The Time-Horizon Strategy That Changes Everything

Most retirement portfolios fail because they ignore timing. A $1.5 million portfolio using traditional withdrawal strategies often runs dry in bear markets, but smart retirement portfolio management changes the game entirely.

The secret lies in dividing your assets by when you'll need them. Instead of keeping everything in one mixed portfolio, you create three buckets: immediate needs (1-3 years in cash), medium-term stability (4-10 years in bonds), and long-term growth (11+ years in stocks).

Here's why this works: when markets crash, you're not forced to sell stocks at a loss. Your cash bucket covers immediate expenses while your stock holdings recover and compound through multiple market cycles.

Real Numbers for a $1.5M Portfolio

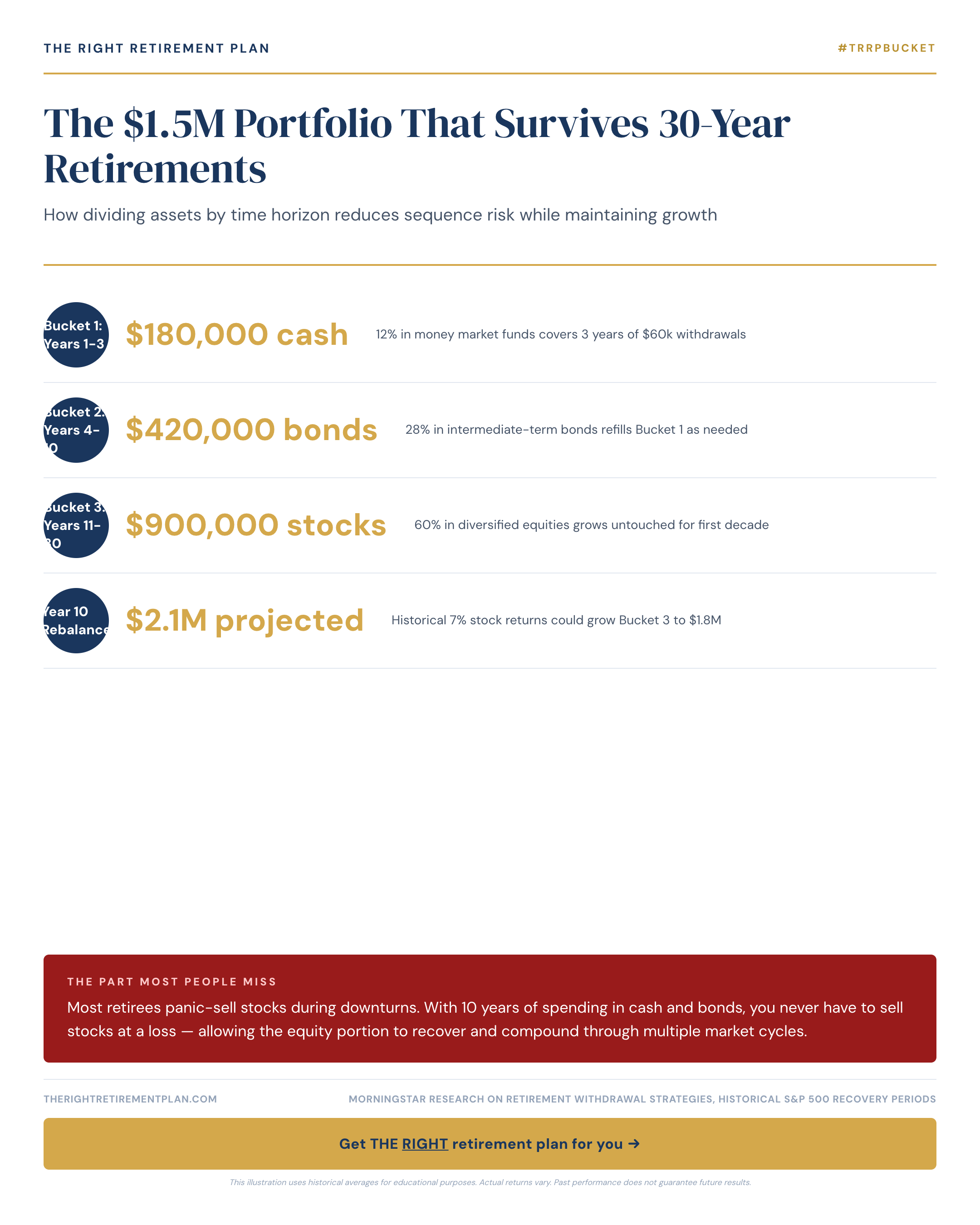

Let's break down the actual allocation that works for most retirees:

- Years 1-3: $180,000 in cash/CDs (covering $60,000 annual spending)

- Years 4-10: $420,000 in bonds and stable investments

- Years 11-30: $900,000 in diversified stock funds

The key advantage? Sequence of returns risk protection. Early retirement losses can devastate traditional portfolios, but time-horizon strategies let you wait out bad markets without touching growth assets.

Implementation Steps

Start by calculating your annual spending needs, then multiply by three for your cash bucket. Your bond allocation should cover years 4-10 of expenses, with the remainder in growth investments.

Most financial advisors recommend rebalancing annually, moving one year of expenses from bonds to cash, and shifting recovered stock gains into the bond bucket. This creates a systematic approach that removes emotion from retirement investment decisions.

Getting retirement math wrong can cost tens of thousands over 30 years, but this approach is completely learnable. If you want personalized guidance on how this strategy applies to your specific situation, consider taking our free Retire Ready Score assessment.