The Federal Reserve's latest Survey of Consumer Finances contains a sobering statistic: only 22% of Americans in their 60s have accumulated $250,000 or more in retirement savings. To put this in perspective, a 65-year-old retiring in 2026 with $250,000 could safely withdraw roughly $10,000 annually using the traditional 4% rule, barely enough to cover basic expenses in many areas.

This retirement savings gap isn't just about people who didn't try to save. It reflects systemic challenges that make consistent retirement savings genuinely difficult, combined with decades of financial decisions that seemed minor at the time but compounded into major shortfalls.

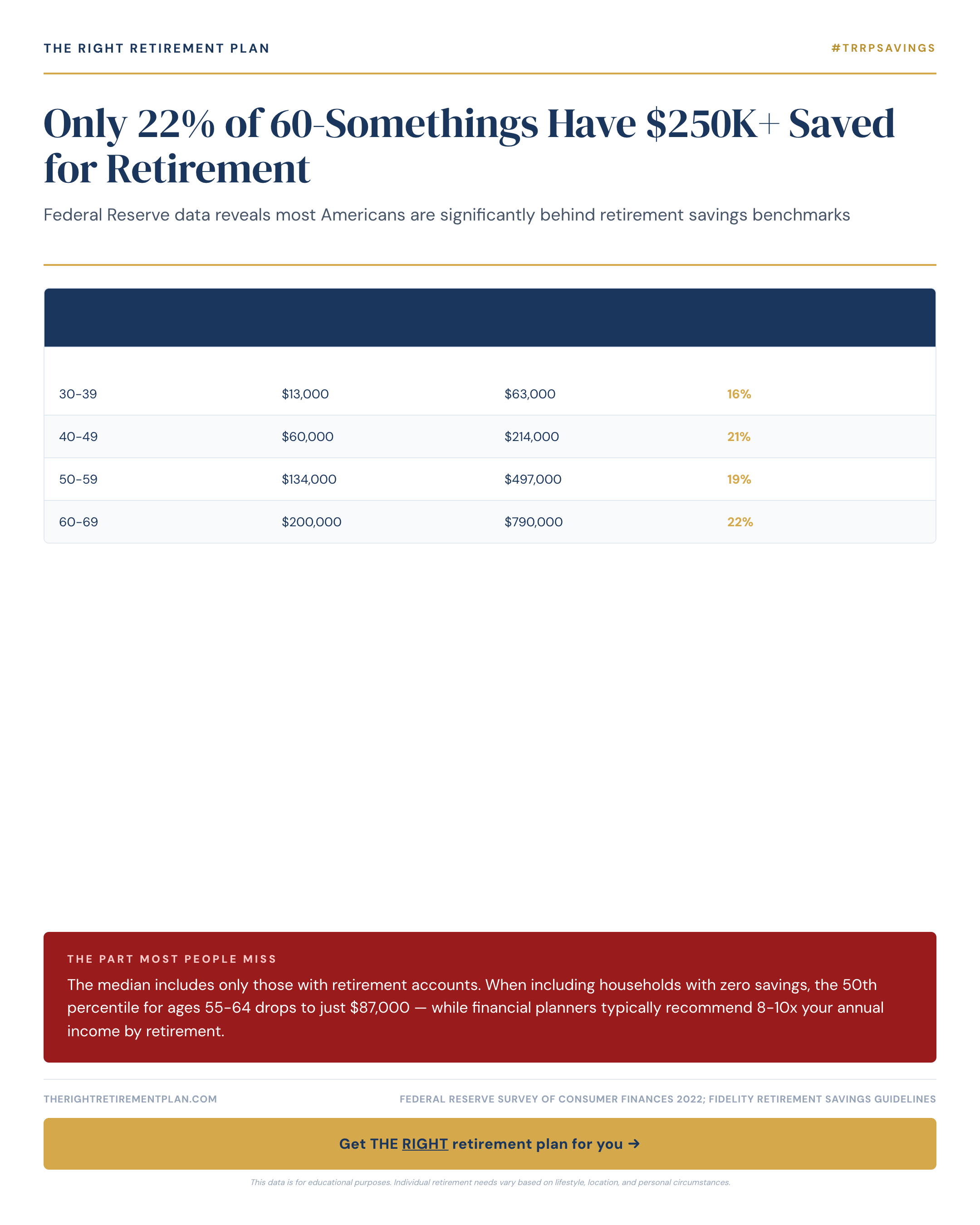

What the Data Really Shows About Retirement Savings

The Federal Reserve's triennial survey provides the most comprehensive view of American household wealth. The 2022 data reveals stark disparities in retirement preparedness among households aged 55-64:

- Bottom 25%: $0-$35,000 in retirement accounts

- Median among savers: Approximately $185,000

- 75th percentile: Around $500,000

- Top 10%: $1 million or more

Most financial planning research suggests accumulating 8-10 times your annual income by retirement age. For someone earning the median household income of roughly $75,000, that translates to $600,000-$750,000, nearly three times the threshold only 22% have reached.

The data also shows significant education and marital status gaps. College-educated households have median retirement savings roughly four times higher than those without degrees. Married couples typically accumulate twice the savings of single individuals.

Why Most Americans Fall Short of Retirement Benchmarks

Financial planning assumptions rarely align with real life. Standard benchmarks assume 40 years of consistent saving, steady 7% annual returns, and no major financial disruptions.

Limited early access to retirement plans costs many workers their most valuable compounding years. A 25-year-old contributing $6,000 annually for 40 years at 7% returns accumulates roughly $1.2 million. Starting at 35 with the same contributions yields approximately $567,000, less than half.

Life disruptions derail consistent saving. Job losses, health crises, divorce, and caregiving responsibilities force nearly 40% of workers to take hardship withdrawals or loans from retirement accounts, according to Employee Benefit Research Institute data.

The pension-to-401(k) shift transferred retirement funding responsibility to individuals without adequate preparation. In 1980, roughly 38% of private-sector workers had defined-benefit pensions. Today, that figure sits below 15%.

Underestimating longevity creates structural shortfalls. A 65-year-old couple has approximately a 50% chance of at least one spouse living past 90, yet many plan for only 20-year retirements.

Proven Strategies to Boost Late-Career Retirement Security

The math becomes challenging after 55, but meaningful improvements remain possible. Maryland retirees and others nearing retirement have several powerful tools available.

Maximize enhanced catch-up contributions. In 2026, workers aged 60-63 can contribute up to $34,750 to their 401(k), $11,250 more than the standard catch-up amount thanks to SECURE 2.0 provisions. Those 50+ can add $8,000 to IRAs. A couple maximizing both could shelter nearly $86,000 annually from taxes.

Delay Social Security strategically. Each year you wait past full retirement age (67 for those born in 1960 or later) until age 70 increases your benefit by 8%. Someone entitled to $2,500 monthly at 67 would receive $3,100 at 70, a permanent 24% increase that also boosts survivor benefits.

Consider bridge employment. Even modest part-time income of $20,000-$30,000 during early retirement reduces portfolio strain significantly. This approach allows retirement accounts more growth time while reducing sequence-of-returns risk.

Coordinate Medicare and Social Security timing. Medicare Part B premiums exceed $185 monthly in 2026, but Income-Related Monthly Adjustment Amounts can substantially increase costs for higher earners. Strategic timing of Roth conversions and Social Security claiming helps manage these thresholds.

This flexibility can be worth the equivalent of having 20-30% more in savings. Conversely, retirees locked into high fixed expenses have little room to maneuver when markets decline or unexpected costs arise.

If you'd like personalized guidance on where you stand relative to retirement readiness benchmarks, consider taking our free Retire Ready Score assessment.