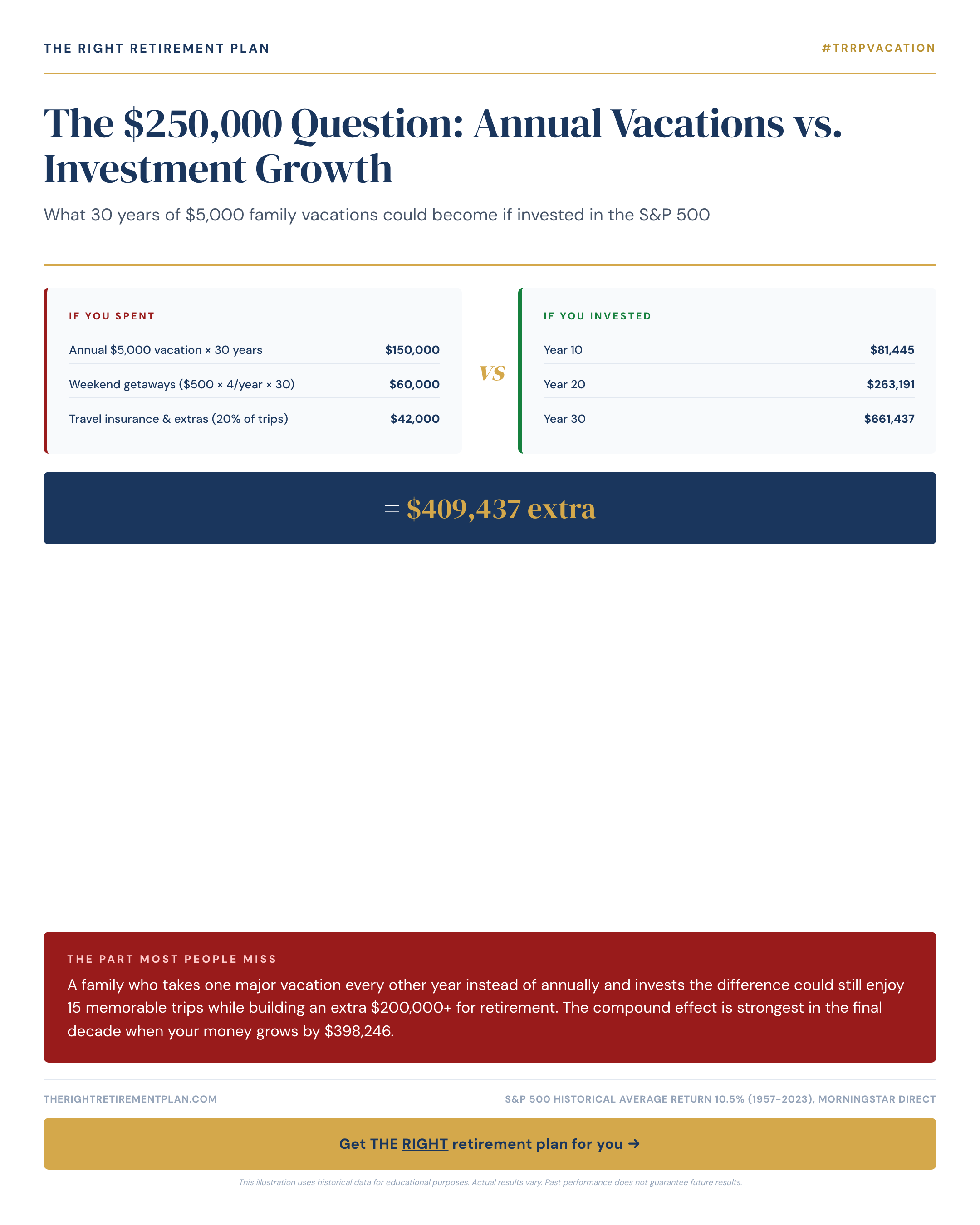

Every year, millions of American families spend around $5,000 on major vacations. While creating memories is invaluable, the retirement planning opportunity cost is staggering. By alternating years, taking a big family trip every other year instead of annually, you could still enjoy 15 memorable vacations over 30 years while potentially building an extra quarter-million dollars for retirement.

Here's the math: investing $5,000 annually in the S&P 500, assuming historical average returns of roughly 10%, would grow to approximately $250,000 over three decades. That's enough to generate an additional $10,000 in annual retirement income using the 4% withdrawal rule.

The Compound Growth Timeline

The magic happens through compound interest, especially in the later years:

- Years 1-10: Your $50,000 in contributions grow to roughly $80,000

- Years 11-20: The balance reaches approximately $175,000

- Years 21-30: Growth accelerates dramatically, with the final decade adding nearly $100,000 in gains alone

The beauty of this approach is flexibility. You're not eliminating vacations, you're being strategic about timing while your money works harder for your future.

Making It Work for Your Family

Consider these practical steps:

- Alternate big trips: Take major vacations every other year, using "off years" for local adventures or visiting family

- Automate the investment: Set up automatic transfers of $416 monthly ($5,000 annually) to prevent spending creep

- Choose low-cost index funds: Keep investment fees minimal to maximize growth potential

If you want personalized guidance on how vacation spending fits into your overall retirement plan, consider taking our Retire Ready Score for insights tailored to your specific situation.