Teacher Pension vs. Tech Salary: The $2 Million Question

When comparing career paths, salary headlines don't tell the full story. A teacher earning $65,000 annually with pension benefits can actually accumulate more long-term wealth than many higher-paid tech workers who must fund their own retirement.

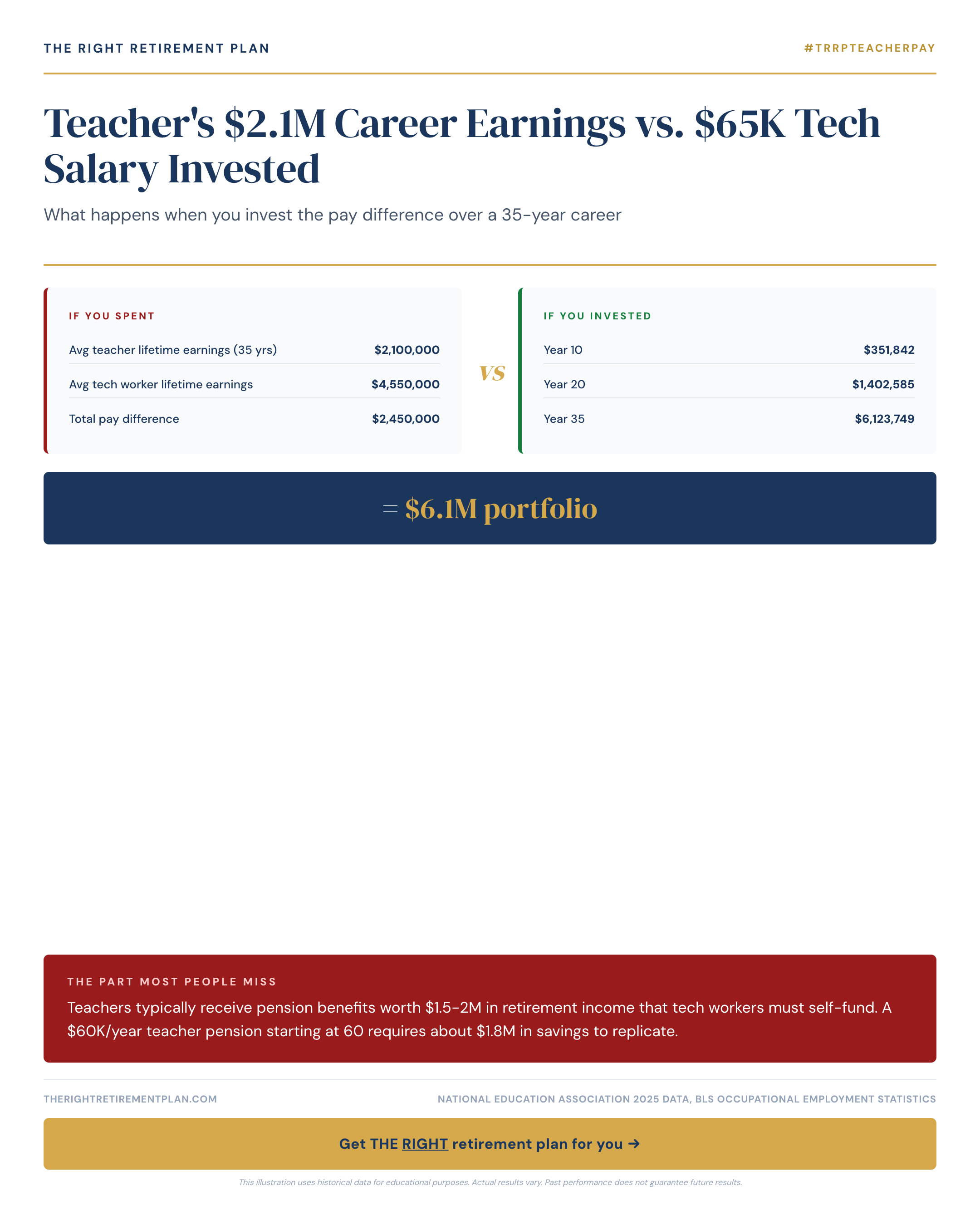

Here's the math that surprises most people: Teachers typically receive pension benefits worth $1.5-2 million in retirement income. A $60,000 annual teacher pension starting at age 60 requires approximately $1.8 million in savings to replicate the same income stream.

Meanwhile, that tech worker earning $100,000+ annually? They're entirely responsible for building their retirement nest egg through 401(k) contributions and personal investments.

The Power of Guaranteed Income

Teacher pensions provide something money can't easily buy: guaranteed lifetime income. This security means teachers can plan confidently, knowing their basic needs will be covered regardless of market volatility.

Tech workers face different challenges:

- Market risk affects their entire retirement portfolio

- No guaranteed income floor in retirement

- Must estimate how long their savings will last

- Healthcare costs aren't subsidized after leaving employment

For Maryland teachers and other public employees in the Mid-Atlantic, this pension security becomes even more valuable when combined with Social Security benefits and any additional savings.

Investment Reality Check

The tech worker's advantage lies in higher earning potential and investment flexibility. Someone earning $35,000 more annually than a teacher has significant opportunity, if they invest the difference wisely.

Key factors that determine success:

- Consistent investing: Contributing 15-20% of income throughout their career

- Market timing: Starting early to benefit from compound growth

- Investment selection: Choosing appropriate risk levels for their timeline

- Fee management: Avoiding high-cost investment products that erode returns

Both career paths can lead to financial security, but they require completely different retirement strategies. Teachers benefit from understanding how to maximize their pension value, while tech workers need sophisticated investment and tax planning.

If you're weighing these considerations for your own retirement journey, consider taking our Retire Ready Score to see how your current strategy stacks up across all the key areas.