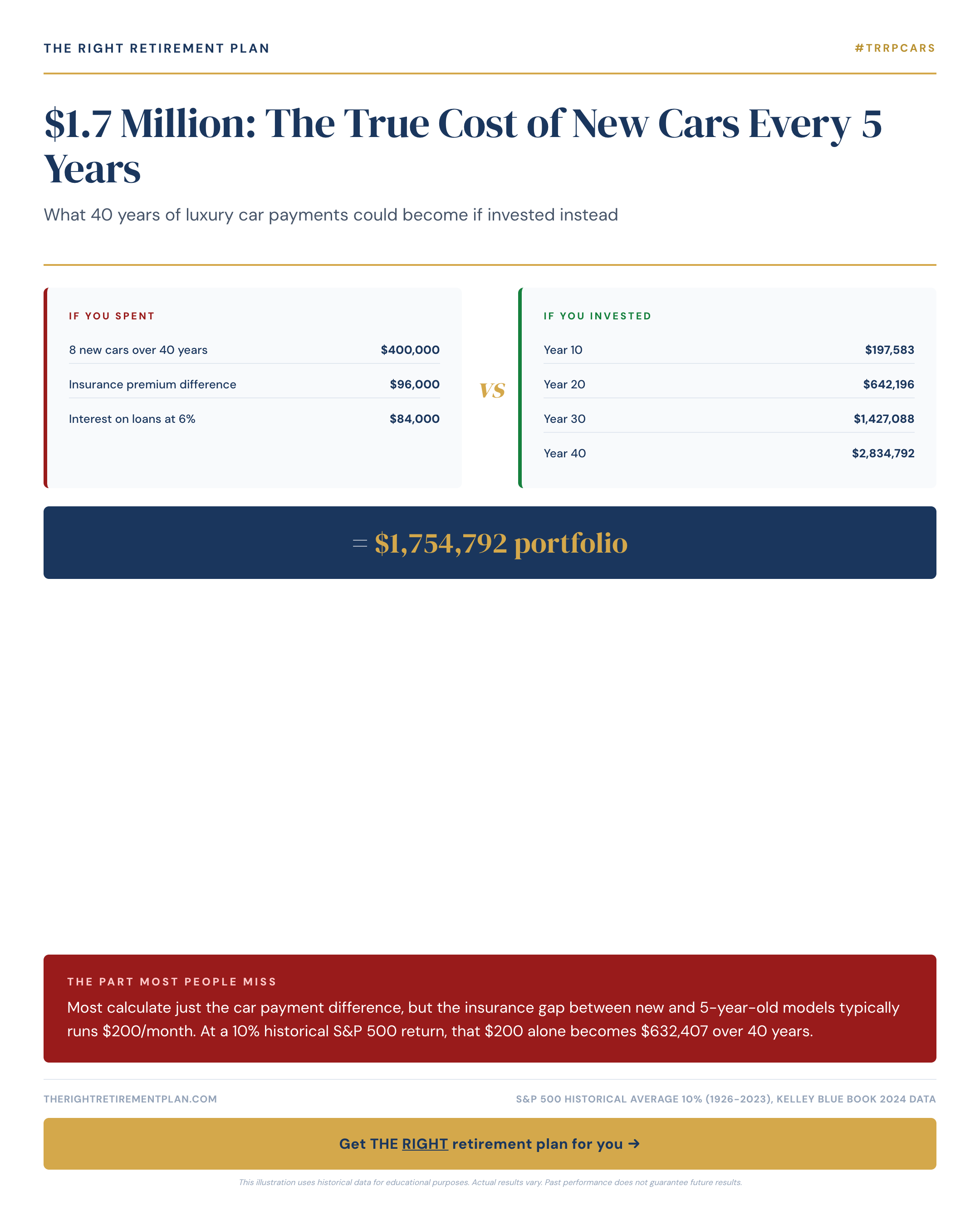

Most people think about car payments in monthly terms, but the real cost of constantly upgrading vehicles extends far beyond the sticker price. When you factor in the opportunity cost of investing that money instead, the true cost of new cars every 5 years can reach a staggering $1.7 million over a 40-year period.

The Hidden Insurance Premium

The math goes deeper than most realize. While many focus on payment differences between new and used vehicles, insurance premiums tell another story. A new luxury vehicle typically costs $200 more per month to insure compared to a 5-year-old model of the same car.

That $200 monthly difference might seem manageable, but invested at the S&P 500's historical 10% annual return, it grows to $632,407 over 40 years. This figure alone represents a significant portion of many Americans' retirement savings goals.

The Compounding Effect of Vehicle Choices

New car purchases every five years create multiple financial drains:

- Higher monthly payments on constantly depreciating assets

- Elevated insurance premiums throughout the ownership period

- Lost investment opportunities from tying up capital in vehicles

- Continuous sales tax and registration fees

The depreciation curve works against frequent upgraders. New vehicles lose roughly 20% of their value in the first year alone, meaning buyers immediately surrender thousands in equity that could have generated returns in the market.

Smart Alternatives for Pre-Retirees

Consider purchasing quality used vehicles 2-3 years old and driving them for 10-15 years. This strategy captures most of the reliability benefits while avoiding the steepest depreciation.

Retirement vehicle planning should prioritize total cost of ownership over monthly affordability. Factor in maintenance, insurance, and opportunity costs when evaluating transportation decisions.

Making informed decisions about major purchases like vehicles can significantly impact your retirement readiness. If you want personalized guidance on how transportation costs fit into your overall retirement strategy, consider taking our Retire Ready Score for insights tailored to your situation.