The letter from the IRS makes your heart sink. You missed a Required Minimum Distribution last year, a $40,000 withdrawal you were supposed to take from your traditional IRA. The penalty? A crushing 25% excise tax, meaning you now owe $10,000 on top of regular income taxes.

This scenario happens more often than you'd think. According to the Employee Benefit Research Institute, approximately 20% of retirees subject to RMD rules make distribution errors, with missed deadlines among the costliest mistakes.

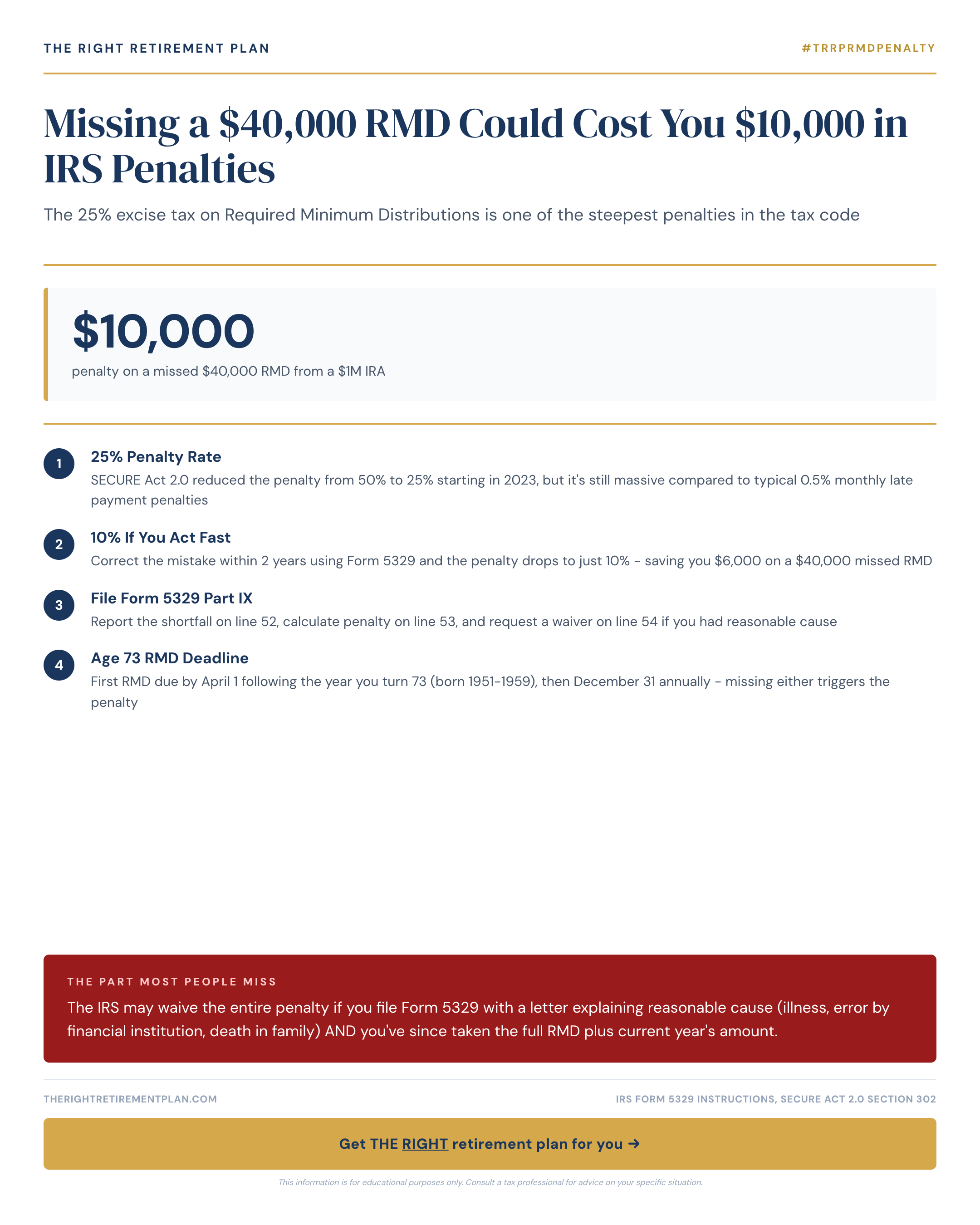

Understanding the 25% RMD Penalty

Required minimum distributions exist because the government wants its share of your tax-deferred savings. Starting at age 73 in 2026 (thanks to <a href="/topics/rmds">SECURE 2.0</a>), you must withdraw minimum amounts annually from traditional IRAs, 401(k)s, and similar accounts.

The RMD calculation divides your December 31st account balance by an IRS life expectancy factor. For a 73-year-old in 2026, that factor is 26.5, requiring roughly 3.77% of your balance as a distribution. On a $1 million IRA, that's approximately $37,736.

When you miss this distribution, IRC Section 4974 imposes the excise tax:

- Missed RMD amount: $40,000

- Excise tax rate: 25%

- Penalty owed: $10,000

- Plus regular income taxes when you eventually withdraw

Common RMD Mistakes to Avoid

Most penalty triggers aren't intentional, they're predictable errors that become avoidable once understood.

Multiple account confusion tops the list. If you have three IRAs at different institutions, you must <a href="/blog/a-500k-ira-300k-401k-two-separate-rmd-calculations">calculate each account's RMD separately</a> (though you can take the total from any combination of accounts). Many retirees miscalculate by using only one account's balance.

<a href="/blog/a-500000-inherited-ira-could-trigger-178000-in-taxes-by-year-10">Inherited IRA complications</a> create another trap. Post-SECURE Act rules require most beneficiaries to deplete inherited accounts within 10 years while taking annual RMDs, requirements many miss entirely.

Timing errors with <a href="/blog/105000-qcd-can-save-23100-in-taxes-at-22-bracket">Qualified Charitable Distributions</a> catch generous retirees off guard. QCDs can satisfy your RMD tax-free, but the charity must receive funds by December 31st.

Other common triggers include:

- Assuming your institution automatically handles RMDs (many don't)

- Confusing Roth IRA rules with traditional IRA requirements

- Forgetting old 401(k)s at former employers

How to Get RMD Penalties Waived

Here's what could save you thousands: the IRS routinely waives the 25% excise tax for taxpayers demonstrating "reasonable cause" who've corrected their error.

The waiver process requires three steps:

Take the missed distribution immediately. Withdraw the full shortfall plus your current year's RMD if applicable. Document everything with account statements.

File Form 5329 with your tax return. Report the RMD shortfall but enter zero for the penalty, attaching an explanation letter.

Write a reasonable cause letter explaining why you missed the distribution and your corrective steps. The IRS accepts various circumstances:

- Serious illness (you or immediate family)

- Financial institution errors

- First-year RMD confusion

- Natural disasters affecting account access

Keep the letter concise, typically one page, with specific dates and clear documentation that you've corrected the shortage.

This means correcting a $40,000 missed RMD promptly reduces your penalty from $10,000 to $4,000 automatically. Combined with a reasonable cause waiver, you could owe nothing, but only if you act before the IRS contacts you first.

Required minimum distribution planning involves complex calculations and tight deadlines that trip up even financially savvy retirees. If you want personalized guidance on avoiding costly RMD mistakes, consider taking our Retire Ready Score for a comprehensive assessment of your retirement readiness.