The difference between the 22% and 24% federal tax brackets might seem minor, just two percentage points. But for retirees executing Roth conversions, that gap represents real money. Cross the line by even one dollar, and you'll pay 24 cents on every dollar above the threshold instead of 22 cents.

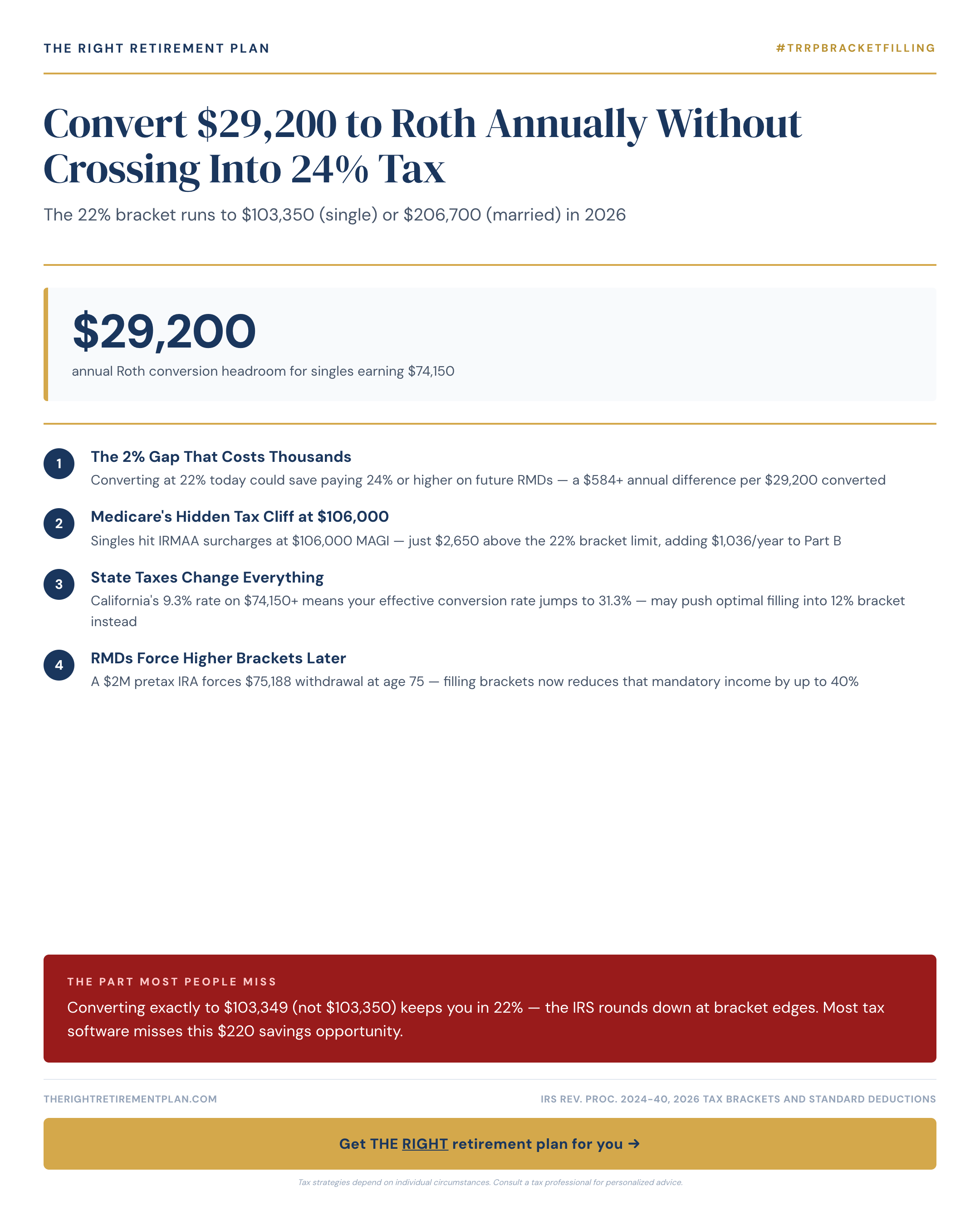

In 2026, the <a href="/blog/2026-tax-brackets-a-250000-couple-pays-18-effective-rate">22% bracket</a> extends to $103,350 for single filers and $206,700 for married couples filing jointly, according to IRS inflation-adjusted projections. For a married couple with $177,500 in other taxable income, that leaves exactly $29,200 of "headroom" before hitting 24%, a window that could allow tax-efficient conversions for years.

Understanding Your 2026 Conversion Capacity

Tax brackets apply to taxable income , not gross income, but the number after subtracting your <a href="/blog/at-65-your-standard-deduction-jumps-to-17300-for-singles">standard or itemized deductions</a>. This distinction is essential for precise <a href="/topics/roth-conversions">Roth conversion planning</a>.

For 2026, the IRS projects these thresholds for the 22% bracket:

- Single filers: $48,476 to $103,350

- Married filing jointly: $96,951 to $206,700

- Head of household: $64,851 to $103,350

To find your available headroom, work backward from the bracket ceiling:

1. Start with the bracket top ($206,700 for married filers)

2. Subtract your standard deduction ($32,300 for married couples 65+ in 2026)

3. Subtract all other income: pensions, taxable Social Security, investment income, and required minimum distributions

Example: A Maryland couple with $119,500 in total income has $206,700, $32,300, $119,500 = $54,900 of conversion capacity while staying in the 22% bracket.

Timing Mistakes That Destroy Your Strategy

Even careful planners stumble on timing issues that push them unexpectedly into higher tax brackets.

The December Surprise

Mutual fund capital gains distributions typically occur in November or December. If you've already executed your Roth conversion in September, a surprise distribution could push you over the threshold.Solution: Complete conversions in late November after most fund distributions are announced.

The Social Security Trap

Conversions increase your modified adjusted gross income, potentially making more <a href="/topics/social-security">Social Security</a> taxable. A $30,000 conversion doesn't just add $30,000 to taxable income, it could push an additional $5,000, $8,000 of previously untaxed Social Security into taxable territory.The RMD Ordering Rule

You cannot convert your required minimum distribution. The first dollars withdrawn from your traditional IRA each year satisfy your RMD before any conversion can occur.Building a Multi-Year Conversion Strategy

Single-year thinking misses the bigger opportunity. Strategic Roth conversions typically work best as a multi-year project, especially during the "gap years" between retirement and age 73 when RMDs begin.

The prime conversion window often occurs during ages 62, 72, when retirees have lower taxable income than they will after RMDs begin. Financial advisors in the Annapolis area frequently help clients map out conversion ladders that take advantage of this window.

Example timeline:

- Ages 63, 64: Convert up to the 22% bracket top

- Ages 65, 72: Balance tax brackets against Medicare premium increases

- Age 73+: Conversion capacity shrinks as RMDs fill bracket space

Key strategies for success:

- Stop $1 below bracket thresholds to account for rounding

- Consider <a href="/topics/medicare">IRMAA cliffs</a> alongside tax brackets

- Complete conversions after year-end fund distributions

- Model the full Social Security provisional income impact

If you want personalized guidance on how tax-efficient retirement strategies might work for your specific situation, consider taking our Retire Ready Score for a comprehensive assessment.