The Privatization Conversation Is Getting Louder

There is a growing conversation around the future of Social Security, specifically whether it might be privatized. For anyone approaching retirement, that is not just a policy debate. It is a real financial concern.

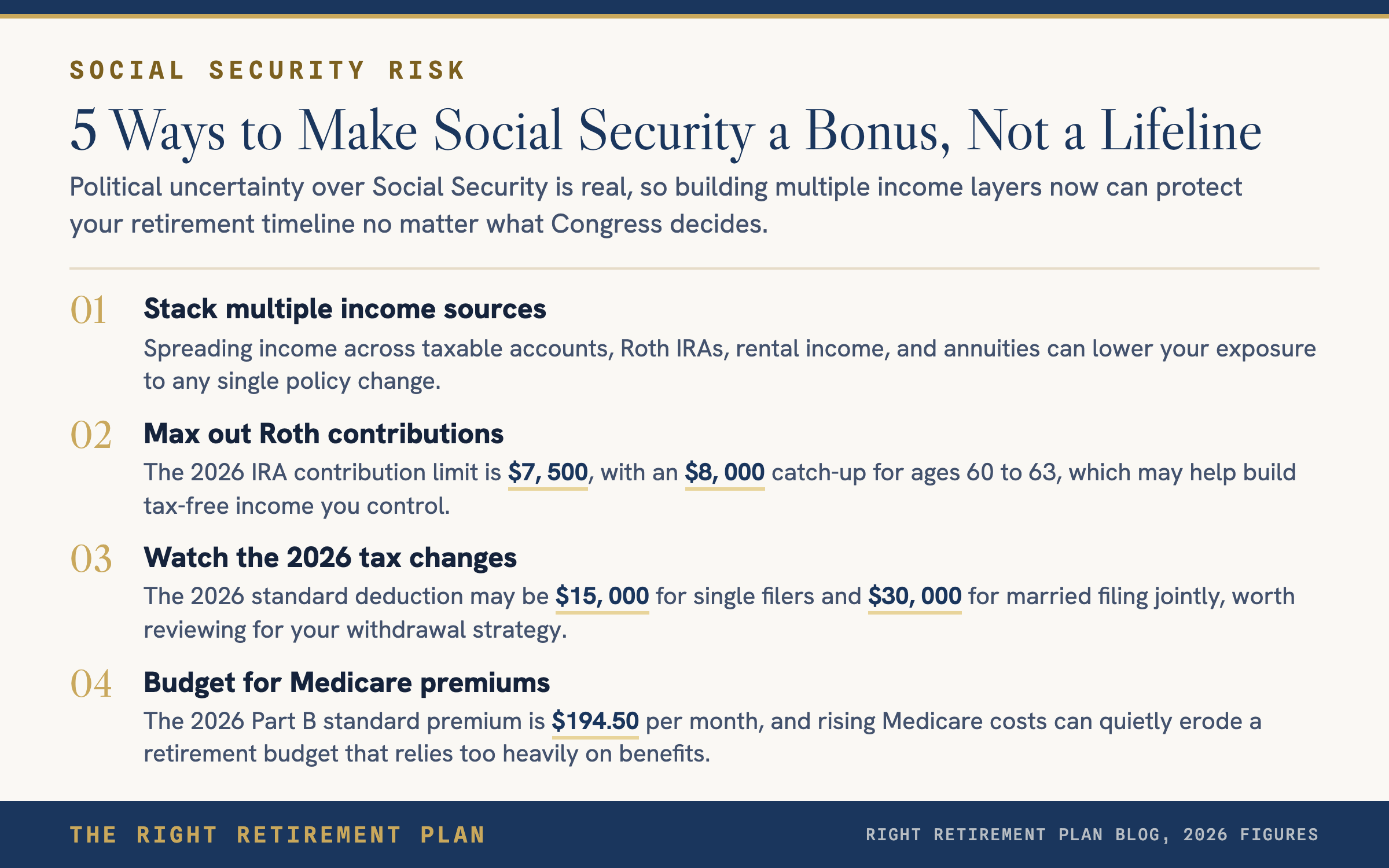

Whether Social Security remains as it is, becomes privatized, or shifts in eligibility rules, one thing is clear. You cannot build your entire retirement on the assumption that it will carry the load. A successful retirement income plan should never depend on a single source of income, especially one controlled by Congress.

The goal is to make Social Security a bonus, not a lifeline.

Build a Plan That Gives You Control

Too many people think retirement starts the day they file for Social Security. Instead of assuming benefits begin at 62 or 67, focus on building a plan that gives you the freedom to retire when you want to, regardless of government changes.

That means creating flexibility through strategies like cash reserves, Roth income ladders, and diversified withdrawal sequencing. When Social Security is just one layer among several, political uncertainty loses much of its power over your retirement date.

To further reduce risk, many retirees diversify across multiple account types and income sources:

- Taxable brokerage accounts

- Roth IRAs and Roth conversions (the 2026 IRA contribution limit is $7,500, with an $8,000 catch-up for ages 60 to 63)

- Rental income or passive real estate

- Annuities, only when truly justified by the math

- Other portfolio income tools

Stay Ahead of Policy Shifts

Big retirement threats do not always come from the stock market. They often come from Washington. That is why a comprehensive retirement review should regularly account for:

- Legislative changes and Social Security proposals

- Tax code updates, including the 2026 standard deduction of $15,000 for single filers and $30,000 for married filing jointly

- Required minimum distributions (RMDs) and how they interact with your tax bracket

- Medicare premium brackets, with the 2026 Part B standard premium at $194.50 per month

The Right Retirement Plan starts with education. If you want to see where your plan stands, take the free Retire Ready Score.