The Numbers Are Real, The Framing Is Wrong

Amazon took roughly 25 years to reshape retail. The internet took the better part of a decade to change how work gets done. AI is doing in 24 months what those waves did in ten or twenty years. The runway is shorter, the surface area is wider, and the cost savings are landing in real time on real income statements.

That is the easy part of the story. It is the part the headlines are written about, and it is mostly a quarterly earnings discussion. The harder part for retirees is what comes next, because the same wave that is compressing software costs is also compressing the labor force that funds the social safety net.

What This Actually Does To A Retirement Portfolio

Three practical effects matter for a retiree.

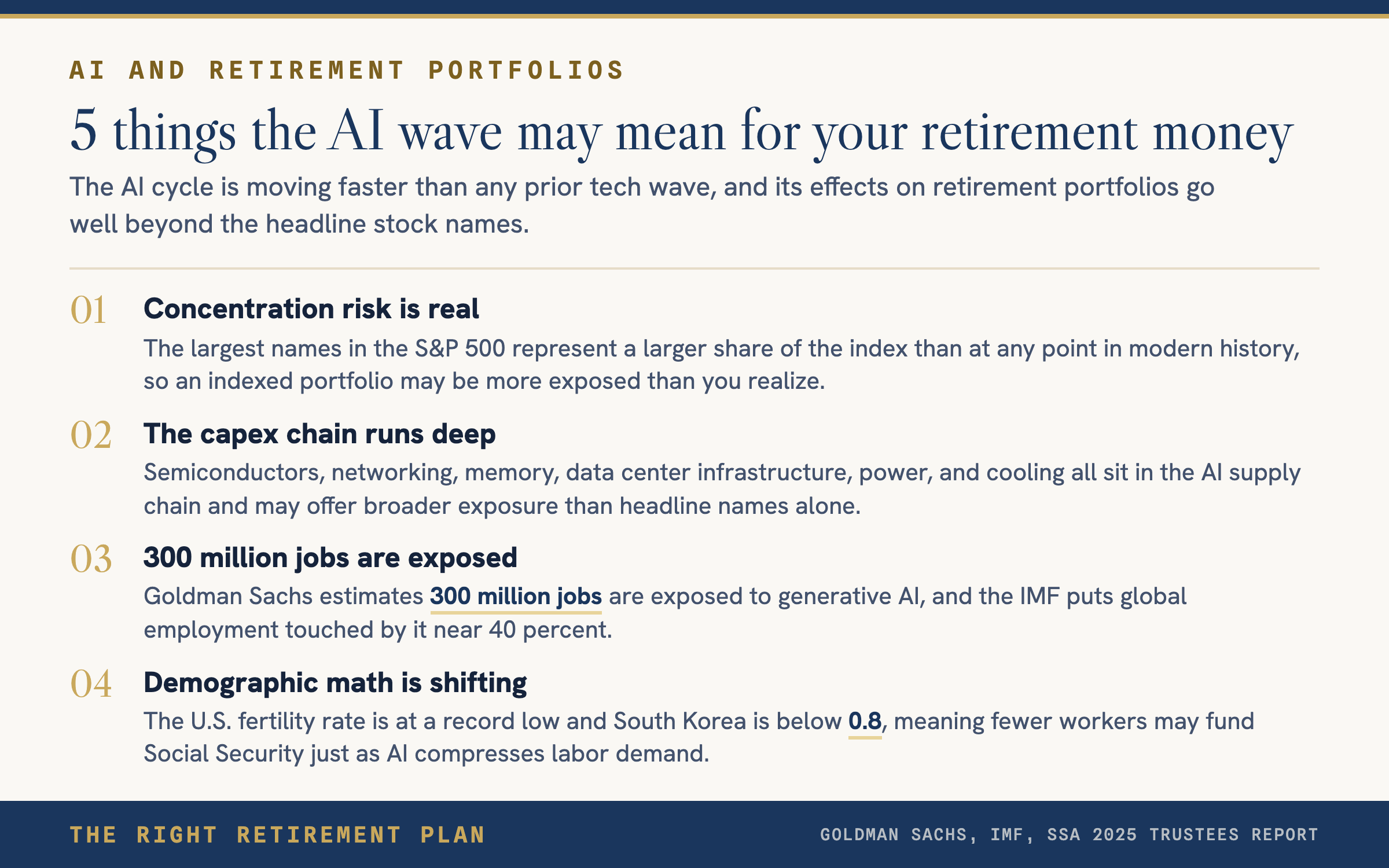

- The capex chain is concrete. Semiconductors, networking, memory, packaging, data center infrastructure, power, cooling, copper. Demand is being funded by some of the most cash rich balance sheets in modern history. That tailwind is real.

- Concentration is real. The largest names in the S&P 500 represent a larger share of the index than at any point in modern history. An indexed retirement portfolio is more exposed to a handful of stocks than most investors realize.

- Productivity gains compress margins for the losers. Companies whose moat was manual labor dressed up as expertise will be repriced. Some of those names sit in legacy index weights that retirees have owned for years.

The Demographic Story Most Plans Ignore

Birth rates are collapsing across the developed world. The U.S. fertility rate is at a record low. South Korea is below 0.8. Japan, Italy, and China are shrinking. If AI shrinks the demand for human labor at the same time the population stops growing, the math gets strange. GDP can keep rising while the labor force falls. Tax receipts, social security funding, and healthcare cost curves all sit downstream of that.

For a retiree, that does not mean panic. It means the assumptions baked into a 30 year retirement projection deserve a second look. Inflation, healthcare cost growth, and Social Security cost of living adjustments are the most exposed.

Frequently Asked Questions

Should I overweight AI stocks in retirement?

No. Most retirement portfolios are already overweight AI through index exposure. The question is whether the rest of the portfolio is diversified enough to survive a multi quarter pullback in the largest names.

Is AI a bubble?

The earnings are real. The valuations are stretched on some names and reasonable on others. Saying the entire wave is a bubble has been a bad bet for two years and saying every name is fairly valued has been worse.

Will AI hurt Social Security?

It is upstream. A smaller working age population funding a larger retired one strains the trust fund regardless of AI. The 2025 trustees report already projects depletion in the mid 2030s. AI accelerates the productivity question. It does not change the demographic one.

Should I switch to dividend stocks because of AI volatility?

No. The instinct to flee growth for yield in a volatile market is one of the most expensive moves retirees make. The right move is the right allocation for your timeline, not a reaction to the last 90 days.

Does any of this change the 4 percent rule?

Not directly. The withdrawal math depends on real return and inflation. AI may raise productivity which is disinflationary. Demographics may be inflationary. The right answer is to stress test the plan against both.

Take The Next Step

If you want a quick read on whether your current portfolio is positioned for the next decade rather than the last one, take the free Retire Ready Score. It maps your setup against the five pillars of a complete retirement plan in a few minutes.